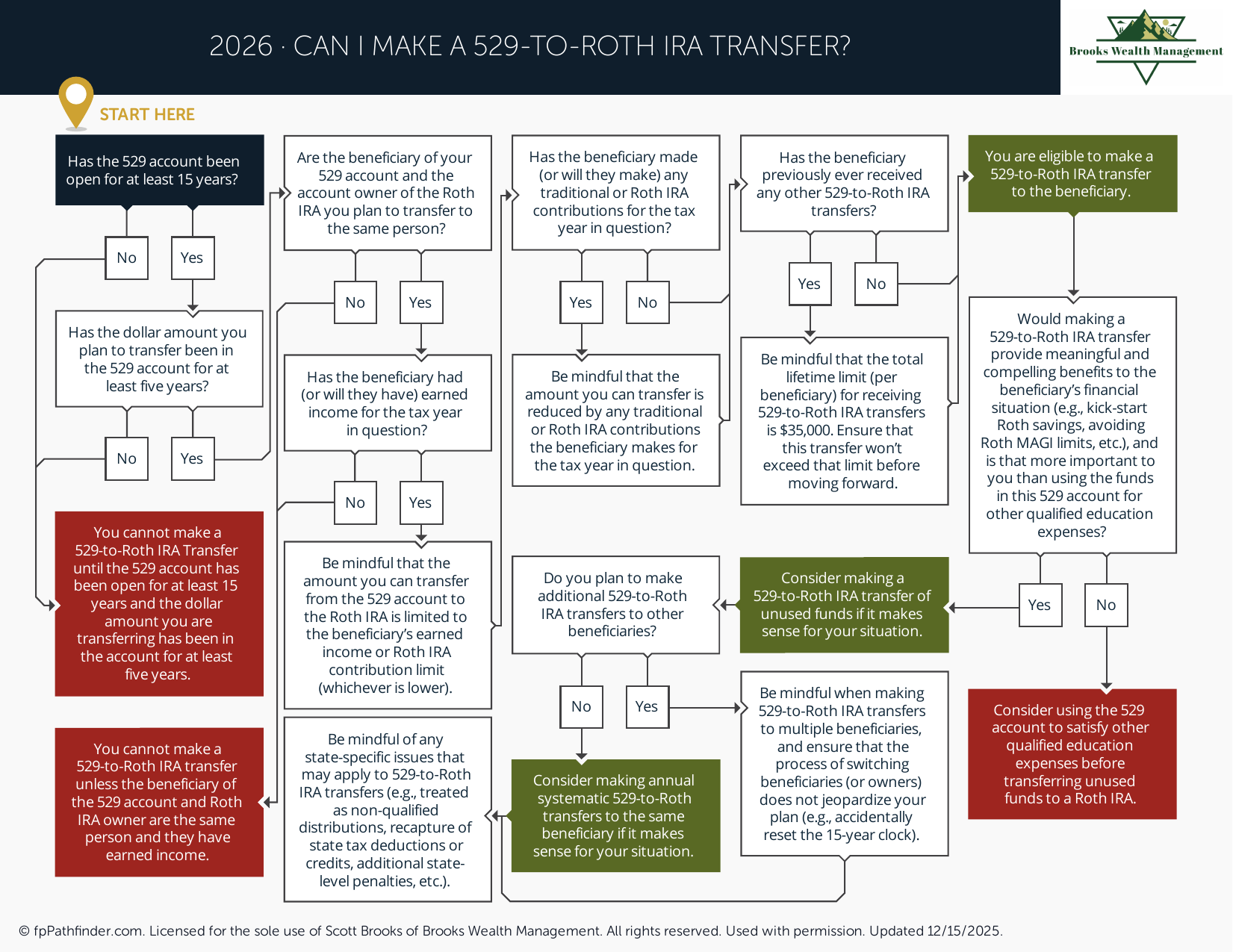

Can I Make a 529-to-Roth Transfer?

Flowchart to determine eligibility and rules for rolling over unused 529 funds to a Roth IRA.

Can I Make a 529-to-Roth Transfer?

The ability to transfer certain unused 529 plan assets to a Roth IRA has created new planning opportunities for families who have accumulated education savings that may no longer be needed for educational expenses. While the concept appears straightforward, several eligibility requirements and limitations must be satisfied before a transfer can occur.

This decision flowchart is designed to help you evaluate whether a 529-to-Roth transfer may be available in your situation. Understanding the applicable rules can help families review unused education savings, evaluate available options, and avoid unintended tax or reporting issues.

