What Issues Should I Consider When Starting a New Job?

Checklist of benefit elections, retirement plan enrollment, and financial steps when starting a new job.

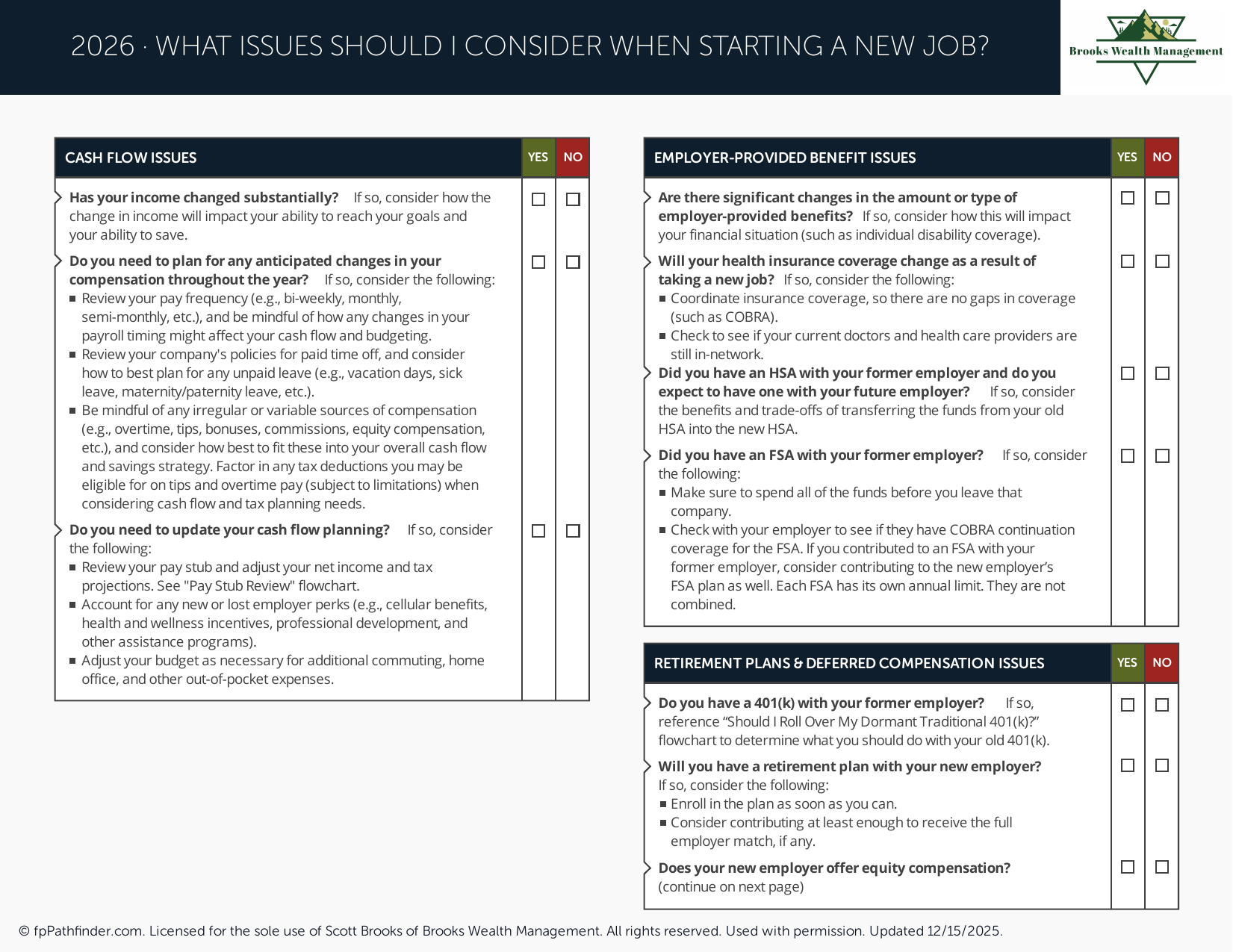

New Job Financial Checklist: What to Address in the First 30 Days

Starting a new job is exciting, and every new job financial checklist should start with the same reminder: the decisions you make in the first few weeks have a meaningful impact on your financial position for years. The new job financial checklist covers benefits enrollment, retirement contributions, tax withholding, and beneficiary designations, and most people rush through all of these during onboarding without fully understanding what they are choosing. This new job financial checklist is designed to help you be intentional about each one.

Benefits Enrollment: The Most Time-Sensitive Item on Your New Job Financial Checklist

Most employers give new employees 30 days to enroll in benefits, and this is the most time-sensitive item on your new job financial checklist. If you miss that window, you typically have to wait until the next open enrollment period. The new job financial checklist for benefits includes health insurance plan selection, dental and vision coverage, life insurance elections, and disability insurance. If your new employer offers a Health Savings Account paired with a high-deductible health plan, your new job financial checklist should include understanding the triple tax advantage: contributions are pre-tax, growth is tax-free, and qualified withdrawals are tax-free. An HSA is one of the most tax-efficient savings vehicles available and deserves a prominent place on any new job financial checklist.

401k Enrollment: A Critical Item on Every New Job Financial Checklist

Set your 401k contribution rate on day one as part of your new job financial checklist. Many plans auto-enroll new employees at a low default rate, often 3%, which is rarely enough. The 2026 contribution limit is $24,500, plus $8,000 catch-up if you are 50 or older. At minimum, your new job financial checklist should include contributing enough to capture your full employer match. You will also need to decide between a Roth 401k and a traditional 401k as part of your new job financial checklist. See the related resource on Roth 401k vs. traditional 401k for a decision framework. And if you have an old 401k from your previous employer, your new job financial checklist should include deciding whether to roll it over.

Tax Withholding: Update Your W-4 as Part of Your New Job Financial Checklist

A new job means a new W-4, and updating your withholding is an important part of your new job financial checklist. If your income has changed significantly, especially if you received a raise, changed from hourly to salaried, or have a spouse who also works, your withholding needs to be recalculated. The new job financial checklist for tax withholding is especially important if your new role comes with equity compensation, multiple income sources, or significant deductions.

Beneficiary Designations: Do Not Skip This on Your New Job Financial Checklist

When you enroll in a new 401k and life insurance plan, you will be asked to name beneficiaries, and this step on your new job financial checklist is too important to rush. Make sure your beneficiary designations reflect your current wishes, and check that your existing accounts are also up to date. Beneficiary designations override your will, so an outdated designation can send assets to the wrong person regardless of your estate plan. For more on the financial decisions surrounding job changes, see the related resources on getting a raise or promotion, reviewing beneficiary designations, and where your next dollar should go in the free resource library.

Book a free consultation to talk through your financial plan, or learn more about working together.Have Questions About Your Situation?

This resource is a starting point. A free consultation with Scott Brooks, CFP® gives you a personalized perspective.

Book a Free ConsultationBased in Westlake Village, CA · Ventura County

Brooks Wealth Management is a Registered Investment Adviser (RIA) in the State of California. Registration does not imply a certain level of skill or training. This resource is provided for educational and informational purposes only and does not constitute investment, tax, or legal advice. Scott Brooks, CFP® · CRD #7227609 · Firm CRD #332237 · 2555 Townsgate Rd STE 200, Westlake Village, CA 91361