Will I Avoid IRMAA Surcharges on Medicare Part B and Part D?

Flowchart to determine whether your income will trigger IRMAA surcharges on Medicare premiums.

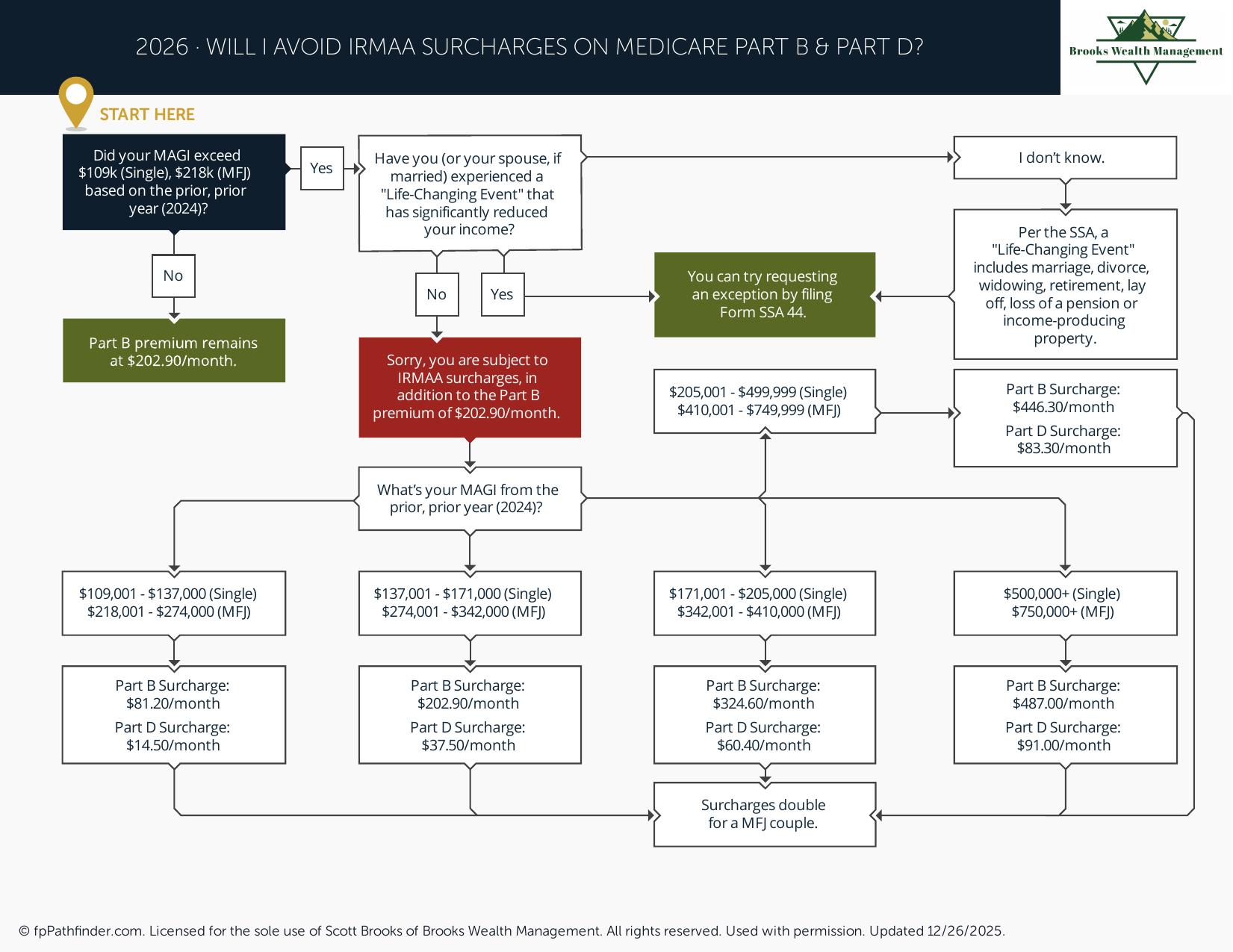

Will I Avoid Medicare IRMAA Surcharges on Part B and Part D?

