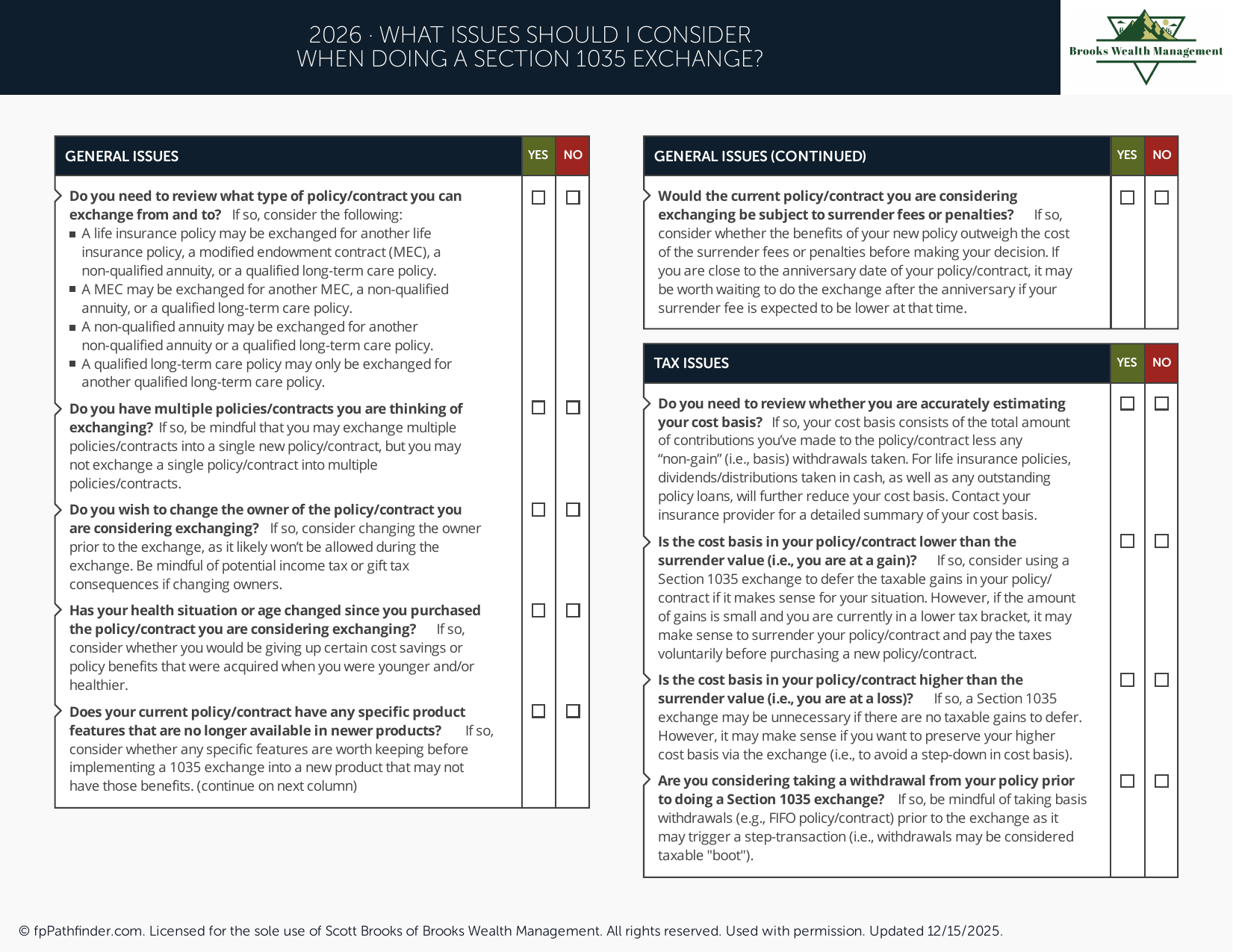

What Issues Should I Consider When Doing a Section 1035 Exchange?

Checklist of tax and planning considerations for a tax-free exchange of annuity or life insurance contracts.

What Issues Should I Consider Before Completing a Section 1035 Exchange?

A Section 1035 exchange allows certain insurance and annuity contracts to be exchanged for another qualifying contract without immediately recognizing taxable gain. This provision of the Internal Revenue Code is designed to allow policyholders to replace existing contracts while preserving tax deferral, provided specific requirements are met.

While a Section 1035 exchange may be appropriate in certain situations, it is important to evaluate the benefits, costs, risks, and tax implications before moving forward. This resource highlights several considerations that may be worth reviewing as part of that evaluation.

