What Issues Should I Consider When Starting a Business?

Checklist of legal, tax, insurance, and financial planning steps when launching a new business.

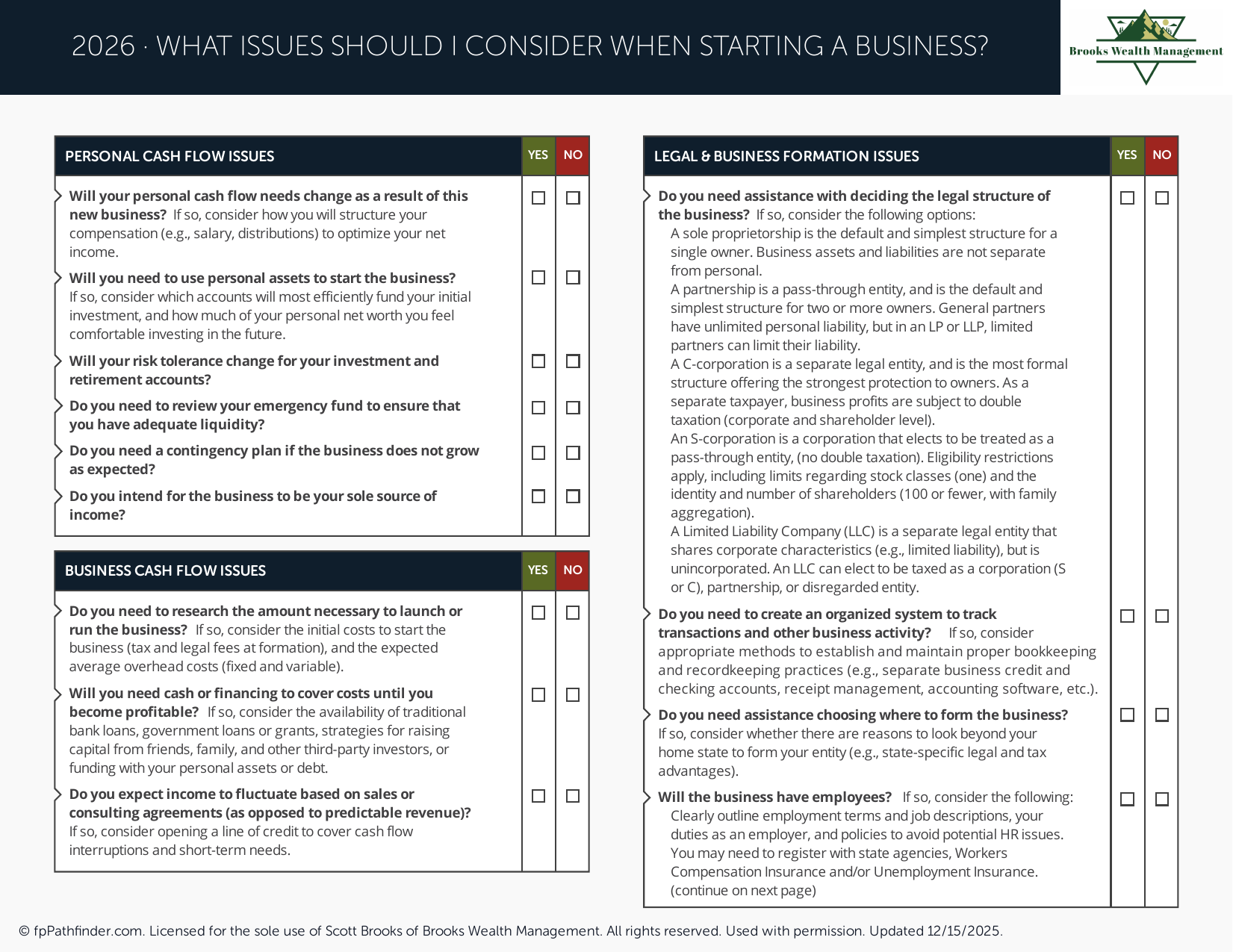

Starting a Business: The Financial Planning Issues That Matter Most

Starting a business is one of the most financially complex transitions a person can make. Beyond the excitement of building something new, starting a business involves a set of financial planning decisions that need to be made early. Some of these decisions, if deferred, become significantly more expensive to fix later. This checklist covers the key financial issues to address when starting a business, whether you are launching a side venture, going full-time as a 1099 contractor, or building a company from the ground up.

Entity Structure: The First Decision When Starting a Business

The legal structure of your business affects your taxes, your liability exposure, your ability to bring on partners or investors, and your retirement plan options when starting a business. For most small business owners and self-employed professionals starting a business, the choice is typically between a single-member LLC and an S-corporation. The S-corp structure can reduce self-employment taxes once your business income exceeds roughly $50,000 to $80,000 per year, but it comes with additional administrative requirements. Getting this decision right when starting a business is important because changing entity structure later can trigger tax consequences.

Retirement Plans: A Major Advantage of Starting a Business

One of the most underutilized advantages of starting a business is access to retirement plans with much higher contribution limits than a standard W-2 employee's 401k. A Solo 401k allows contributions of up to $72,000 in 2026 when starting a business, far more than the $24,500 employee-only limit. A SEP-IRA allows contributions of up to 25% of net self-employment income. A defined benefit plan can allow even higher contributions for high-income business owners who are older and want to accelerate retirement savings after starting a business. Choosing the right retirement plan structure when starting a business can save tens of thousands of dollars in taxes annually. See the related resource on SEP IRA vs. SIMPLE IRA for a comparison of the most common small business retirement plan options.

Taxes: What Changes When Starting a Business

When starting a business, you are responsible for paying your own taxes because no employer is withholding them for you. This means making quarterly estimated tax payments to avoid underpayment penalties. Starting a business also means you are responsible for both the employee and employer portions of Social Security and Medicare taxes, which adds 15.3% on top of your income tax rate on the first $184,500 of net self-employment income in 2026. Understanding this when starting a business prevents the unpleasant surprise of a large tax bill in April.

Insurance and Risk Management When Starting a Business

Starting a business creates insurance needs that employees do not have, including business liability insurance, errors and omissions coverage, business interruption insurance, and disability insurance. Disability insurance is often called the most important and most overlooked coverage for people starting a business. If you cannot work, your business income stops. For more on the financial planning issues surrounding starting a business, see the related resources on being a business owner or 1099 worker, reviewing health and life insurance, and where your next dollar should go in the free resource library.

Have Questions About Your Situation?

This resource is a starting point. A free consultation with Scott Brooks, CFP® gives you a personalized perspective.

Book a Free ConsultationBased in Westlake Village, CA · Ventura County

Brooks Wealth Management is a Registered Investment Adviser (RIA) in the State of California. Registration does not imply a certain level of skill or training. This resource is provided for educational and informational purposes only and does not constitute investment, tax, or legal advice. Scott Brooks, CFP® · CRD #7227609 · Firm CRD #332237 · 2555 Townsgate Rd STE 200, Westlake Village, CA 91361