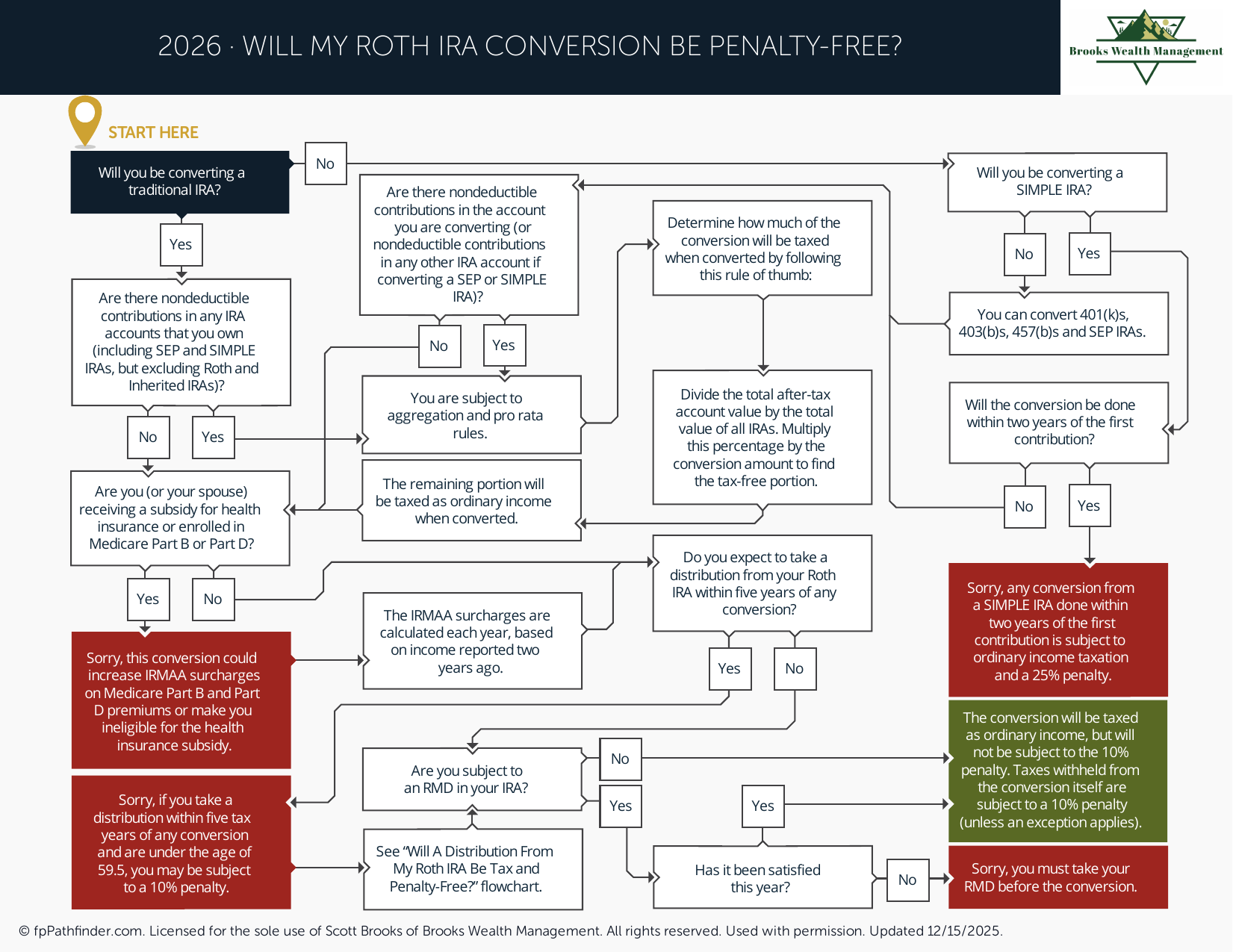

Will My Roth IRA Conversion Be Penalty-Free?

Flowchart to determine whether a Roth IRA conversion will trigger the 10% penalty.

Will My Roth IRA Conversion Be Penalty-Free?

A Roth IRA conversion itself is generally not subject to the 10% early withdrawal penalty. However, whether future withdrawals from converted funds will be penalty-free depends on several factors, including your age, the timing of the conversion, and whether specific IRS exceptions apply.

Because Roth conversion rules involve separate holding periods and distribution ordering rules, individuals often review conversion strategies carefully before moving funds from a traditional IRA, rollover IRA, SEP IRA, SIMPLE IRA, or employer-sponsored retirement plan into a Roth IRA.

Review How a Roth IRA Conversion Works

A Roth IRA conversion occurs when assets are moved from a pre-tax retirement account into a Roth IRA. The amount converted is generally included in taxable income during the year of conversion, unless a portion represents after-tax contributions.

