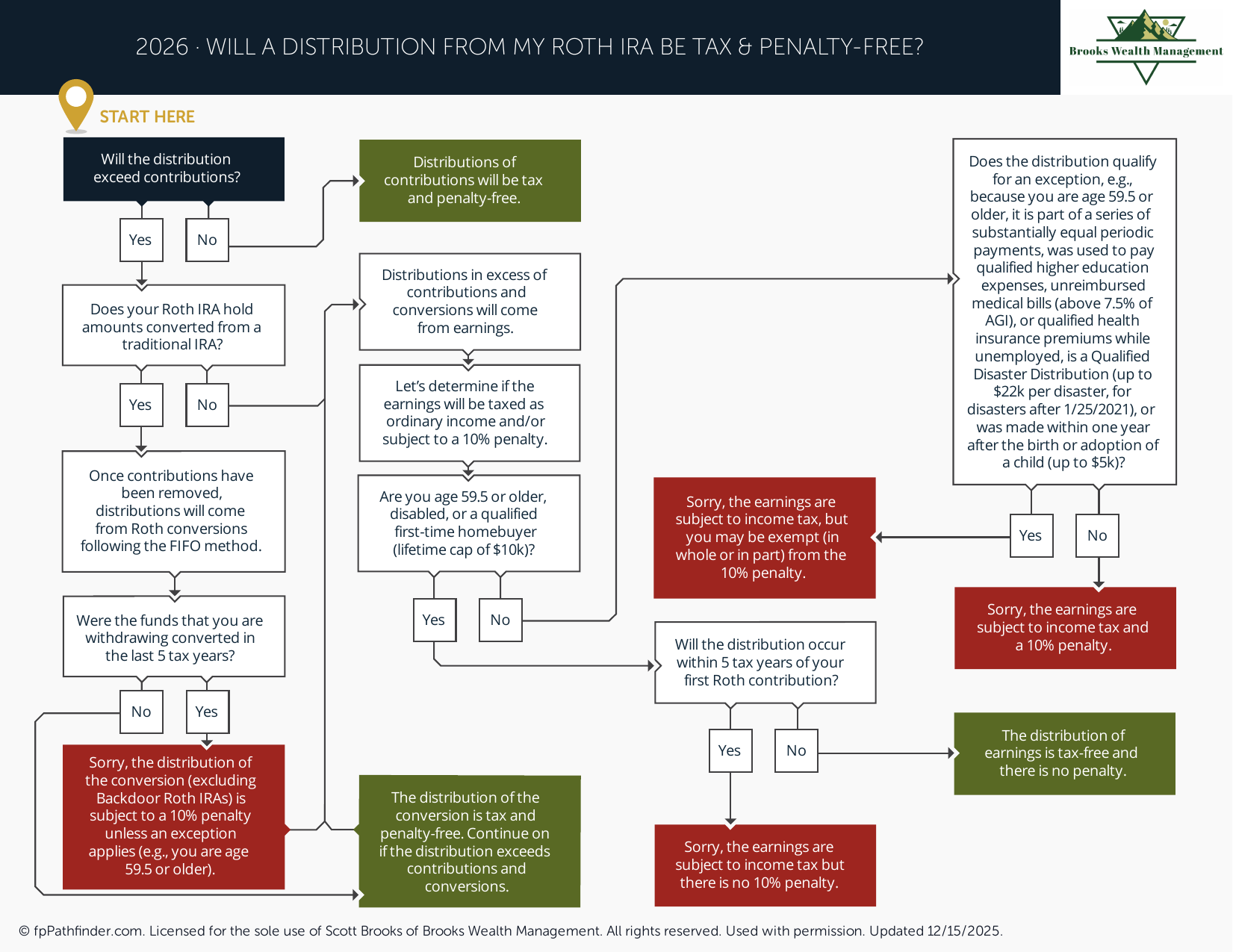

Will a Distribution from My Roth IRA Be Tax- and Penalty-Free?

Flowchart to determine whether a Roth IRA distribution is tax- and penalty-free.

When Can I Take a Roth IRA Distribution Tax and Penalty-Free?

One of the primary benefits of a Roth IRA is the potential for tax-free withdrawals. However, whether a Roth IRA distribution is tax-free and penalty-free depends on several factors, including the source of the funds being withdrawn, the age of the account owner, and how long the Roth IRA has been established.

Because Roth IRAs have unique distribution rules that differ from Traditional IRAs, individuals often review withdrawal requirements before accessing retirement assets. Understanding these rules may help avoid unexpected taxes or penalties and support broader retirement planning goals.

Review the Different Types of Roth IRA Assets

Not all Roth IRA dollars are treated the same when distributions occur. The IRS generally distinguishes between three categories of assets within a Roth IRA.

- Regular Roth IRA contributions.

