Common Retirement Plans for Small Business Owners

Reference guide comparing retirement plan options available to small business owners.

Understanding Common Retirement Plans for Small Business Owners

As a small business owner, planning for your retirement can feel like a complex endeavor, especially when balancing the demands of running your company with your personal financial goals. However, establishing a robust retirement plan is crucial for securing your future and can also offer significant tax advantages for both you and your employees. This guide will walk you through the **common retirement plans for small business owners**, helping you understand the options available and how to choose the best fit for your unique situation.

At Brooks Wealth Management, we understand the specific challenges and opportunities that small business owners face. Our goal is to provide clear, actionable advice that empowers you to make informed decisions about your financial well-being. Let's explore the various retirement plan structures designed with small businesses in mind.

Key Considerations When Choosing Retirement Plans for Small Business Owners

Before diving into the specifics of each plan, it's important to consider several factors that will influence your decision. These include the size of your business, your budget for contributions, your desire for administrative simplicity, and whether you want to offer benefits to employees. The right choice among the **common retirement plans for small business owners** will align with your business's growth trajectory and your personal retirement aspirations.

- Business Size: Some plans are better suited for solo entrepreneurs, while others are designed for businesses with multiple employees.

- Contribution Flexibility: Do you want to contribute a fixed amount each year, or do you need the flexibility to adjust contributions based on your business's profitability?

- Administrative Burden: Some plans require more administrative effort and compliance testing than others.

- Employee Participation: Will you be the only participant, or do you plan to include employees? If so, what level of contribution do you want to offer them?

- Tax Advantages: All qualified retirement plans offer tax benefits, but the specifics can vary.

Understanding these considerations will help narrow down the options and make the selection process more efficient. For a personalized assessment, consider reaching out to our team at Brooks Wealth Management.

