Should I Consider Doing a Roth Conversion?

Flowchart to evaluate whether a Roth conversion makes sense given your tax situation.

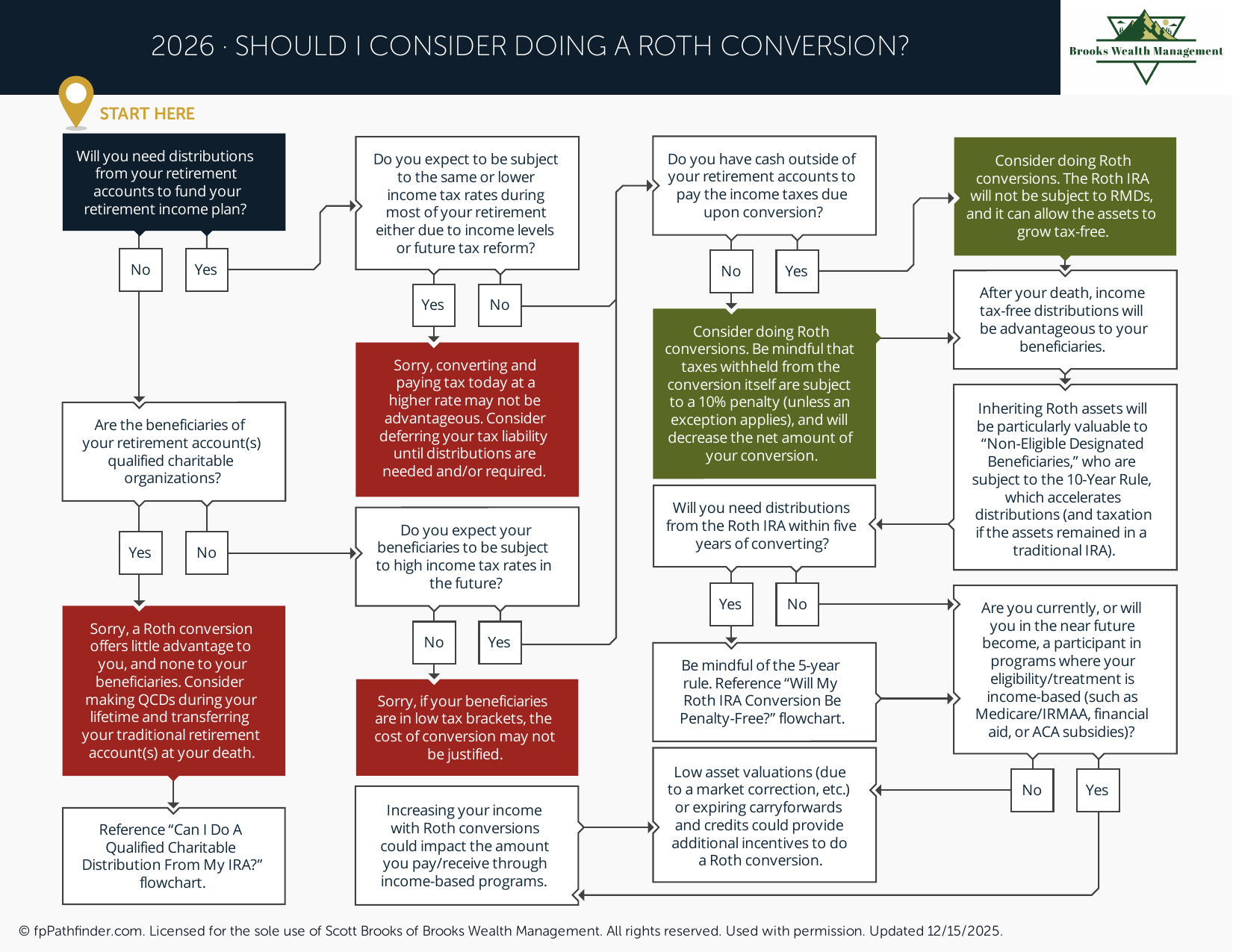

Should I Consider Doing a Roth Conversion?

A Roth conversion may be appropriate when current tax rates are lower than the tax rates you expect to face in the future. The decision depends on your income, retirement timeline, future required minimum distributions, and your ability to pay the conversion tax from assets outside of the retirement account.

While Roth conversions can create future tax-free income, they also increase taxable income in the year of conversion. Reviewing the potential benefits and tradeoffs before making a decision is important.

Review Your Current and Expected Future Tax Brackets

The primary purpose of a Roth conversion is to voluntarily pay income tax today in exchange for tax-free growth and tax-free qualified withdrawals later. Individuals often review whether their current marginal tax rate is lower than the rate they may face in retirement.

- Current federal and state tax rates

- Expected retirement income sources

- Future tax law uncertainty

- Potential changes in filing status

Review Whether You Have a Temporary Low-Income Opportunity

Many Roth conversions occur during years when taxable income is temporarily reduced. These periods can create opportunities to convert assets at lower tax rates than might otherwise apply.

- Early retirement before Social Security begins

- Career transitions or sabbaticals

- Business income fluctuations

- Years before pension income begins

Review Future Required Minimum Distributions

Large traditional IRA balances may eventually create significant required minimum distributions. Those distributions can increase taxable income later in retirement regardless of whether the income is needed.

- Projected IRA balances at retirement

- Expected RMD amounts

- Potential impact on tax brackets

- Long-term retirement income needs

Review Medicare IRMAA Considerations

A Roth conversion increases modified adjusted gross income during the year the conversion occurs. Higher income may affect Medicare Part B and Part D premiums through Income Related Monthly Adjustment Amount (IRMAA) surcharges.

- Current Medicare enrollment status

- Projected income after conversion

- Applicable IRMAA thresholds

- Multi-year tax planning opportunities

Review How You Will Pay the Conversion Tax

One factor frequently reviewed is the source of funds used to pay the conversion tax. The ability to pay taxes from non-retirement assets may preserve more retirement capital for future tax-free growth.

- Available taxable savings

- Cash flow needs

- Age and retirement timeline

- Potential penalties if retirement assets are used

Review Estate and Legacy Planning Goals

Roth IRAs may provide different planning opportunities for beneficiaries compared to traditional IRAs. The potential value of future tax-free distributions is often considered as part of broader estate planning discussions.

- Beneficiary tax situations

- Legacy objectives

- Expected account growth

- Estate planning priorities

Review Whether Partial Conversions May Be Appropriate

Many individuals do not convert their entire retirement account at once. Instead, they review whether smaller annual conversions may allow them to manage taxes more effectively over time.

- Available tax bracket capacity

- Multi-year conversion opportunities

- Projected retirement dates

- Long-term tax planning objectives

For additional context, review our resources on Roth IRA vs. Traditional IRA contributions, whether a Roth conversion will be penalty-free, IRMAA considerations, and where your next dollar should go in the free resource library.

About This Resource

This resource provides general educational information regarding Roth conversions and retirement income planning. Individuals often review Roth conversion opportunities when evaluating future tax liability, retirement income flexibility, required minimum distributions, and estate planning considerations.

Whether a Roth conversion is beneficial depends on individual circumstances including tax rates, retirement timing, available assets, Medicare considerations, and long-term financial objectives. Rules and tax laws may change over time.

This resource is intended as a starting point for evaluating the issues that may be relevant before completing a Roth conversion.

If you would like to discuss how this topic fits into your broader financial plan, we invite you to schedule an introductory conversation.