Will I Be Enrolled Automatically in Medicare?

Flowchart to determine whether you will be automatically enrolled in Medicare at age 65.

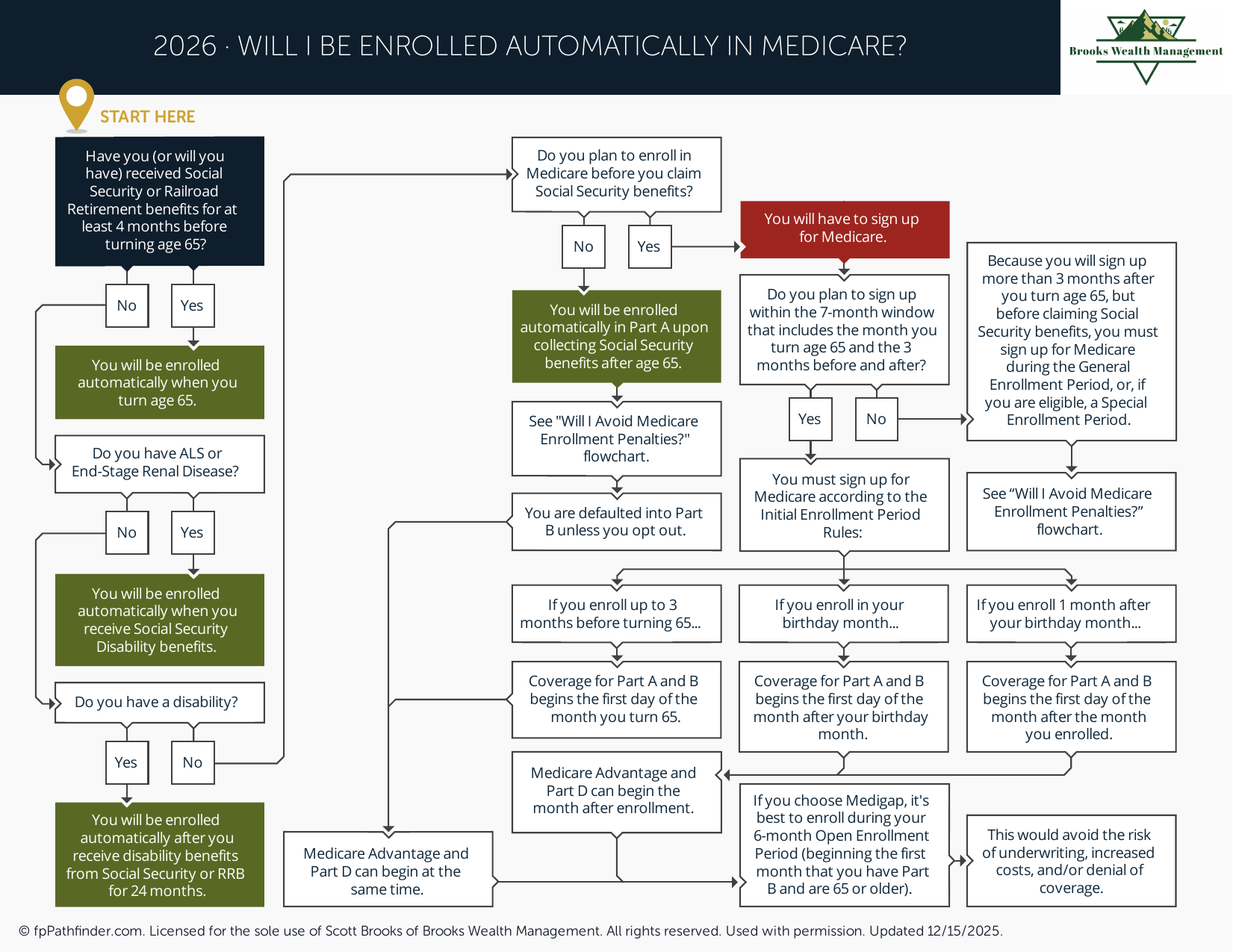

Will I Be Automatically Enrolled in Medicare?

Many individuals approaching age 65 wonder whether Medicare enrollment happens automatically or whether they need to actively enroll. The answer depends largely on whether you are already receiving Social Security or Railroad Retirement Board benefits when you become eligible for Medicare.

