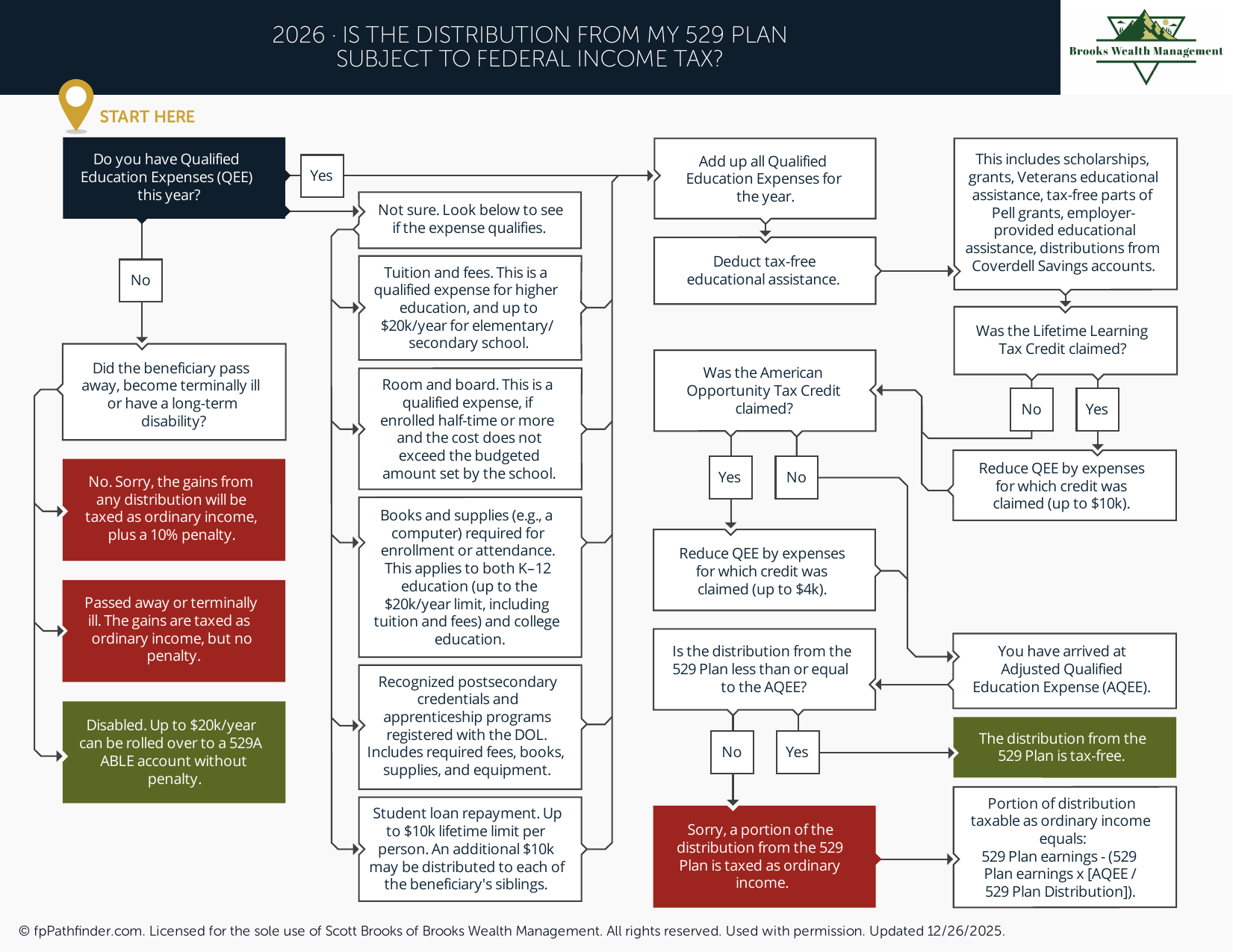

Is the Distribution from My 529 Plan Subject to Federal Income Tax?

Flowchart to determine whether a 529 plan distribution is taxable at the federal level.

Is the Distribution From My 529 Plan Subject to Federal Income Tax?

529 plans are commonly used to save for future education expenses because they offer potential tax advantages when funds are used for qualified educational purposes. However, not every distribution from a 529 plan automatically receives favorable federal tax treatment. Whether a withdrawal is subject to federal income tax often depends on how the funds are used, when the distribution occurs, and whether the expenses qualify under applicable rules.

This resource is designed to help you think through the factors that may determine whether a 529 plan distribution could be taxable at the federal level. While the rules can appear straightforward, there are several situations that may create unexpected tax consequences if withdrawals are not coordinated properly with education expenses.