- Amounts converted from other retirement accounts.

- Investment earnings generated within the Roth IRA.

Each category may be subject to different distribution rules, tax treatment, and penalty considerations.

Individuals evaluating retirement savings opportunities may also find it helpful to review what accounts to consider when saving more.

Review Roth IRA Contribution Withdrawal Rules

Regular Roth IRA contributions are generally the most flexible assets within the account.

Common considerations include:

- Contributions are generally distributed first under IRS ordering rules.

- Previously contributed principal can generally be withdrawn at any time.

- Withdrawals of contributions are generally not subject to income tax.

- Withdrawals of contributions are generally not subject to the 10% early withdrawal penalty.

Because contributions have already been taxed before entering the Roth IRA, many individuals are surprised to learn they may generally access these amounts without triggering additional taxes or penalties.

Review Roth Conversion Distribution Rules

Amounts converted from a Traditional IRA, rollover IRA, SEP IRA, SIMPLE IRA, or employer-sponsored retirement plan are subject to additional rules.

Each conversion generally has its own five-year holding period for purposes of determining whether a penalty may apply to withdrawals made before age 59½.

Common considerations include:

- The year each conversion occurred.

- The amount converted.

- Your current age.

- Whether multiple conversions have been completed.

- Whether an exception to the early withdrawal penalty may apply.

Individuals often review conversion holding periods before withdrawing converted assets from a Roth IRA.

Additional information is available in our guide discussing Roth conversion considerations.

Review the Five-Year Rule for Qualified Distributions

In addition to the conversion-specific holding periods, Roth IRAs are also subject to a broader five-year rule that applies to qualified distributions.

In general, the five-year period begins on January 1 of the year an individual first establishes and funds any Roth IRA.

Common considerations include:

- The date of the first Roth IRA contribution.

- The date of the first Roth conversion.

- Whether the Roth IRA owner has multiple Roth accounts.

- The timing of future retirement withdrawals.

Individuals often review the timing of their first Roth contribution because it may affect when earnings become eligible for tax-free treatment.

Review When Earnings May Be Tax-Free

Investment earnings within a Roth IRA generally receive the most favorable tax treatment when distributions qualify under IRS rules.

A distribution of earnings is commonly reviewed as qualified when:

- The applicable five-year requirement has been satisfied.

- The account owner has reached age 59½.

- The account owner has become disabled.

- The distribution qualifies under applicable first-time home purchase rules.

- The distribution occurs following the account owner's death.

When these requirements are met, earnings may generally be distributed free from federal income tax and the 10% early withdrawal penalty.

Review Roth IRA Ordering Rules

The IRS applies specific ordering rules to Roth IRA distributions.

Distributions generally occur in the following order:

- Regular Roth IRA contributions.

- Conversion and rollover contributions.

- Investment earnings.

These ordering rules often determine whether a distribution is taxable or subject to penalties.

Individuals considering Roth IRA withdrawals frequently review these rules before taking distributions, particularly when multiple contribution and conversion sources exist.

Review Common Exceptions to Early Withdrawal Penalties

Certain exceptions may apply when distributions occur before age 59½.

Common exceptions individuals review include:

- Disability.

- Qualified first-time home purchases.

- Certain medical expense situations.

- Certain substantially equal periodic payment arrangements.

- Distributions following death.

Whether an exception applies depends on individual circumstances and applicable IRS requirements.

Review How Roth IRA Distributions Fit Within Retirement Planning

Roth IRAs are often evaluated as part of a broader retirement income strategy because qualified distributions may provide tax-free retirement income.

Common planning considerations include:

- Future tax rate expectations.

- Required minimum distribution planning.

- Retirement cash flow needs.

- Estate and beneficiary planning goals.

- Coordination with taxable and tax-deferred accounts.

Because Roth IRA assets may offer flexibility during retirement, many individuals review distribution strategies as part of a broader retirement income plan.

Additional retirement planning considerations can be found in our guide discussing issues to consider before retirement.

About This Resource

This resource provides general educational information regarding Roth IRA distributions, withdrawal rules, five-year holding periods, and qualified distribution requirements. Roth IRA distribution rules can be complex because different rules apply to contributions, conversions, and investment earnings.

Individuals often review Roth IRA distribution strategies when evaluating retirement income planning, Roth conversion opportunities, tax diversification goals, estate planning objectives, and long-term wealth accumulation strategies. Understanding how distributions are taxed and when penalties may apply can be an important part of retirement planning.

This resource is intended to provide a framework for understanding common Roth IRA distribution considerations. It is not intended as investment, tax, legal, insurance, healthcare, cybersecurity, or financial advice. Individual circumstances vary, and tax rules may change over time.

If you would like to discuss how this topic fits into your broader financial plan, we invite you to schedule an introductory conversation.