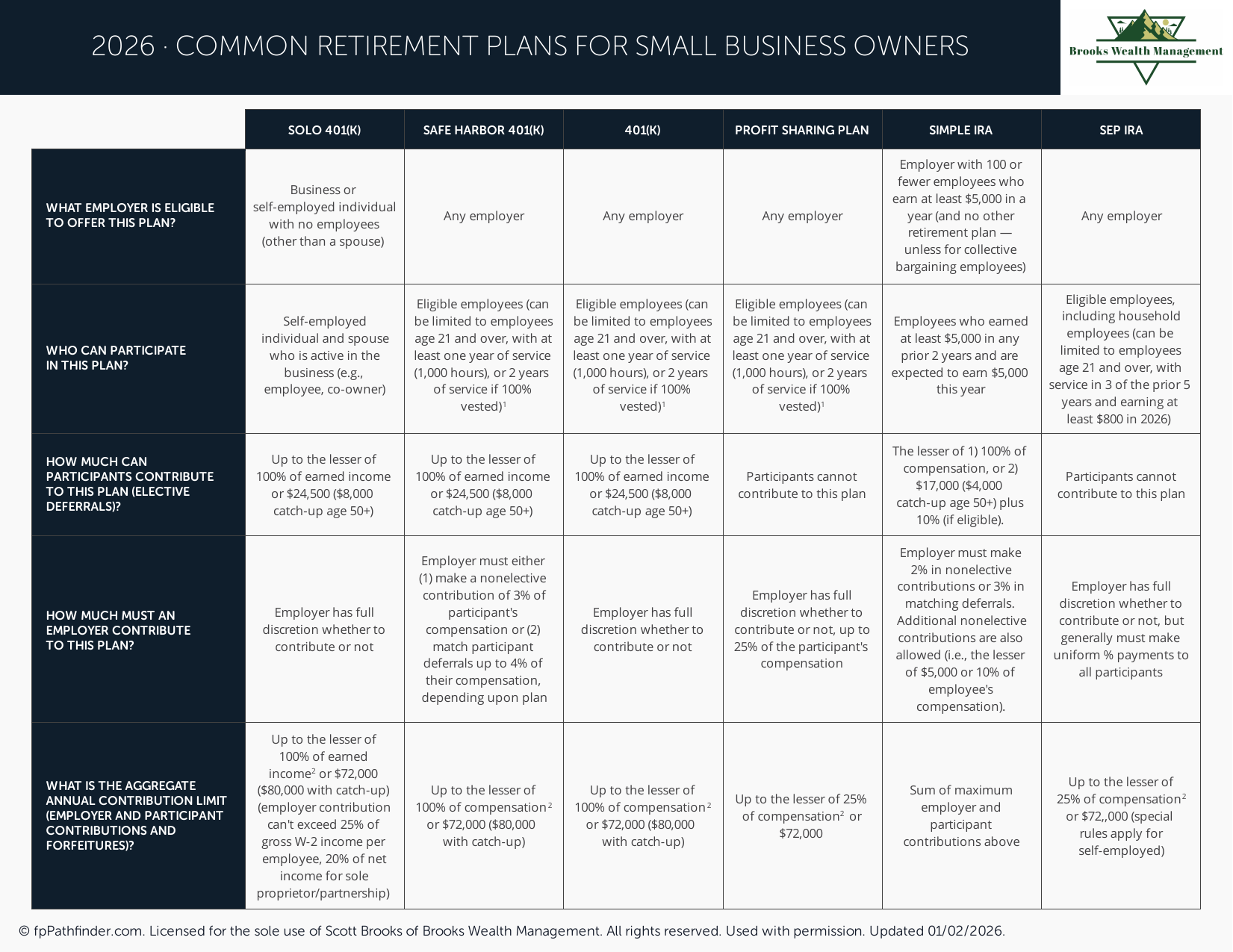

Simplified Employee Pension (SEP) IRA: A Popular Choice

The **SEP IRA** is one of the most straightforward and popular **common retirement plans for small business owners**, particularly for sole proprietors and businesses with a few employees. It allows employers to contribute to traditional IRAs set up for themselves and their eligible employees. Contributions are made solely by the employer, and they are tax-deductible for the business.

Key features of a SEP IRA:

- High Contribution Limits: In 2026, you can contribute up to 25% of an employee's compensation (or 20% of your net self-employment earnings) or $73,000, whichever is less.

- Easy to Set Up and Administer: Minimal paperwork and no annual IRS filings (Form 5500) are typically required.

- Flexibility: Employers can vary contributions each year, even contributing nothing in less profitable years.

- Employee Eligibility: Generally, employees aged 21 or older who have worked for the employer in at least three of the last five years and earned at least $750 (indexed for inflation) must be included.

While SEP IRAs offer simplicity and high contribution limits, they require employers to contribute the same percentage of pay for all eligible employees, including themselves. This can be a drawback if you wish to contribute more for yourself than for your employees.

SIMPLE IRA: Balancing Simplicity and Employee Benefits

The **SIMPLE IRA** (Savings Incentive Match Plan for Employees of Small Employers) is another excellent option among the **common retirement plans for small business owners** with 100 or fewer employees. It offers a balance between ease of administration and providing a valuable benefit to employees, as both employers and employees can contribute.

Key features of a SIMPLE IRA:

- Employee Contributions: Employees can contribute up to $16,500 in 2026, with an additional catch-up contribution of $3,500 for those aged 50 and over.

- Mandatory Employer Contributions: Employers must either match employee contributions dollar-for-dollar up to 3% of their compensation or make a non-elective contribution of 2% of each eligible employee's compensation (up to the annual limit), regardless of whether the employee contributes.

- Lower Administrative Costs: Similar to SEP IRAs, SIMPLE IRAs have fewer administrative requirements than 401(k) plans.

- No Discrimination Testing: These plans are exempt from complex nondiscrimination testing.

A SIMPLE IRA can be a good stepping stone for small businesses looking to offer a retirement plan without the complexities of a full-fledged 401(k). If you're considering how to save more for retirement, you might also explore other account types.

