What Issues Should I Consider with the Income from My Taxable (Non-Qualified) Accounts?

Checklist of tax planning considerations for income and gains generated in taxable investment accounts.

As a high-income professional, business owner, or Gen X/Y client, you likely have a diversified investment portfolio. A significant component of this might be your **taxable non-qualified account income**. Understanding the nuances of this income is crucial for effective financial planning and tax optimization.

At Brooks Wealth Management, we often guide clients through the complexities of managing investments outside of traditional retirement accounts. These non-qualified accounts offer flexibility but come with specific tax implications that demand careful consideration.

Understanding Taxable Non-Qualified Account Income

When we talk about **taxable non-qualified account income**, we're referring to earnings generated from investment accounts that do not receive special tax treatment, unlike 401(k)s, IRAs, or HSAs. This typically includes brokerage accounts, mutual funds held outside of retirement wrappers, and other similar investment vehicles. The income generated from these accounts can come in various forms, such as interest, dividends, and capital gains.

The key distinction is that these accounts are funded with after-tax dollars, and their earnings are generally subject to taxation in the year they are realized, rather than being deferred until retirement. This immediate taxability makes strategic management of your **taxable non-qualified account income** paramount.

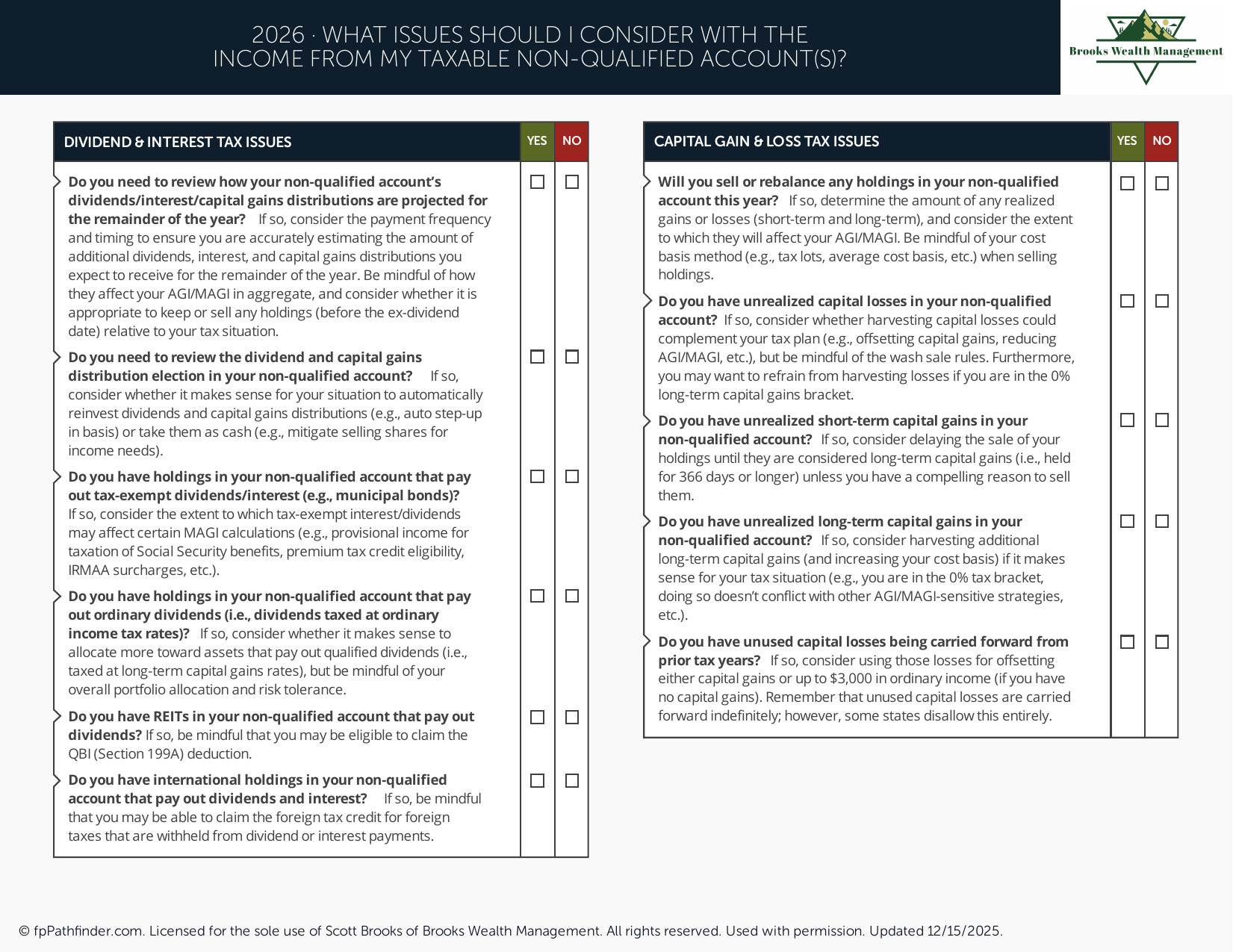

Key Tax Considerations for Your Non-Qualified Account

Managing the tax implications of your non-qualified accounts is a cornerstone of smart financial planning. Here are the primary issues to consider:

