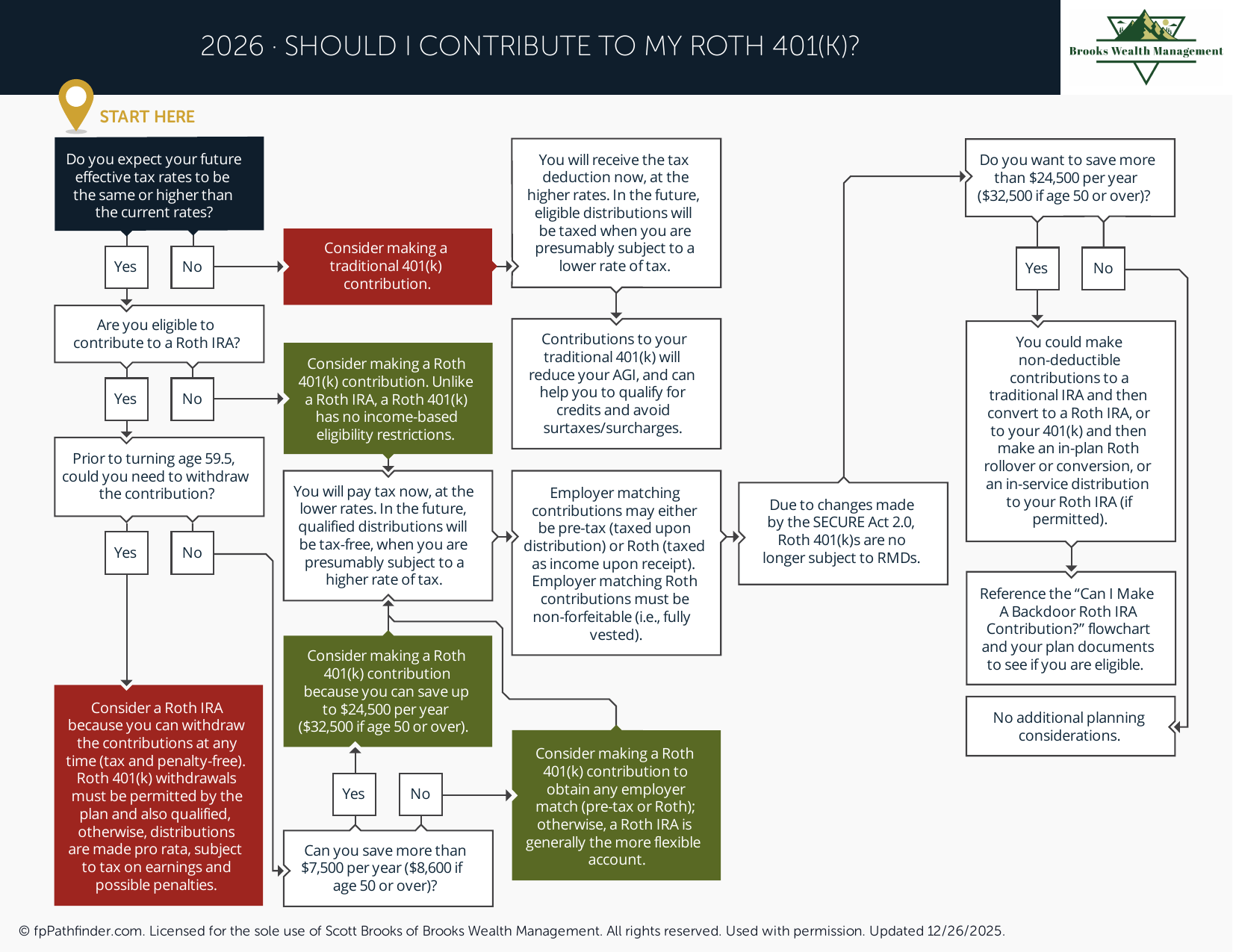

Should I Contribute to My Roth 401(k)?

Decision flowchart to determine whether Roth 401(k) contributions are right for you.

Should I Contribute to a Roth 401(k) or a Traditional 401(k)?

If your employer offers both Roth and Traditional 401(k) contribution options, one of the most important retirement planning decisions is determining how contributions should be allocated. While both accounts allow tax-advantaged retirement savings, the tax treatment differs significantly and may affect future retirement income, tax planning flexibility, and long-term financial goals.

The decision is often less about which account is universally better and more about how each option fits within your current tax situation, expected future income, retirement timeline, and broader financial plan.

Review How a Traditional 401(k) Works

Traditional 401(k) contributions are generally made on a pre-tax basis. Contributions reduce current taxable income, investment earnings grow tax-deferred, and withdrawals are generally taxed as ordinary income in retirement.

Common features include:

- Current-year tax deduction.

- Tax-deferred investment growth.

- Reduced taxable income today.