Understanding Medicare automatic enrollment can help you avoid coverage gaps, enrollment delays, and potential Medicare penalties. While some individuals are enrolled automatically, others must take action during their enrollment window to begin coverage.

Are You Already Receiving Social Security Benefits?

If you are already receiving Social Security retirement benefits at least four months before your 65th birthday, Medicare enrollment is generally automatic. In most situations, you will be enrolled in both Medicare Part A (Hospital Insurance) and Medicare Part B (Medical Insurance).

Your Medicare card is typically mailed approximately three months before your coverage begins. For many retirees, this creates a seamless transition into Medicare because no separate enrollment application is required.

This is one reason why Medicare enrollment experiences can vary significantly. Two individuals turning 65 at the same time may have very different enrollment requirements depending on whether they have already started receiving Social Security benefits.

Are You Receiving Social Security Disability Benefits?

Individuals receiving Social Security Disability Insurance (SSDI) benefits are generally enrolled in Medicare automatically after receiving disability benefits for 24 months. Medicare coverage typically begins during the 25th month of disability benefits.

As with retirement-based enrollment, Medicare cards are generally mailed before coverage begins. However, beneficiaries should still review their coverage choices, particularly regarding prescription drug coverage and supplemental insurance options.

Are You Delaying Social Security Benefits?

Many individuals choose to delay Social Security benefits beyond age 65. In these situations, Medicare enrollment generally does not occur automatically.

This is a common situation among professionals and business owners who continue working or who plan to delay Social Security benefits until Full Retirement Age or age 70. While Social Security and Medicare are closely connected, delaying one does not automatically delay the other.

If you are not receiving Social Security benefits, you may need to actively enroll in Medicare during your Initial Enrollment Period. This enrollment window begins three months before the month you turn 65, includes your birth month, and extends for three months afterward.

For additional information, review our resource on Medicare Part A and Part B eligibility.

Do You Have Employer Health Coverage?

One of the most common Medicare questions involves individuals who continue working beyond age 65. In many cases, employer-sponsored health insurance remains available, creating additional Medicare planning considerations.

Depending on the size of your employer and the structure of your health plan, you may qualify for a Special Enrollment Period that allows you to delay certain Medicare coverage without penalties. However, these rules can be complex, and eligibility often depends on whether the employer coverage meets Medicare requirements.

Many individuals mistakenly assume that any health insurance allows them to delay Medicare enrollment. In reality, the rules can differ depending on employer size, plan structure, and employment status. Reviewing these details before making enrollment decisions can help avoid future coverage issues.

Should You Keep Medicare Part B?

Even when Medicare enrollment occurs automatically, individuals may still evaluate whether Medicare Part B is necessary immediately.

This commonly arises when someone remains employed and covered by an employer-sponsored health plan. Because Medicare Part B requires a monthly premium, some individuals review whether delaying Part B enrollment is appropriate based on their existing coverage.

However, delaying Part B without qualifying coverage can result in future enrollment penalties and delayed access to benefits. Understanding whether your current coverage is considered creditable is an important part of the decision-making process.

For additional guidance, review our resource on Medicare enrollment penalties.

Other Medicare Decisions to Review

Automatic enrollment is only one part of the Medicare planning process. Individuals approaching age 65 often review several additional healthcare decisions, including:

- Medicare Part D prescription drug coverage

- Medicare Advantage plans

- Medigap supplemental coverage

- Healthcare costs in retirement

- Income-related Medicare premium surcharges (IRMAA)

For higher-income retirees, Medicare premiums may be affected by income reported on prior tax returns. Understanding how retirement income, capital gains, Roth conversions, and other planning decisions interact with Medicare costs can be an important part of retirement planning.

You may also find our resources on healthcare in retirement, retirement planning considerations, and Social Security benefits helpful.

About This Resource

This resource provides general educational information regarding Medicare automatic enrollment. It is not intended as healthcare, tax, legal, or financial advice. Medicare rules may change, and individual circumstances vary.

If you would like to discuss retirement planning, Medicare decisions, or other financial planning considerations, we invite you to schedule an introductory conversation.