What Is a Section 1035 Exchange?

A Section 1035 exchange generally allows a direct exchange of one qualifying insurance or annuity contract for another qualifying contract without immediately triggering federal income tax on any gain within the original contract.

Common examples may include exchanging one annuity contract for another annuity contract or exchanging one life insurance policy for another life insurance policy. Certain exchanges involving life insurance and annuity contracts may also qualify, subject to applicable IRS rules.

To preserve tax-deferred treatment, the exchange generally must be completed directly between carriers. Receiving the proceeds personally before completing the transaction may result in different tax treatment.

Review Surrender Charges and Contract Restrictions

Before completing a Section 1035 exchange, it may be important to review any surrender charges, market value adjustments, withdrawal restrictions, or other costs associated with the existing contract.

Some insurance and annuity products impose surrender charges that can reduce the value received upon exchange. Understanding these costs can help provide a clearer picture of the economic impact of replacing an existing contract.

Contract owners may wish to request current policy illustrations, surrender schedules, or carrier disclosures before making a decision.

Compare Fees, Expenses, and Contract Features

When evaluating a potential replacement contract, it may be helpful to compare fees, expenses, investment options, riders, guarantees, death benefits, income features, and other policy provisions.

In some situations, newer contracts may offer features that differ from older policies. In other cases, existing contracts may contain benefits that would be difficult or impossible to replace. Understanding these differences may help support a more informed decision.

If you are evaluating broader savings and investment opportunities, you may find our guide on accounts to consider if you want to save more helpful.

Understand Potential Tax Considerations

Although a properly completed Section 1035 exchange is generally intended to preserve tax deferral, certain circumstances may create unintended tax consequences. For example, policy loans, withdrawals, partial exchanges, or other contract-specific provisions may affect the tax treatment of the transaction.

Because tax outcomes can vary depending on the facts and circumstances, individuals should review the transaction with qualified tax professionals before proceeding.

Understanding the tax basis of the existing contract and how that basis transfers to the replacement contract may also be an important part of the evaluation process.

Evaluate Whether the New Contract Supports Your Goals

A Section 1035 exchange should generally be evaluated within the context of broader financial goals rather than focusing exclusively on tax treatment. Factors such as retirement income needs, risk tolerance, liquidity requirements, estate planning considerations, and insurance objectives may all influence whether a replacement is appropriate.

For individuals approaching retirement, insurance and annuity decisions often interact with broader retirement planning considerations. You may also find our guide on issues to consider before retirement helpful.

Consider the Role of Insurance and Annuities Within Your Financial Plan

Insurance and annuity contracts often represent only one component of a broader financial strategy. Evaluating how a proposed exchange affects cash flow, investment allocation, retirement planning, estate planning, and risk management objectives may help provide additional context for the decision.

Depending on individual circumstances, other planning opportunities may also warrant review. For example, some individuals may evaluate tax planning strategies such as Roth conversions or review broader financial priorities such as debt management as part of a comprehensive financial plan.

When Professional Guidance May Be Helpful

Insurance contracts, annuity products, tax rules, and replacement transactions can involve complex considerations. Individuals evaluating a Section 1035 exchange may benefit from reviewing the proposed transaction with qualified tax professionals, insurance specialists, and financial advisors before making a decision.

Brooks Wealth Management works with professionals, business owners, retirees, and families on a wide range of financial planning topics, including retirement planning, tax-aware financial planning, and wealth management. You can explore additional educational content through our free resource library.

About This Resource

This resource provides general educational information regarding Section 1035 exchanges, insurance contracts, annuity contracts, and related tax planning considerations. Every individual's circumstances are different, and financial decisions should be evaluated based on personal goals, contract provisions, tax considerations, and applicable laws.

If you would like to discuss your situation, we invite you to schedule an introductory conversation.

Have Questions About Your Situation?

This resource is intended for educational purposes only. If you would like to discuss your circumstances, schedule an introductory conversation with Scott Brooks, CFP®.

Schedule an Introductory ConversationVentura County, California · Serving Clients Throughout California and Across the United States

Brooks Wealth Management is a Registered Investment Adviser registered with the State of California. Registration does not imply a certain level of skill or training. This content is provided for informational and educational purposes only and should not be construed as investment, tax, legal, or accounting advice. Advisory services are offered only to clients or prospective clients where Brooks Wealth Management and its representatives are properly licensed or exempt from licensure. Investing involves risk, including the potential loss of principal. CFP® is a certification mark owned by the Certified Financial Planner Board of Standards, Inc. Scott Brooks, CFP® · CRD #7227609 · Firm CRD #332237