Your financial life, working as one.

Every piece, brought together through a clear process, so nothing important falls through the cracks.

The Seven Plans of Your Financial Life

No financial decision happens in isolation. These are the seven plans we build and coordinate together, so every part of your financial life works as one. Hover any plan to see what it covers.

Everything starts here. Before any numbers, we get clear on what you actually want your money to make possible, whether you're building toward a life or already living it, and what that life truly costs.

- What you want your money to make possible, now and later

- The goals that matter most, and the tradeoffs between them

- What your ideal life actually costs

Everything flowing through your life: money in, money out, savings, and debt. While you're working, it's about routing every dollar well. In retirement, it's turning what you've built into a reliable paycheck.

- Where your money goes, and whether it matches your priorities

- Debt, savings, and the order you fund your accounts

- Turning savings into income, including Social Security timing

A portfolio built around your actual life, not market predictions or headlines. How much growth you need, how much risk fits, and how the mix should change as you move from building wealth to living on it.

- The right balance of risk and growth for your stage

- Tax-smart placement across your accounts

- Managing concentrated stock and equity compensation

Keeping more of what's yours across your whole life, not just this April. From Roth decisions and equity comp in your earning years to conversions and withdrawal order once you retire.

- Roth versus traditional, and the order you fund accounts

- Managing capital gains and equity compensation

- Conversions, RMDs, and withdrawal sequencing later on

Covering the costs that can quietly derail everything else, from using your HSA well today to navigating the years before Medicare, then Medicare and long-term care down the road.

- Using your HSA as a long-term tool

- Bridging coverage before 65, then choosing wisely at Medicare

- Planning ahead for long-term care

Protecting the plan, and the people who depend on you, without turning insurance into the plan. The right coverage for the life you're trying to protect, and nothing you don't need.

- Life and disability coverage matched to your real needs

- Protecting your home, assets, and liability exposure

- Guarding against outliving your money later on

Making sure your wishes, and your people, are taken care of. From the essential documents today to legacy, giving, and tax-efficient transfer as your estate grows.

- Wills, powers of attorney, and beneficiary designations

- Titling, and how everything passes on

- Legacy goals, charitable giving, and tax-efficient transfer

Lifestyle Plan

Everything starts here. Before any numbers, we get clear on what you actually want your money to make possible, whether you're building toward a life or already living it, and what that life truly costs.

- What you want your money to make possible, now and later

- The goals that matter most, and the tradeoffs between them

- What your ideal life actually costs

Every other plan takes its direction from this one. Without it, recommendations are just guesses.

Data-Driven Planning

Brooks Wealth Management's financial planning process is data-driven, using industry-leading technology and financial planning software to help turn complex financial decisions into a clear path.

A quick look at how planning technology can help organize the moving parts.

