What Issues Should I Consider as a Business Owner or 1099 Worker?

Checklist of tax, retirement, insurance, and financial planning considerations for self-employed individuals.

Financial Planning Considerations for Business Owners and 1099 Workers

Business owners and independent contractors often face financial planning challenges that differ from those of traditional employees. Income may fluctuate from year to year, taxes are generally more complex, and retirement planning often requires greater individual responsibility. As a result, a thoughtful approach to business owner financial planning can help coordinate personal goals, business decisions, tax considerations, and long-term wealth accumulation.

This guide highlights several financial planning topics that business owners and self-employed individuals may wish to review. Every situation is unique, and planning decisions should be evaluated based on your income, business structure, financial goals, tax circumstances, and overall resources.

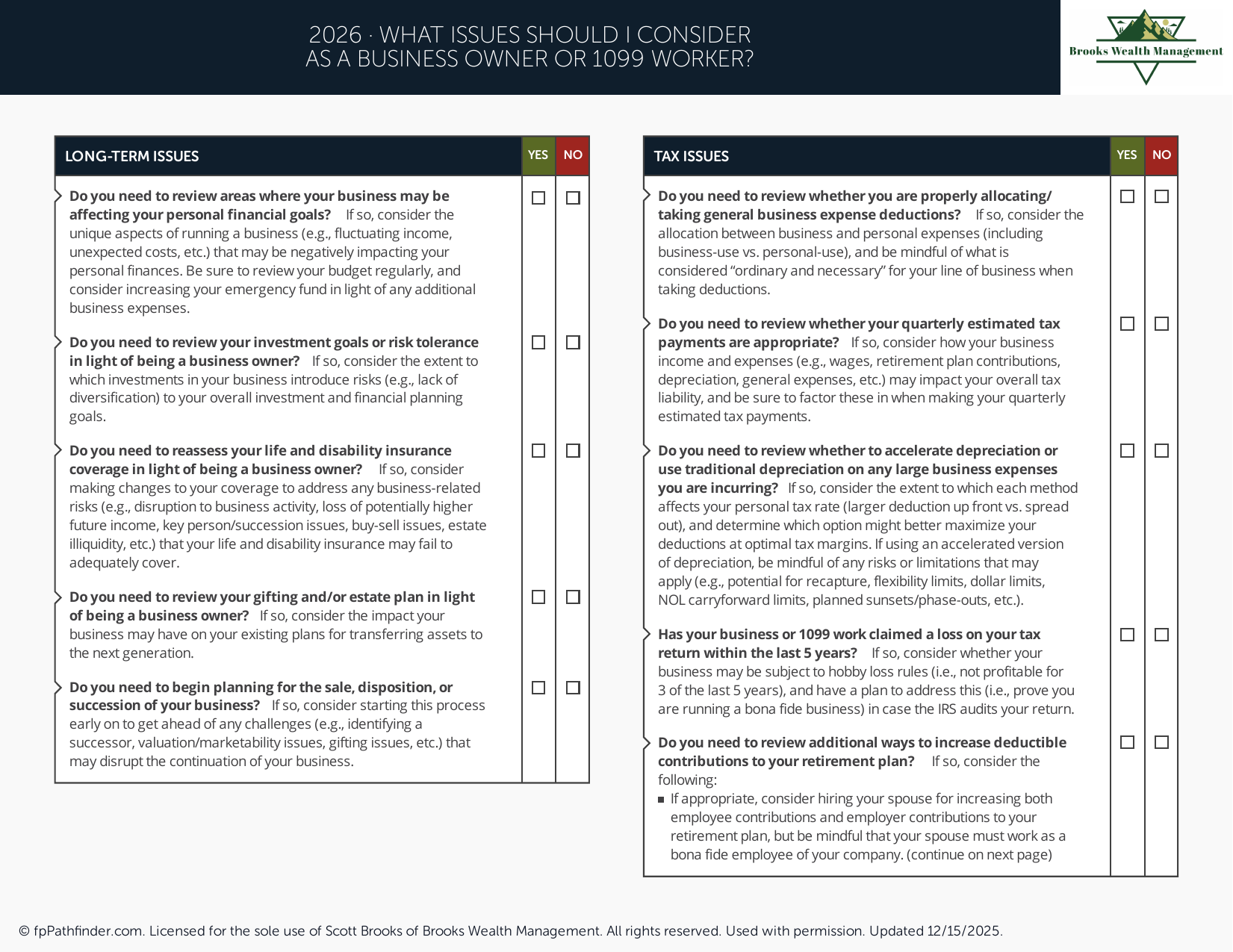

Understanding Income, Taxes, and Business Structure

Unlike many W-2 employees, business owners and 1099 workers are often responsible for managing estimated tax payments, self-employment taxes, and business-related deductions. Income may vary from year to year, making tax planning an ongoing process rather than a once-a-year event.