Review How 529 Plan Distributions Are Generally Treated

529 plans are designed to encourage education savings by allowing investment growth to accumulate on a tax-advantaged basis. In general, distributions used for qualified education expenses may receive favorable federal tax treatment.

When reviewing a planned withdrawal, it is often important to consider:

- The amount being distributed

- The timing of the withdrawal

- The educational expenses incurred during the same period

- Whether those expenses qualify under applicable rules

- Whether other education-related tax benefits are being claimed

Understanding these factors can help determine whether a distribution is likely to qualify for favorable treatment or whether additional review may be warranted.

Review What May Constitute Qualified Education Expenses

The tax treatment of a 529 plan distribution often depends on whether the withdrawal is used for qualified education expenses. While education costs are frequently associated with tuition, the rules may extend to other eligible expenses depending on the circumstances.

Examples of expenses that may require review include:

- Tuition and fees

- Books and required educational materials

- Certain technology and equipment expenses

- Housing and meal costs in qualifying situations

- Other education-related expenses permitted under current rules

Because eligibility requirements can vary based on the type of institution, enrollment status, and other factors, families often benefit from reviewing expenses carefully before taking distributions.

Review Timing Considerations

One of the most overlooked aspects of 529 plan withdrawals is timing. Even when funds are ultimately used for educational purposes, the timing of the distribution and the related expenses can affect how the withdrawal is treated.

Questions that may be helpful to consider include:

- Did the education expense occur during the same period as the withdrawal?

- Were expenses paid before or after the distribution?

- Have supporting records been retained?

- Are multiple withdrawals being coordinated throughout the year?

Maintaining records and matching distributions with eligible expenses can help simplify documentation and support the intended tax treatment of a withdrawal.

Review Coordination With Other Education Benefits

Education expenses are sometimes used to qualify for tax credits, deductions, scholarships, grants, employer education benefits, or other assistance programs. In some situations, the same expense may not be used for multiple tax benefits simultaneously.

As a result, families often review:

- Scholarships and grants received by the student

- Employer-provided education assistance

- Available education tax credits

- Other education-related tax benefits

- How expenses are allocated among various programs

Coordinating these items may help avoid unintended consequences and provide a clearer understanding of how 529 plan distributions fit into the broader education funding strategy.

Additional resources that may be helpful include How Should I Fund My Child's College Education? and What Accounts Should I Consider If I Want to Save More?.

Review Situations That May Create Taxable Distributions

Not every withdrawal from a 529 plan necessarily qualifies for favorable federal tax treatment. Certain situations may result in all or a portion of a distribution being subject to federal income tax.

Examples may include:

- Withdrawals exceeding qualified education expenses

- Distributions used for non-qualified purposes

- Improper coordination with other education benefits

- Recordkeeping issues that make expenses difficult to substantiate

- Changes in educational plans after funds have been withdrawn

The existence of a taxable distribution does not necessarily mean a planning mistake occurred. Educational circumstances frequently change, and understanding the rules can help families evaluate available options when those situations arise.

Review Recordkeeping and Documentation

Good recordkeeping can play an important role in supporting the treatment of 529 plan withdrawals. Maintaining documentation may help demonstrate how distributions were used and whether corresponding educational expenses were incurred.

Documents that families commonly retain may include:

- Tuition statements

- Receipts for educational expenses

- Housing and meal documentation when applicable

- 529 plan distribution records

- Scholarship and financial aid documentation

Keeping organized records can make future tax reporting easier and may provide support if questions arise regarding a prior distribution.

Review Your Broader Education Funding Strategy

529 plan withdrawals are only one component of a broader education funding plan. Decisions regarding savings, distributions, financial aid, investment management, and family contributions often interact with one another.

Periodic review can help ensure that education funding decisions remain aligned with changing circumstances, educational goals, and broader financial priorities.

You may also find it helpful to review Where Should My Next Dollar Go? and What Issues Should I Consider When Reviewing My Beneficiaries? as part of a comprehensive financial planning process.

About This Resource

This decision flowchart was created to help individuals and families evaluate whether a 529 plan distribution may be subject to federal income tax. The goal is to provide a structured framework for reviewing common considerations such as qualified education expenses, timing requirements, coordination with other education benefits, documentation, and potential tax implications.

Every situation is different. Factors such as the amount distributed, the nature of the educational expenses, available tax benefits, scholarship assistance, and family circumstances can all influence how a withdrawal is treated. Reviewing these issues before taking a distribution may help reduce confusion and improve decision-making.

This resource is provided for educational purposes only and should not be considered investment, tax, legal, or financial advice. Individuals should consult appropriate professionals regarding their specific circumstances before making financial, tax, or education planning decisions.