- Ordinary income taxation on future withdrawals.

- Required minimum distributions during retirement.

Individuals often review whether receiving a tax benefit today aligns with their current financial and tax planning objectives.

Review How a Roth 401(k) Works

Roth 401(k) contributions are generally made with after-tax dollars. Contributions do not reduce taxable income today, but qualified withdrawals in retirement may be tax-free.

Common features include:

- After-tax contributions.

- Tax-free growth potential.

- Tax-free qualified withdrawals.

- No current-year tax deduction.

- Potential retirement tax diversification.

Many individuals review whether paying taxes today in exchange for future tax-free income aligns with their long-term retirement planning goals.

Review Your Current Tax Situation

Current tax rates are often one of the primary factors when evaluating Roth versus Traditional contributions.

Common considerations include:

- Current marginal tax bracket.

- State income taxes.

- Expected future income growth.

- Business ownership considerations.

- Current taxable income levels.

Individuals often evaluate whether today's tax rate is likely to be higher, lower, or similar to future retirement tax rates.

Review Expected Retirement Tax Rates

Future tax rates are uncertain, but they remain a key consideration when evaluating retirement contribution strategies.

Common questions include:

- Will retirement income be lower than current income?

- Will future tax laws change?

- Will Social Security and retirement distributions create taxable income?

- Will required minimum distributions increase future taxes?

- Will future tax-free income be valuable?

Because future tax rates cannot be predicted with certainty, many individuals evaluate multiple scenarios when making contribution decisions.

Review Retirement Tax Diversification

Some individuals choose to maintain both Roth and pre-tax retirement assets to increase future planning flexibility.

Common considerations include:

- Managing retirement tax brackets.

- Controlling taxable income.

- Reducing reliance on a single account type.

- Planning for future tax law changes.

- Creating withdrawal flexibility.

Having access to both taxable and tax-free retirement income sources may provide additional options during retirement.

Review Time Horizon Considerations

The amount of time until retirement may affect how individuals evaluate Roth versus Traditional contributions.

Common considerations include:

- Years until retirement.

- Expected investment growth period.

- Long-term compounding opportunities.

- Retirement savings objectives.

- Future income expectations.

Individuals often review how long assets may remain invested before distributions are expected.

Review Required Minimum Distribution Considerations

Required minimum distributions may affect retirement income planning.

Common considerations include:

- Future required distributions.

- Retirement tax planning.

- Income management strategies.

- Legacy planning objectives.

- Long-term withdrawal flexibility.

Understanding how future distributions may affect retirement income is often part of the Roth versus Traditional contribution decision.

Review Roth Conversion Opportunities

Individuals making Traditional 401(k) contributions sometimes evaluate whether future Roth conversions may be appropriate.

Common considerations include:

- Current versus future tax rates.

- Retirement income planning.

- Low-income years.

- Tax diversification goals.

- Long-term tax planning opportunities.

Additional information is available in our guide discussing Roth conversion considerations.

Review Questions Before Choosing Roth or Traditional Contributions

Individuals often review the following questions when evaluating contribution options:

- Is a tax deduction today more valuable than potential tax-free income later?

- What is my current tax bracket?

- What tax rates might apply in retirement?

- How important is future tax flexibility?

- Would a combination approach provide greater diversification?

These questions can help frame the decision before selecting a contribution strategy.

Additional retirement savings considerations can be found in our resources discussing Roth IRA versus Traditional IRA considerations and accounts to consider when saving more.

Review How the Decision Fits Into Your Overall Financial Plan

The choice between Roth and Traditional 401(k) contributions is often evaluated within the context of a broader financial plan.

Common considerations include:

- Retirement income objectives.

- Tax planning goals.

- Investment strategy.

- Estate planning considerations.

- Long-term wealth accumulation goals.

Because retirement account decisions may affect taxes, retirement income, and future planning flexibility, many individuals evaluate contribution choices alongside their broader financial objectives.

About This Resource

This resource provides general educational information regarding Roth 401(k) plans, Traditional 401(k) plans, retirement contribution strategies, and related retirement planning considerations. Both account types can provide meaningful retirement savings opportunities, but they differ in tax treatment, withdrawal rules, retirement income planning implications, and long-term flexibility.

Individuals often review Roth versus Traditional contribution decisions alongside broader retirement planning, tax planning, and wealth management objectives. The appropriate contribution strategy depends on factors such as current income, expected future tax rates, retirement goals, and overall financial circumstances.

This resource is intended to provide a framework for understanding common Roth 401(k) versus Traditional 401(k) considerations. It is not intended as investment, tax, legal, insurance, healthcare, cybersecurity, or financial advice. Individual circumstances vary, and applicable rules may change over time.

If you would like to discuss how this topic fits into your broader financial plan, we invite you to schedule an introductory conversation.