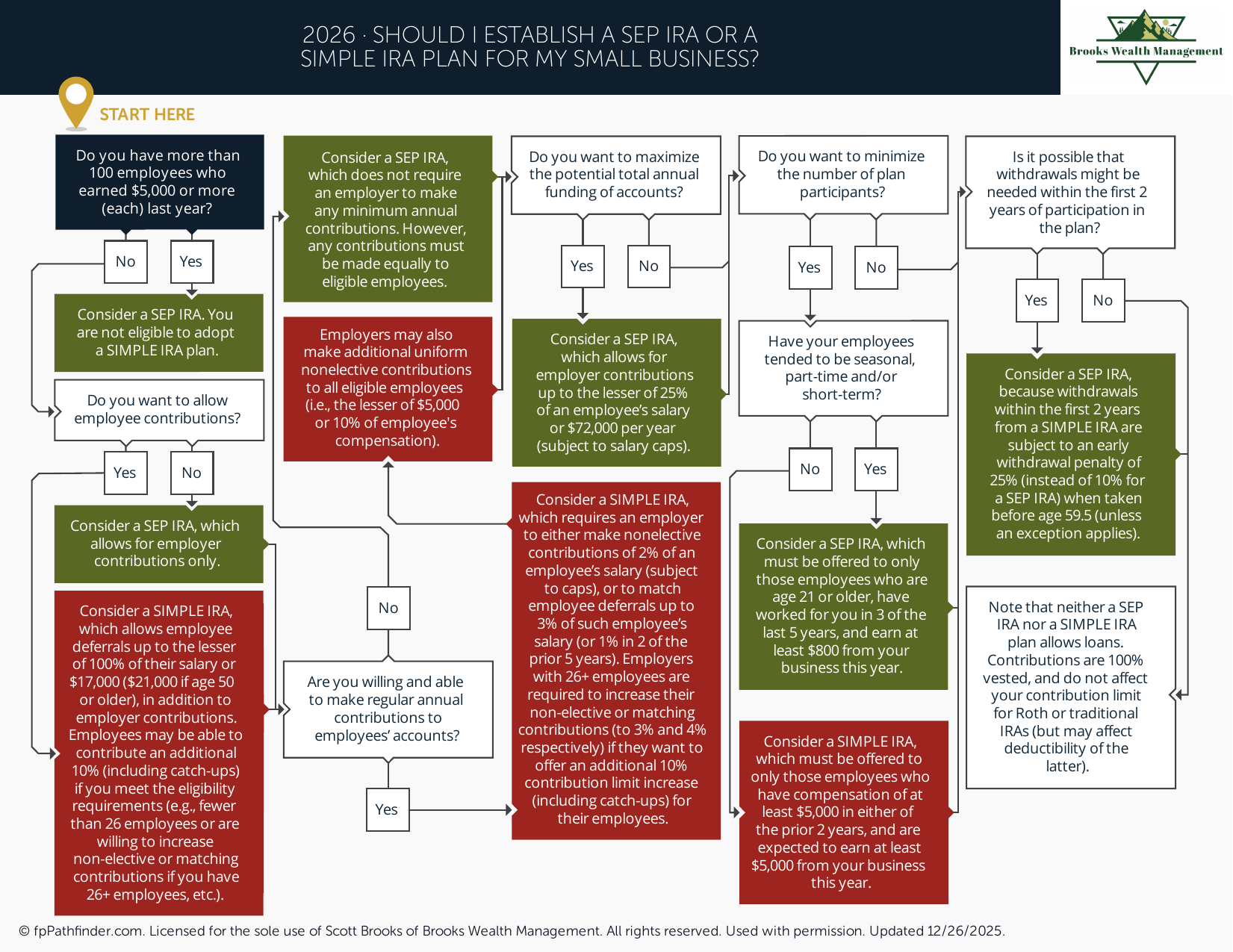

Should I Establish a SEP IRA or a SIMPLE IRA for My Small Business?

Flowchart comparing SEP IRA and SIMPLE IRA options for small business owners.

Should I Choose a SEP IRA or a SIMPLE IRA for My Business?

SEP IRAs and SIMPLE IRAs are two retirement plan options commonly considered by small business owners, self-employed individuals, and growing companies. Both plans can provide tax-advantaged retirement savings opportunities, but they differ in contribution structures, employer obligations, employee participation, and administrative requirements.

The appropriate choice often depends on factors such as business size, profitability, employee demographics, retirement savings goals, and the level of flexibility desired by the business owner.

Review How a SEP IRA Works

A Simplified Employee Pension (SEP) IRA is an employer-sponsored retirement plan that allows employers to make contributions on behalf of eligible employees.

Common features include:

- Employer-only contributions.

- Flexible annual contribution decisions.

- Minimal administrative requirements.

- Tax-deductible employer contributions.

- Immediate employee ownership of contributions.

Because contributions are discretionary, employers may choose different contribution amounts from year to year based on business performance and cash flow needs.