Solo 401(k): Maximize Contributions for Self-Employed

For self-employed individuals or business owners with no full-time employees other than themselves or a spouse, the **Solo 401(k)** (also known as an Individual 401(k) or Uni-k) is arguably the most powerful of the **common retirement plans for small business owners**. It allows you to contribute in two capacities: as both an employee and an employer.

Key features of a Solo 401(k):

- Dual Contribution Power: As an employee, you can contribute up to $23,000 in 2026 (or $30,500 if age 50 or older) as an elective deferral. As an employer, you can make a profit-sharing contribution of up to 25% of your compensation.

- Very High Contribution Limits: The combined employee and employer contributions can reach up to $69,000 in 2026 (or $76,500 if age 50 or older).

- Loan Provision: Unlike IRAs, a Solo 401(k) may allow you to borrow from your plan.

- Roth Option: Many Solo 401(k)s offer a Roth contribution option, allowing for tax-free withdrawals in retirement. If you're curious about the benefits of Roth accounts, you might want to read our article on Roth conversions or contributing to a Roth 401(k).

The Solo 401(k) is ideal for maximizing your retirement savings when you are the sole participant. However, if you hire full-time employees, you would generally need to convert it to a traditional 401(k) plan, which comes with more administrative responsibilities.

Traditional 401(k): Comprehensive Benefits for Growing Businesses

For small businesses with multiple employees, a **Traditional 401(k)** plan offers the most comprehensive benefits, though it also comes with the highest administrative complexity. It allows both employers and employees to contribute, and it can be designed with various features, including matching contributions, profit-sharing, and vesting schedules.

Key features of a Traditional 401(k):

- High Employee Contribution Limits: Employees can contribute up to $23,000 in 2026, with an additional catch-up contribution of $7,500 for those aged 50 and over.

- Employer Contributions: Employers can make discretionary matching or profit-sharing contributions.

- Roth 401(k) Option: Many plans offer a Roth 401(k) option, allowing employees to make after-tax contributions that grow tax-free.

- Flexibility in Design: Can be customized to meet specific business and employee needs, including vesting schedules for employer contributions.

- Potential for Tax Credits: Small businesses may be eligible for tax credits to help offset the costs of setting up and administering a 401(k) plan.

While a Traditional 401(k) requires more administrative effort, including annual compliance testing and IRS Form 5500 filings, it provides the most robust retirement savings vehicle for a growing business and its employees. For a deeper dive into retirement planning strategies, especially as you approach your golden years, consider our resources on pre-retirement considerations.

Choosing the Right Plan for Your Business

Selecting the right retirement plan is a critical decision for any small business owner. The best choice among the **common retirement plans for small business owners** depends on your specific circumstances, including your business structure, number of employees, desired contribution levels, and administrative preferences. Whether you opt for the simplicity of a SEP IRA, the balance of a SIMPLE IRA, the maximizing power of a Solo 401(k), or the comprehensive benefits of a Traditional 401(k), establishing a plan is a vital step toward financial security.

We encourage you to review your options carefully and consider how each plan aligns with your long-term financial goals. For further guidance on optimizing your retirement strategy or to discuss other financial planning needs, such as debt management or mortgage refinancing, please visit our free resources page.

About This Resource

This article provides general information about common retirement plans for small business owners and is not intended as personalized financial advice. For tailored guidance on your specific situation, we invite you to book a consultation with the expert team at Brooks Wealth Management. Visit our contact page to schedule your appointment today.

Have Questions About Your Situation?

This resource is a starting point. A free consultation with Scott Brooks, CFP® gives you a personalized perspective.

Book a Free ConsultationBased in Westlake Village, CA · Ventura County · Serving clients across all 50 states

Brooks Wealth Management is a Registered Investment Adviser (RIA) in the State of California. Registration does not imply a certain level of skill or training. This resource is provided for educational and informational purposes only and does not constitute investment, tax, or legal advice. Scott Brooks, CFP® · CRD #7227609 · Firm CRD #332237 · 2555 Townsgate Rd STE 200, Westlake Village, CA 91361