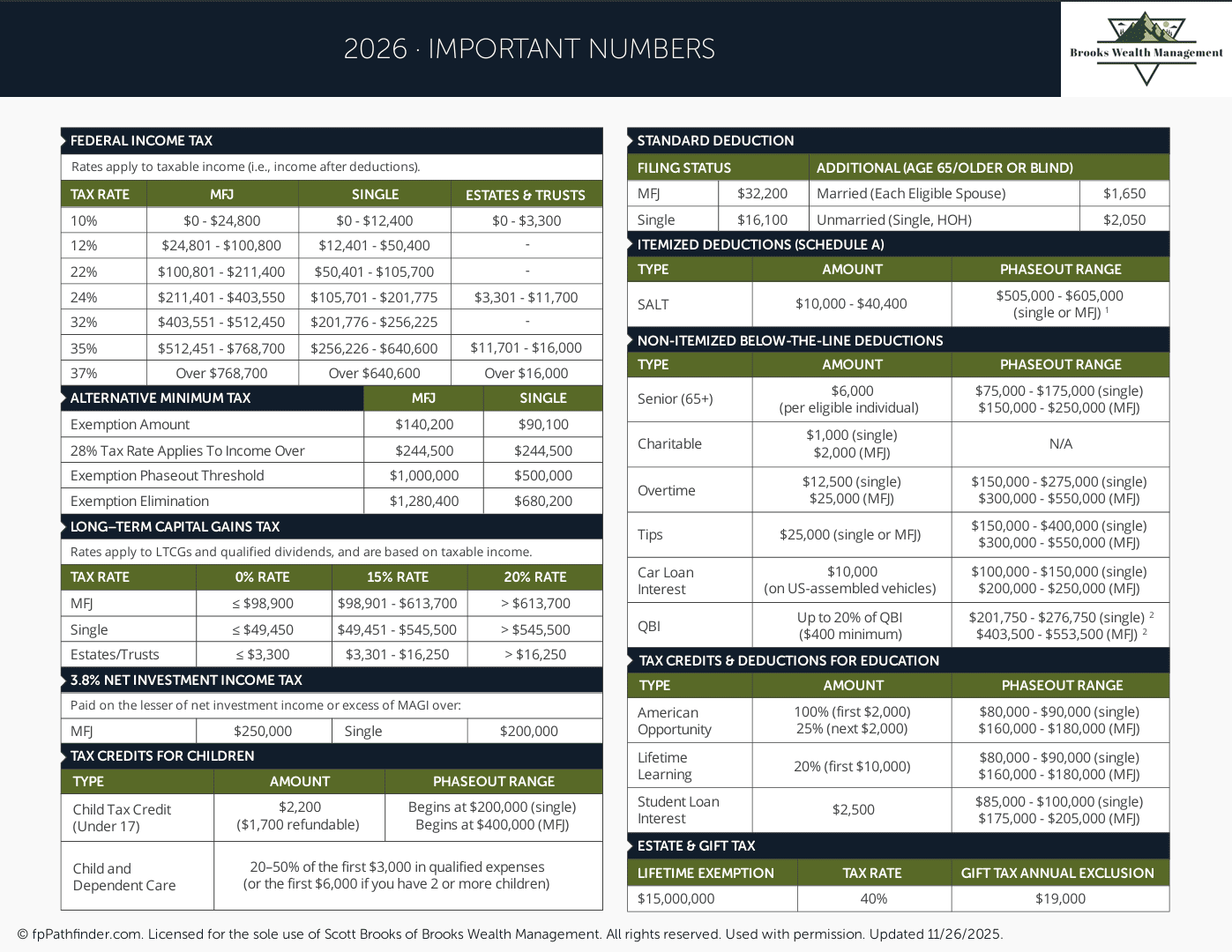

Open Video →Get the 2026 Important Numbers

A quick-reference guide for the planning numbers that tend to matter throughout the year.

Send me the guide.

Enter your name and email, and I'll send the 2026 Important Numbers to your inbox.

Check your inbox.

Your copy of the 2026 Important Numbers is on the way.

You'll also receive occasional planning updates. Unsubscribe anytime.

Beyond Investment Management

Investment management matters. But as life gets more complex, the bigger value often comes from coordinating the decisions around the portfolio.

| What the relationship may include | Brooks Wealth Management | Investment-Management-Only Relationship |

|---|---|---|

| Investment management | ✓ | ✓ |

| Retirement income planning | ✓ | — |

| Strategic withdrawal sequencing | ✓ | — |

| Tax planning coordination | ✓ | — |

| Roth conversion analysis | ✓ | — |

| Equity compensation and concentrated stock planning | ✓ | — |

| Cash flow and major life decisions | ✓ | — |

| Social Security and Medicare timing | ✓ | — |

| Insurance and risk review | ✓ | — |

| Estate, legacy, and beneficiary coordination | ✓ | — |

| Advice across accounts, not just what we manage | ✓ | — |

| Ongoing planning reviews as life changes | ✓ | — |

This comparison is intended to show the difference between a planning-first relationship and a narrower relationship limited to investment management. Other advisors and firms may offer different services, structures, and planning support.

This comparison is intended to show the difference between a planning-first relationship and a narrower relationship limited to investment management. Other advisors and firms may offer different services, structures, and planning support.