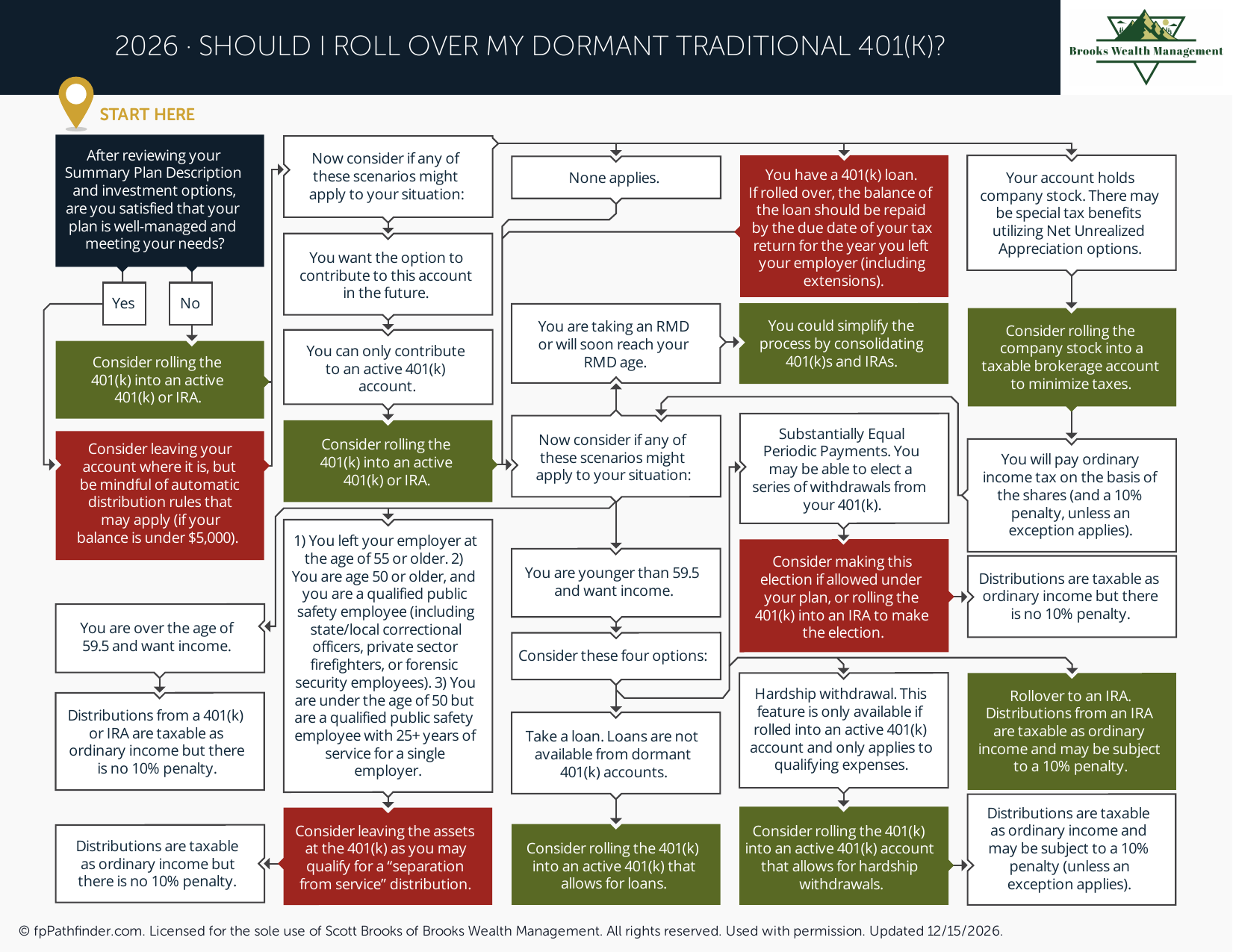

Should I Roll Over My Dormant Traditional 401(k)?

Flowchart to decide whether to roll over, keep, or cash out an old 401(k).

Should I Do a 401(k) Rollover?

When leaving an employer, one of the most important retirement planning decisions is determining what to do with an existing 401(k) balance. A 401(k) rollover may provide additional flexibility and investment options, but leaving assets in a former employer plan or rolling them into a new employer plan may also be worth evaluating.

Because retirement account decisions can affect taxes, investment management, withdrawal flexibility, and future planning opportunities, individuals often review all available options before moving retirement assets.

Review Your Available 401(k) Options

When separating from an employer, individuals generally have four primary options for an existing 401(k) account.

- Leave the assets in the former employer's plan.

- Roll the assets into a new employer's retirement plan.

- Complete a rollover to a Traditional IRA.

- Take a cash distribution.

Each option may have different investment, tax, administrative, and retirement planning implications.

