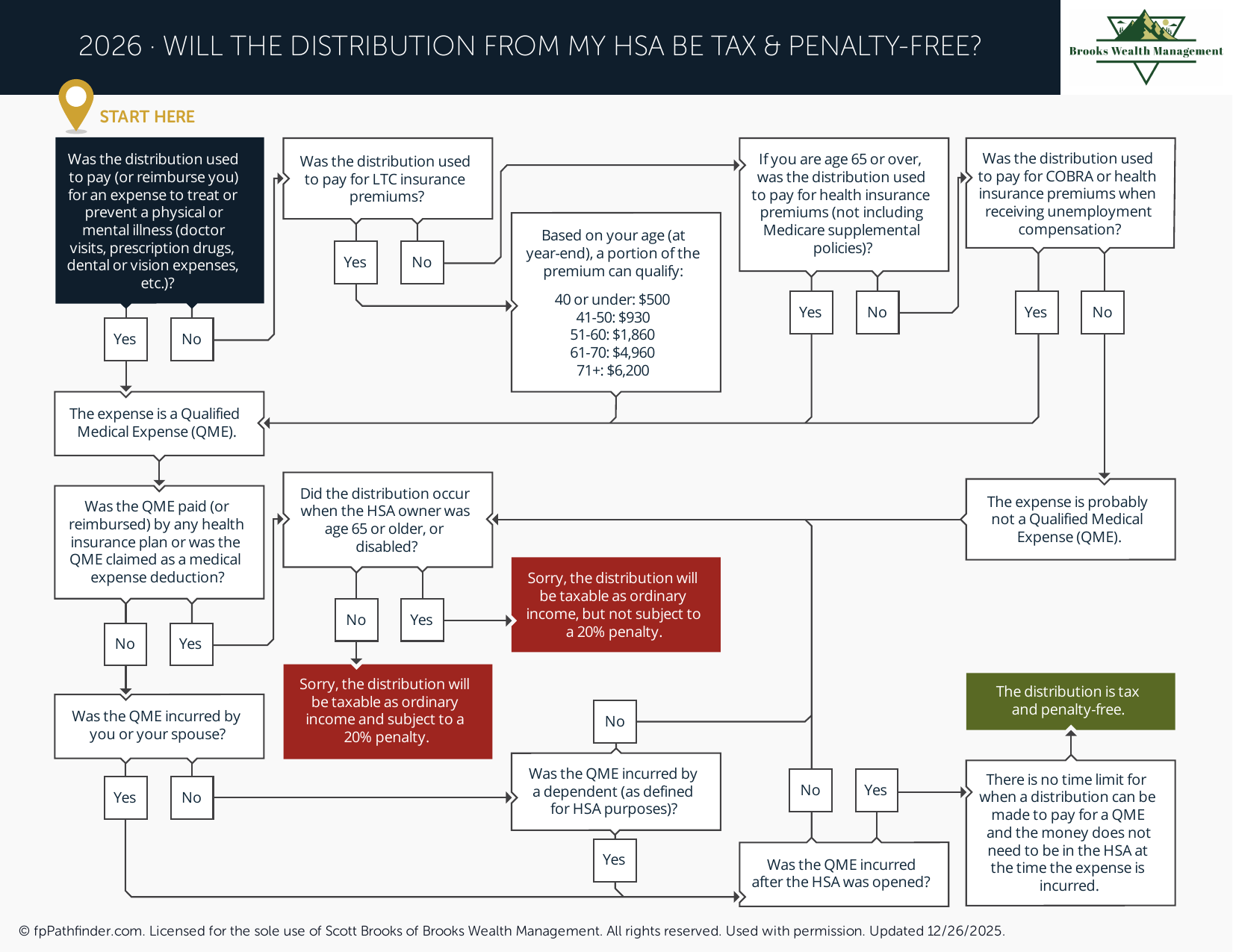

Will the Distribution from My HSA Be Tax- and Penalty-Free?

Flowchart to determine whether an HSA distribution is tax- and penalty-free.

Understanding HSA Distribution Taxes: A Guide for High-Income Professionals

As a high-income professional, business owner, or Gen X/Y client, you're likely leveraging every available tax-advantaged account to optimize your financial future. The Health Savings Account (HSA) stands out as a powerful tool, often dubbed the "triple-tax advantaged" account. But a common question I receive is: **will the distribution from my HSA be tax and penalty-free**? The answer, like many things in personal finance, depends on how you use it. Understanding **HSA distribution taxes** is crucial to maximizing its benefits.

At Brooks Wealth Management, we help clients navigate these complexities to ensure their financial strategies align with their goals. Let's delve into the specifics of HSA distributions and how to avoid unnecessary taxes and penalties.