Common reasons individuals review Roth conversions include:

- Building tax-free retirement income sources.

- Reducing future required minimum distributions.

- Creating greater flexibility in retirement income planning.

- Evaluating future tax rate uncertainty.

- Supporting estate and wealth transfer objectives.

Additional information is available in our resource discussing whether a Roth conversion should be considered.

Review Whether the Conversion Itself Is Subject to Penalties

One of the most common misconceptions is that converting retirement funds to a Roth IRA automatically creates an early withdrawal penalty.

In general, the act of converting funds is not subject to the 10% early withdrawal penalty, regardless of age. However, income taxes may apply to the taxable portion of the conversion.

Common considerations include:

- The amount being converted.

- Your current tax bracket.

- Whether after-tax contributions exist in the account.

- Available cash to pay any resulting tax liability.

- The effect of the conversion on other tax-related items.

Because a Roth conversion increases taxable income in the year of conversion, many individuals evaluate the broader tax consequences before proceeding.

Review the Roth Conversion Five-Year Rule

Each Roth conversion generally has its own five-year holding period for purposes of determining whether converted funds can be withdrawn without penalty before age 59½.

Common considerations include:

- The year each conversion occurred.

- Whether multiple conversions have been completed.

- Your current age.

- Expected future withdrawal needs.

- Whether exceptions to the penalty rules may apply.

If converted funds are withdrawn before satisfying the applicable holding period and before reaching age 59½, a penalty may apply unless an exception is available.

For this reason, individuals often review liquidity needs before implementing a conversion strategy.

Review the General Roth IRA Five-Year Rule

Separate from the conversion holding period, Roth IRAs also have a broader five-year rule that applies to qualified distributions of earnings.

In general, qualified distributions depend on:

- The age of the Roth IRA owner.

- The date the first Roth IRA was established.

- Whether a qualifying event has occurred.

- The source of the distribution.

- The ordering rules that apply to Roth IRA withdrawals.

Individuals often review both five-year rules together because they serve different purposes and can affect the taxation and penalty treatment of distributions.

Review Common Exceptions to Early Withdrawal Penalties

Certain distributions may qualify for exceptions to the 10% early withdrawal penalty.

Common exceptions individuals review include:

- Attaining age 59½.

- Disability.

- Qualified first-time home purchases.

- Certain higher education expenses.

- Certain unreimbursed medical expenses.

- Substantially equal periodic payment arrangements.

- Distributions following the account owner's death.

Whether an exception applies depends on individual circumstances and applicable IRS requirements.

Review Liquidity Before Completing a Roth Conversion

One of the most important planning considerations involves whether converted funds may be needed in the near future.

Individuals often review:

- Emergency reserve needs.

- Upcoming major purchases.

- Retirement timing.

- Expected cash flow requirements.

- The ability to pay conversion-related taxes from non-retirement assets.

Because Roth conversions are often intended as long-term planning strategies, understanding future liquidity needs may help reduce the likelihood of needing to access converted assets prematurely.

Individuals evaluating broader savings decisions may also find it helpful to review what accounts to consider when saving more.

Review Whether a Roth Conversion Fits Within Your Financial Plan

A Roth conversion may be evaluated as part of a broader retirement income, tax, and estate planning strategy.

Common questions individuals review include:

- Are future tax rates expected to be higher or lower?

- Will future required minimum distributions create taxable income concerns?

- Is there sufficient cash available to pay conversion-related taxes?

- How does the conversion affect retirement income projections?

- How does the conversion fit within broader wealth transfer goals?

Because the benefits and tradeoffs vary by individual circumstances, Roth conversions are often evaluated alongside retirement planning, tax planning, and legacy planning objectives.

Additional retirement planning considerations can be found in our guide discussing issues to consider before retirement.

About This Resource

This resource provides general educational information regarding Roth IRA conversions, conversion holding periods, and early withdrawal penalty considerations. Roth conversion rules involve multiple IRS requirements, including taxation, distribution ordering rules, and separate five-year holding periods that may affect future withdrawals.

Individuals often review Roth conversion strategies when evaluating retirement income planning, future tax rates, required minimum distributions, estate planning objectives, and long-term wealth accumulation goals. Whether a Roth conversion is beneficial depends on individual circumstances, current and projected tax situations, available assets, and broader financial planning objectives.

This resource is intended to provide a framework for understanding common Roth conversion considerations. It is not intended as investment, tax, legal, insurance, healthcare, cybersecurity, or financial advice. Individual circumstances vary, and tax rules may change over time.

If you would like to discuss how this topic fits into your broader financial plan, we invite you to schedule an introductory conversation.