Individuals enrolled in Medicare may pay higher Medicare Part B and Part D premiums if their income exceeds certain thresholds established by federal law. These additional premiums are known as Income-Related Monthly Adjustment Amounts (IRMAA).

Many retirees review their income and tax situation periodically to better understand whether Medicare IRMAA surcharges may apply in future years.

This resource highlights several common issues individuals review when evaluating potential Medicare IRMAA exposure.

Understand How Medicare IRMAA Is Calculated

Medicare IRMAA surcharges are generally based on Modified Adjusted Gross Income (MAGI) reported on a federal tax return from two years prior.

For example, Medicare premiums in one year are typically based on income reported two tax years earlier.

MAGI for Medicare purposes generally includes:

- Adjusted Gross Income (AGI)

- Tax-exempt interest income

If income exceeds certain thresholds, higher Medicare Part B and Part D premiums may apply.

Review Sources of Income That May Affect IRMAA

Many retirees review all sources of income that could increase Modified Adjusted Gross Income.

Common income sources include:

- Traditional IRA withdrawals

- 401(k) distributions

- Pension income

- Employment income

- Rental income

- Capital gains

- Business income

- Interest and dividend income

- Tax-exempt municipal bond interest

Even a one-time income event may affect Medicare premiums in a future year if it increases income above an IRMAA threshold.

Review Potential Capital Gain Events

Many individuals review whether significant capital gains could affect future Medicare premiums.

Examples may include:

- Sale of a business

- Sale of investment property

- Large taxable investment gains

- Concentrated stock sales

Because IRMAA is based on prior-year income, a large capital gain may affect Medicare premiums for a future year even if income later declines.

Review Retirement Account Distributions

Retirement account withdrawals frequently represent one of the largest contributors to retirement income.

Individuals often review:

- Traditional IRA distributions

- 401(k) withdrawals

- Required Minimum Distributions (RMDs)

- Qualified Charitable Distributions (QCDs)

- Roth IRA distributions

Understanding how retirement account distributions affect taxable income may help retirees evaluate future Medicare premium exposure.

Additional information is available in our resources covering Required Minimum Distributions and retirement withdrawal strategies.

Review Roth Conversion Activity

Individuals considering Roth conversions often review the impact on Medicare premiums.

Although Roth conversions may be used as part of a broader retirement income strategy, the amount converted generally increases taxable income during the year of conversion.

Because Medicare IRMAA calculations are income-based, retirees frequently evaluate how Roth conversion activity may affect future Medicare premiums.

For additional information, see our resource on Roth conversions.

Review Whether a Life-Changing Event Applies

Medicare beneficiaries who experience certain life-changing events may be eligible to request a review of their IRMAA determination.

Examples may include:

- Retirement or work stoppage

- Reduction in work hours

- Death of a spouse

- Divorce or marriage

- Loss of income-producing property under certain circumstances

Individuals experiencing these events often review whether updated income information may be considered by the Social Security Administration.

Review Medicare Costs as Part of Retirement Planning

Healthcare expenses represent a significant retirement cost for many households.

As part of a broader retirement planning review, individuals often evaluate:

- Medicare premiums

- IRMAA surcharges

- Prescription drug costs

- Healthcare expenses

- Retirement account withdrawal strategies

- Tax planning opportunities

Additional retirement planning resources are available on:

About This Resource

This resource provides general educational information regarding Medicare IRMAA surcharges. It is not intended as investment, tax, legal, healthcare, or financial advice. Medicare rules, income thresholds, and premium amounts may change over time.

If you would like to discuss Medicare planning, retirement income strategies, or broader retirement considerations, we invite you to schedule an introductory conversation.