The "Triple-Tax Advantage" and Qualified Medical Expenses

The allure of the HSA lies in its unique tax benefits: contributions are tax-deductible, earnings grow tax-free, and qualified distributions are tax-free. This triple advantage makes it an incredibly efficient vehicle for healthcare savings and even retirement planning. However, the key to maintaining this tax-free status for distributions hinges entirely on what those distributions are used for.

To be tax and penalty-free, your HSA distributions must be used for **qualified medical expenses**. The IRS defines these broadly, including medical, dental, and vision care, prescription drugs, and even certain long-term care insurance premiums. It's important to keep meticulous records of all your medical expenses, even if you pay for them out-of-pocket initially, as this allows you to reimburse yourself from your HSA at a later date, potentially years down the line. This strategy is a cornerstone of advanced HSA planning, effectively turning your HSA into an additional tax-free investment account for retirement.

Avoiding Penalties and Non-Qualified HSA Distribution Taxes

What happens if you take a distribution from your HSA for something other than a qualified medical expense? This is where **HSA distribution taxes** and penalties come into play. If you are under age 65 and withdraw funds for non-qualified expenses, that distribution will be subject to your ordinary income tax rate, plus a 20% penalty. This penalty is designed to discourage using HSA funds for non-medical purposes before retirement age.

Once you reach age 65, the 20% penalty no longer applies. However, if you take distributions for non-qualified expenses after age 65, those distributions will still be subject to ordinary income tax. This is similar to how a traditional IRA or 401(k) distribution works in retirement. Therefore, even in retirement, it's generally best practice to use HSA funds for qualified medical expenses to maintain their tax-free status. For more insights on optimizing your retirement accounts, consider exploring our resources on retirement planning.

Documentation is Key: Proving Qualified Medical Expenses

The burden of proof for qualified medical expenses rests with you, the account holder. The IRS does not require you to submit receipts with your tax return, but you must be able to provide them if audited. This means maintaining a robust record-keeping system is paramount. We advise clients to keep all receipts, Explanation of Benefits (EOB) statements, and any other documentation related to medical expenses. Digital copies are perfectly acceptable and often easier to manage.

A common misconception is that you must take a distribution from your HSA in the same year you incur the medical expense. This is not true. You can pay for medical expenses out-of-pocket and then reimburse yourself from your HSA years later, provided you have kept the necessary records. This allows your HSA funds to continue growing tax-free for a longer period. This strategy can significantly enhance your long-term wealth accumulation, similar to how strategic contributions to other tax-advantaged accounts work. Learn more about various savings vehicles in our guide on what accounts to consider for saving more.

HSA as a Retirement Planning Tool Beyond Healthcare

While primarily designed for healthcare, the HSA's unique tax structure makes it an excellent supplementary retirement account, especially for those who are diligent about saving and investing. By paying for current medical expenses out-of-pocket and allowing your HSA balance to grow, you create a substantial tax-free reservoir for future medical costs in retirement. This can be particularly valuable as healthcare expenses tend to increase with age, and Medicare doesn't cover everything. For information on Medicare eligibility, you might find our article on Medicare Part A and Part B helpful.

If you reach retirement with a significant HSA balance and find that your medical expenses are lower than anticipated, you can use the funds for non-qualified expenses after age 65, albeit subject to ordinary income tax, without the 20% penalty. This flexibility provides a valuable safety net and an additional source of income in retirement, complementing your other retirement savings like 401(k)s and IRAs. Understanding these nuances of **HSA distribution taxes** is key to leveraging this account effectively.

About This Resource

At Brooks Wealth Management, we are dedicated to providing clear, actionable financial guidance for high-income professionals, business owners, and Gen X/Y clients. Navigating the intricacies of **HSA distribution taxes** and maximizing your tax-advantaged accounts is a critical component of a robust financial plan. We believe in empowering our clients with the knowledge to make informed decisions about their wealth. For more free resources and insights, please visit our free resources page. If you have further questions or would like to discuss your specific financial situation, we invite you to book a consultation with our team today.

Have Questions About Your Situation?

This resource is a starting point. A free consultation with Scott Brooks, CFP® gives you a personalized perspective.

Book a Free ConsultationBased in Westlake Village, CA · Ventura County · Serving clients across all 50 states

Brooks Wealth Management is a Registered Investment Adviser (RIA) in the State of California. Registration does not imply a certain level of skill or training. This resource is provided for educational and informational purposes only and does not constitute investment, tax, or legal advice. Scott Brooks, CFP® · CRD #7227609 · Firm CRD #332237 · 2555 Townsgate Rd STE 200, Westlake Village, CA 91361