Review How a SIMPLE IRA Works

A Savings Incentive Match Plan for Employees (SIMPLE) IRA allows both employers and employees to contribute toward retirement savings.

Common features include:

- Employee salary deferral contributions.

- Required employer contributions.

- Relatively simple administration.

- Tax-deferred growth potential.

- Retirement savings opportunities for both employers and employees.

SIMPLE IRAs are often reviewed by businesses seeking a retirement plan that encourages employee participation while maintaining relatively straightforward administration.

Review Contribution Flexibility

One of the primary differences between a SEP IRA and a SIMPLE IRA involves contribution flexibility.

With a SEP IRA, employers generally determine whether to contribute each year and how much to contribute, subject to applicable limits.

Common considerations include:

- Variable business income.

- Seasonal cash flow fluctuations.

- Changing profitability.

- Owner retirement savings goals.

- Long-term business planning objectives.

Businesses with inconsistent earnings often review whether contribution flexibility is an important factor when selecting a retirement plan.

Review Employer Contribution Requirements

Employer obligations differ significantly between the two plans.

With a SIMPLE IRA, employers generally must make contributions each year through either:

- A matching contribution formula.

- A non-elective contribution formula.

With a SEP IRA, contributions are generally discretionary.

Business owners often review whether mandatory employer contributions align with expected cash flow and budgeting objectives.

Review Employee Participation Considerations

Employee participation may be an important factor when evaluating retirement plan options.

Common questions include:

- Should employees be allowed to contribute their own salary deferrals?

- Is increasing employee retirement participation a priority?

- Will retirement benefits support employee retention goals?

- How important are retirement benefits in recruiting efforts?

- What retirement benefits are common within the industry?

SIMPLE IRAs allow employee contributions, while SEP IRAs generally rely solely on employer funding.

Review Contribution Limits

Contribution limits differ between SEP IRAs and SIMPLE IRAs.

Common considerations include:

- Owner retirement savings goals.

- Business profitability.

- Employee compensation levels.

- Long-term retirement planning objectives.

- Desired annual contribution amounts.

Individuals seeking higher contribution potential often review whether SEP IRA limits better align with their retirement savings objectives.

Review Administrative Requirements

Both plans are generally less complex than traditional 401(k) plans, but administrative requirements differ.

Common considerations include:

- Plan setup requirements.

- Ongoing administration.

- Annual reporting obligations.

- Employee communications.

- Employer recordkeeping responsibilities.

Many business owners evaluate the time and resources required to maintain each plan before making a decision.

Review Business Size Considerations

The number of employees may influence which retirement plan structure is most appropriate.

Common considerations include:

- Current workforce size.

- Expected future hiring.

- Employee turnover rates.

- Compensation structures.

- Growth projections.

As businesses expand, retirement plan needs may evolve, making long-term planning an important consideration.

Review Tax Considerations

Both SEP IRAs and SIMPLE IRAs may provide tax-related benefits for employers and participants.

Common considerations include:

- Employer deduction opportunities.

- Tax-deferred growth.

- Current taxable income reduction.

- Retirement income planning.

- Coordination with other retirement accounts.

Tax outcomes depend on individual circumstances and may warrant review alongside broader financial planning objectives.

Review Alternative Retirement Plan Options

Before selecting a SEP IRA or SIMPLE IRA, some business owners review additional retirement plan alternatives.

Common options include:

- Traditional 401(k) plans.

- Safe Harbor 401(k) plans.

- Solo 401(k) plans.

- Cash balance plans.

- Defined benefit pension plans.

Each option has different contribution limits, administrative requirements, and planning considerations.

Additional retirement planning information is available in our guide discussing accounts to consider when saving more.

Review Which Plan May Fit Your Situation

Business owners often review the following questions when comparing SEP IRAs and SIMPLE IRAs:

- Is contribution flexibility important?

- Should employees be able to make salary deferrals?

- Are mandatory employer contributions acceptable?

- How much administrative complexity is appropriate?

- What retirement savings goals exist for owners and employees?

The answers to these questions may help determine which retirement plan structure aligns more closely with business and personal financial objectives.

About This Resource

This resource provides general educational information regarding SEP IRAs, SIMPLE IRAs, small business retirement plans, and related retirement planning considerations. Both retirement plan types may provide tax-advantaged savings opportunities, but they differ in contribution structures, employee participation, administrative requirements, and employer obligations.

Business owners often review retirement plan options alongside broader business planning, employee benefits strategies, retirement savings goals, and tax planning considerations. The appropriate retirement plan depends on individual business circumstances, workforce characteristics, profitability, and long-term objectives.

This resource is intended to provide a framework for understanding common SEP IRA and SIMPLE IRA considerations. It is not intended as investment, tax, legal, insurance, healthcare, cybersecurity, or financial advice. Individual circumstances vary, and applicable rules may change over time.

If you would like to discuss how this topic fits into your broader financial plan, we invite you to schedule an introductory conversation.