Reviewing your business structure, estimated tax payments, available deductions, and overall tax strategy may help improve financial organization and reduce surprises throughout the year. Depending on your circumstances, considerations may include sole proprietorship, LLC, partnership, or S corporation structures, as well as retirement plan contributions and other tax-related planning opportunities.

For additional educational resources on financial planning topics, visit our free resource library.

Retirement Planning Opportunities for Business Owners

Self-employed individuals often have access to retirement savings vehicles that may allow for substantial annual contributions. Depending on eligibility and business structure, options may include a Solo 401(k), SEP IRA, SIMPLE IRA, defined benefit plan, or other retirement arrangements.

Choosing the most appropriate retirement plan depends on several factors, including income, business profitability, employee considerations, and long-term retirement goals. Regularly reviewing retirement contribution opportunities may help align savings decisions with broader financial objectives.

If you are looking to increase retirement savings, you may find our guide on what accounts to consider if you want to save more helpful. You may also wish to review our resource on Roth 401(k) versus traditional retirement contributions.

Managing Cash Flow and Maintaining Financial Flexibility

Because business income can fluctuate, many business owners prioritize maintaining adequate cash reserves for both personal and business needs. Establishing emergency savings and monitoring cash flow may help provide flexibility during periods of lower revenue, unexpected expenses, or business transitions.

Cash flow planning can also help business owners evaluate spending decisions, tax obligations, debt repayment strategies, and savings goals. Maintaining a clear understanding of available liquidity may reduce financial stress during periods of uncertainty.

Insurance, Estate Planning, and Asset Protection Considerations

Business owners often have personal and business financial interests that are closely connected. Reviewing insurance coverage, including health, disability, liability, and life insurance, may be an important part of a broader risk management strategy.

Estate planning considerations may also become increasingly important as business value grows. Depending on your circumstances, this may involve wills, trusts, powers of attorney, beneficiary designations, and succession planning considerations. Reviewing these areas periodically may help ensure planning documents remain aligned with your goals.

For additional information, you may find our estate planning guide helpful.

Investment Planning and Long-Term Wealth Accumulation

In addition to retirement plans, many business owners build wealth through taxable investment accounts, real estate, business reinvestment, and other financial assets. Determining how much capital to retain in the business versus investing outside the business is often an important planning decision.

A diversified investment strategy may help align investment decisions with your risk tolerance, time horizon, liquidity needs, and long-term financial objectives. Reviewing investment allocations periodically can help ensure your portfolio continues to reflect your evolving goals and circumstances.

For individuals exploring tax planning opportunities, our resource on whether to consider a Roth conversion may provide additional context. If retirement planning is a current priority, you may also find value in our guide on what issues to consider before retirement.

About This Resource

This resource provides general educational information regarding financial planning considerations for business owners and self-employed individuals, including taxes, retirement planning, cash flow management, insurance, estate planning, and investment decisions. Every individual's circumstances are different, and financial strategies should be evaluated based on personal goals, business needs, tax considerations, and available resources.

Brooks Wealth Management works with professionals, business owners, retirees, and families on a wide range of financial planning topics. If you would like to discuss your situation, we invite you to schedule an introductory conversation or learn more about our approach on our pricing page.

Have Questions About Your Situation?

This resource is intended for educational purposes only. If you would like to discuss your circumstances, schedule an introductory conversation with Scott Brooks, CFP®.

Schedule an Introductory ConversationVentura County, California · Serving Clients Throughout California and Across the United States

Brooks Wealth Management is a Registered Investment Adviser registered with the State of California. Registration does not imply a certain level of skill or training. This content is provided for informational and educational purposes only and should not be construed as investment, tax, legal, or accounting advice. Advisory services are offered only to clients or prospective clients where Brooks Wealth Management and its representatives are properly licensed or exempt from licensure. Investing involves risk, including the potential loss of principal. CFP® is a certification mark owned by the Certified Financial Planner Board of Standards, Inc. Scott Brooks, CFP® · CRD #7227609 · Firm CRD #332237