Review Why a 529-to-Roth Transfer May Be Considered

Historically, one concern associated with 529 plans was the possibility of accumulating more education savings than ultimately needed. Educational plans can change, scholarships may reduce costs, or students may pursue alternative educational paths that require less funding than originally anticipated.

As a result, some families have been concerned about maintaining flexibility when contributing to education savings accounts.

The introduction of 529-to-Roth transfer provisions provides an additional option that may be available in certain situations. Rather than withdrawing funds for non-educational purposes, eligible account owners and beneficiaries may have the ability to move a portion of unused assets into a Roth IRA if specific requirements are met.

This change has made 529 plans more flexible for some families, but eligibility depends on several important factors.

Review Basic Eligibility Requirements

A 529-to-Roth transfer is not automatically available simply because a 529 plan contains unused funds. Various eligibility requirements generally apply before a transfer can occur.

Questions commonly addressed include:

- Has the 529 plan been established long enough to satisfy applicable requirements?

- Is the intended Roth IRA owner the appropriate beneficiary?

- Are the assets eligible for transfer under current rules?

- Has the transfer amount been calculated correctly?

- Are annual contribution limitations being considered?

Because multiple requirements must often be satisfied simultaneously, reviewing the details carefully before initiating a transfer can be important.

Review Beneficiary Considerations

The beneficiary of the 529 plan often plays a central role in determining whether a transfer may be available. In many cases, the Roth IRA receiving the funds must be associated with the beneficiary connected to the education account.

Families may wish to consider:

- Whether the beneficiary remains the same individual originally designated on the account

- Whether beneficiary changes have occurred over time

- How future educational needs may affect the decision

- Whether retaining funds inside the 529 plan may provide additional flexibility

Because beneficiary designations can influence eligibility and planning opportunities, they are often reviewed as part of the overall decision-making process.

Additional resources that may be helpful include What Issues Should I Consider When Reviewing My Beneficiaries? and How Should I Fund My Child's College Education?.

Review Contribution and Transfer Limitations

Even when a transfer is permitted, limitations may apply regarding how much can be moved and when transfers can occur. Families often discover that eligibility alone does not necessarily mean the entire account balance can be transferred immediately.

Areas commonly reviewed include:

- Lifetime transfer limitations that may apply

- Annual Roth IRA contribution constraints

- Coordination with other Roth IRA contributions

- Timing requirements associated with transfers

- Recordkeeping and documentation considerations

Understanding these limitations can help establish realistic expectations regarding how a transfer strategy may be implemented over time.

Review Potential Planning Opportunities

For some families, the ability to move unused education savings into a Roth IRA may create additional flexibility within a broader financial plan. Depending on the circumstances, a transfer may provide an alternative to leaving excess funds unused or withdrawing assets for non-qualified purposes.

Potential planning considerations may include:

- Excess education savings after graduation

- Scholarships that reduce anticipated education costs

- Changes in educational plans

- Long-term retirement savings opportunities for beneficiaries

- Coordination with other savings goals

The availability of these transfers does not necessarily mean a transfer is always the preferred choice. Instead, it represents one option that may warrant evaluation alongside other alternatives.

Review Recordkeeping and Documentation

Like many tax-related planning strategies, documentation can play an important role in supporting eligibility and compliance with applicable rules.

Records that may be useful to maintain include:

- 529 account statements

- Contribution history

- Beneficiary records

- Transfer documentation

- Roth IRA contribution records

- Relevant tax forms and supporting materials

Accurate records may help simplify future reporting and provide support if questions arise regarding a transfer.

Review How 529 Planning Fits Into Your Broader Financial Plan

Education funding decisions rarely exist in isolation. Choices regarding 529 plans often intersect with retirement planning, estate planning, tax planning, and broader family financial goals.

Families reviewing unused education savings may also find value in evaluating how those assets fit into their overall financial picture.

Additional resources that may be helpful include Where Should My Next Dollar Go?, What Accounts Should I Consider If I Want to Save More?, and Is the Distribution From My 529 Plan Subject to Federal Income Tax?.

About This Resource

This decision flowchart was created to help individuals and families evaluate whether a 529-to-Roth transfer may be available under current rules. The objective is to provide a structured framework for reviewing common considerations such as eligibility requirements, beneficiary status, transfer limitations, recordkeeping requirements, and broader financial planning implications.

Every situation is unique. Factors such as account history, beneficiary information, contribution timing, retirement savings goals, and education funding needs can all influence whether a transfer is available and how it may fit into an overall financial plan. Reviewing these issues before initiating a transfer can help improve understanding and decision-making.

This resource is provided for educational purposes only and should not be construed as investment, tax, legal, or financial advice. Individuals should consult appropriate professionals regarding their specific circumstances before implementing any financial strategy.