Review Leaving Assets in a Former Employer Plan

In some situations, retaining assets in a former employer's plan may be worth evaluating.

Common considerations include:

- Availability of low-cost institutional investment options.

- Plan administrative fees.

- Investment selection quality.

- Creditor protection considerations.

- Potential retirement distribution flexibility.

Individuals often compare the costs and features of their existing plan before deciding whether a rollover is appropriate.

Review Rolling Assets Into a New Employer Plan

Some employer-sponsored retirement plans allow incoming rollovers from previous employer plans.

Common considerations include:

- Whether the new plan accepts rollovers.

- Investment options available in the new plan.

- Plan expenses.

- Administrative convenience.

- Consolidation of retirement accounts.

For some individuals, maintaining fewer retirement accounts may simplify future account management.

Review a 401(k) Rollover to an IRA

A rollover to a Traditional IRA is one of the most common retirement account decisions after leaving an employer.

Common reasons individuals evaluate an IRA rollover include:

- Expanded investment choices.

- Greater control over account management.

- Flexible beneficiary designations.

- Potential Roth conversion planning opportunities.

- Consolidation of multiple retirement accounts.

Because IRAs generally provide access to a wider range of investment options than employer-sponsored plans, individuals often review whether increased flexibility aligns with their broader financial goals.

Additional information is available in our guide discussing Roth conversion considerations.

Review Direct Versus Indirect Rollovers

The method used to complete a rollover can affect taxes and administrative requirements.

A direct rollover generally transfers assets directly between retirement custodians without the account owner taking possession of the funds.

Common considerations include:

- Maintaining tax-deferred status.

- Avoiding mandatory withholding requirements.

- Reducing administrative complexity.

- Avoiding potential rollover deadlines.

Individuals often review rollover procedures carefully before initiating any transfer of retirement assets.

Review Potential Tax Considerations

Many 401(k) rollovers can be completed without creating a taxable event when handled properly.

However, tax considerations may arise depending on:

- The type of account being rolled over.

- Whether after-tax contributions exist.

- Whether Roth assets are included.

- The destination account.

- The rollover method selected.

Understanding potential tax consequences is often an important part of evaluating rollover options.

Review Situations Where a Rollover May Not Be Appropriate

While IRA rollovers are common, certain situations may warrant additional review before moving retirement assets.

Common considerations include:

- Potential net unrealized appreciation (NUA) opportunities involving employer stock.

- Special retirement plan distribution rules.

- Unique investment options available within the plan.

- Creditor protection considerations.

- Access to penalty-free withdrawals under certain retirement plan provisions.

Individuals often evaluate these factors before completing a rollover.

Review Investment Management Considerations

Investment management may be an important factor when deciding whether to complete a 401(k) rollover.

Common questions individuals review include:

- Are current investment options appropriate?

- Are investment costs competitive?

- Would additional investment flexibility be beneficial?

- How does the account fit within the broader portfolio?

- Should multiple retirement accounts be consolidated?

The investment opportunities available after a rollover may differ significantly from those available within an employer-sponsored plan.

Review How a 401(k) Rollover Fits Within Your Retirement Plan

A rollover decision is often evaluated as part of a broader retirement planning strategy.

Common considerations include:

- Retirement timeline.

- Future withdrawal needs.

- Tax planning opportunities.

- Estate planning objectives.

- Long-term investment management goals.

Because retirement account decisions may affect multiple aspects of a financial plan, individuals often evaluate rollover options alongside broader retirement planning objectives.

Additional retirement planning considerations can be found in our guide discussing issues to consider before retirement.

Review Questions Before Completing a 401(k) Rollover

Before moving retirement assets, individuals often review the following questions:

- What investment options are available in each account?

- How do costs compare?

- Are there unique plan benefits that would be lost after a rollover?

- Will a rollover simplify retirement planning?

- How does the rollover fit within broader tax and retirement objectives?

These questions can help frame the decision before transferring retirement assets.

About This Resource

This resource provides general educational information regarding 401(k) rollovers, retirement account transfers, IRA rollover considerations, and related retirement planning issues. When leaving an employer, individuals often review whether to leave assets in a former employer plan, move assets into a new employer plan, complete an IRA rollover, or consider other available options.

The appropriate choice depends on factors such as investment options, plan expenses, retirement objectives, tax considerations, withdrawal flexibility, and overall financial planning goals. Because retirement account decisions can have long-term implications, reviewing all available options before taking action may be appropriate.

This resource is intended to provide a framework for understanding common 401(k) rollover considerations. It is not intended as investment, tax, legal, insurance, healthcare, cybersecurity, or financial advice. Individual circumstances vary, and applicable rules may change over time.

If you would like to discuss how this topic fits into your broader financial plan, we invite you to schedule an introductory conversation.