- Ordinary Income vs. Qualified Dividends: Interest income from bonds or certain money market accounts is taxed as ordinary income, at your marginal tax rate. Qualified dividends, however, from eligible domestic and certain foreign corporations, are taxed at lower long-term capital gains rates. Understanding this distinction can significantly impact your after-tax returns.

- Short-Term vs. Long-Term Capital Gains: When you sell an investment in a non-qualified account for a profit, you realize a capital gain. If you held the asset for one year or less, it's a short-term capital gain, taxed at your ordinary income rate. If held for more than a year, it's a long-term capital gain, subject to more favorable rates. Strategic timing of sales is vital.

- Tax-Loss Harvesting: This is a powerful strategy to offset capital gains and even a limited amount of ordinary income. By selling investments at a loss, you can reduce your taxable income. This can be particularly effective when managing your **taxable non-qualified account income**. For more on optimizing your tax strategy, you might find our resources on debt management helpful, as reducing interest payments can free up capital for tax-efficient investments.

- Net Investment Income Tax (NIIT): High-income individuals may be subject to a 3.8% Net Investment Income Tax on certain investment income, including interest, dividends, and capital gains, if their modified adjusted gross income (MAGI) exceeds specific thresholds.

Strategic Management of Your Taxable Non-Qualified Account Income

Beyond understanding the tax rules, proactive management can enhance your returns. Here are some strategies we often discuss with clients:

- Asset Location: This involves deciding which types of investments to hold in which accounts. For instance, placing highly taxed investments (like bonds generating ordinary income) in tax-advantaged accounts (like a 401(k) or IRA) and tax-efficient investments (like growth stocks generating long-term capital gains) in your non-qualified accounts.

- Diversification: While not directly a tax strategy, a well-diversified portfolio helps manage risk, which indirectly protects your capital from significant losses that could impact your overall **taxable non-qualified account income**.

- Rebalancing: Regularly rebalancing your portfolio ensures it aligns with your risk tolerance and financial goals. This can also be an opportunity to realize losses for tax-loss harvesting.

- Understanding Cost Basis: Accurately tracking the cost basis of your investments is essential for calculating capital gains and losses. Different methods (e.g., FIFO, specific identification) can impact your tax liability.

Integrating Non-Qualified Accounts into Your Overall Financial Plan

Your taxable non-qualified accounts don't exist in a vacuum. They are an integral part of your broader financial picture. Consider how they interact with your retirement savings, such as when you might need to consider a Roth conversion, or how they fit into your overall savings strategy. For those nearing retirement, understanding how these accounts will provide income is critical, especially when considering pre-retirement planning.

For business owners, the income from these accounts might also play a role in business succession planning or funding future ventures. It's about creating a cohesive strategy where every component works together to achieve your long-term objectives.

The Brooks Wealth Management Approach

At Brooks Wealth Management, we believe in a holistic approach to financial planning. We don't just look at your **taxable non-qualified account income** in isolation. Instead, we integrate it into a comprehensive strategy that considers your entire financial life, including your goals, risk tolerance, and tax situation. Our aim is to help you navigate these complexities with confidence, ensuring your investments are working as efficiently as possible for you.

Whether you're just starting to build wealth or are nearing retirement, understanding and strategically managing your non-qualified accounts is key to maximizing your financial potential.

About This Resource

This resource provides general information and is not intended as personalized financial or tax advice. For tailored guidance on managing your taxable non-qualified account income and other financial planning needs, we invite you to book a consultation with our expert team. Visit brookswealthmanagement.com/contact/ to schedule your personalized session today.

Have Questions About Your Situation?

This resource is a starting point. A free consultation with Scott Brooks, CFP® gives you a personalized perspective.

Book a Free ConsultationBased in Westlake Village, CA · Ventura County · Serving clients across all 50 states

Brooks Wealth Management is a Registered Investment Adviser (RIA) in the State of California. Registration does not imply a certain level of skill or training. This resource is provided for educational and informational purposes only and does not constitute investment, tax, or legal advice. Scott Brooks, CFP® · CRD #7227609 · Firm CRD #332237 · 2555 Townsgate Rd STE 200, Westlake Village, CA 91361