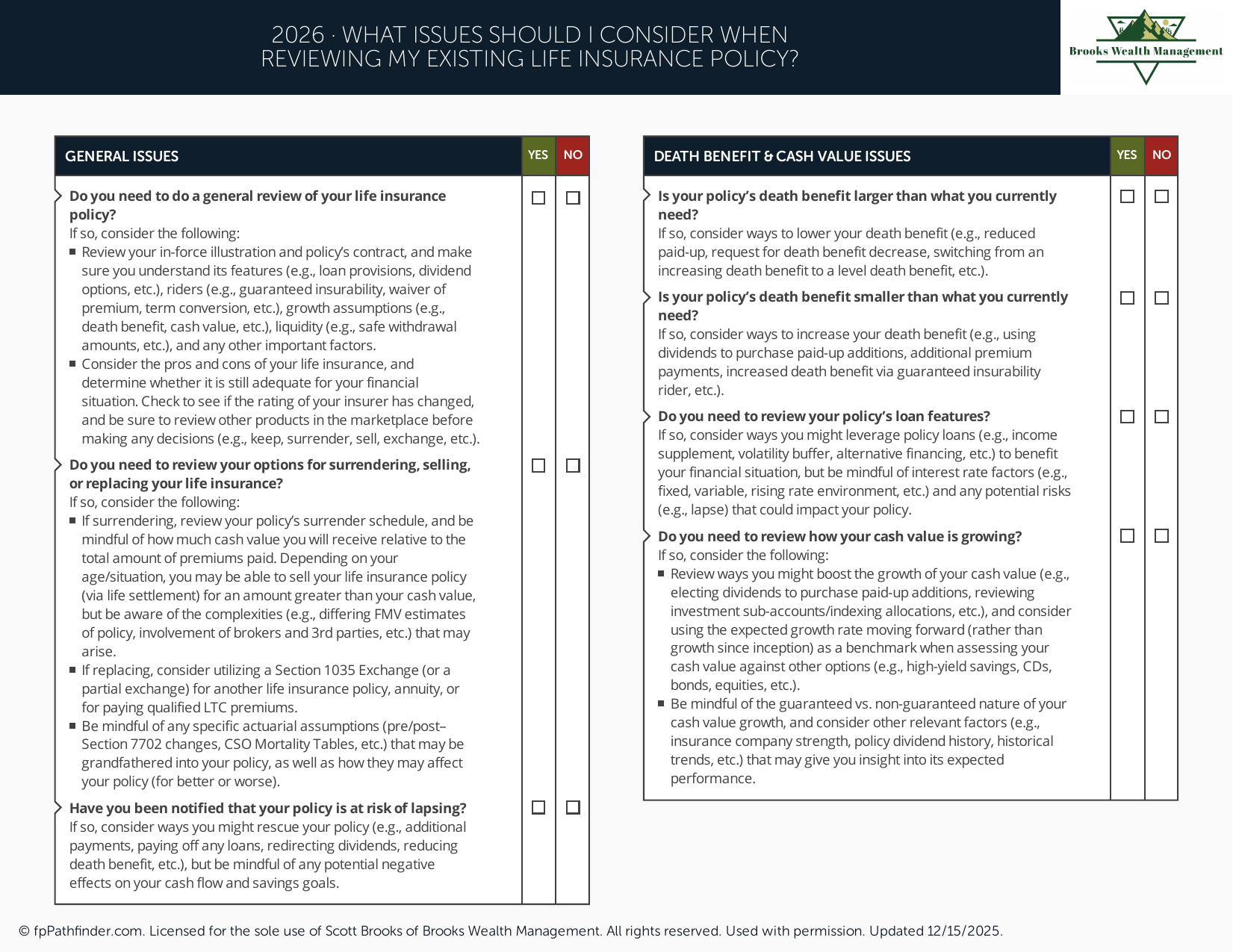

What Issues Should I Consider When Reviewing My Existing Life Insurance Policy?

Checklist for evaluating whether your current life insurance policy still meets your needs.

What Issues Should I Consider When Reviewing My Existing Life Insurance Policy?

Life insurance is often purchased to address a specific need at a particular point in time. Over the years, however, personal circumstances, financial goals, family responsibilities, and overall net worth may change. As a result, a life insurance policy that originally appeared appropriate may deserve periodic review.

This checklist is designed to provide a framework for reviewing an existing life insurance policy. The goal is not to determine whether a policy should be changed, replaced, maintained, or surrendered. Instead, it is intended to help identify common questions and planning considerations that may be worth evaluating as part of an ongoing financial review.

Review Why Life Insurance Needs Can Change Over Time

Life insurance planning often evolves alongside major life events. Marriage, divorce, the birth of children, retirement planning, business ownership, estate planning goals, and changes in financial obligations may all influence how an existing policy fits within a broader financial plan.

For some individuals, life insurance is intended to help provide financial support for dependents. For others, it may play a role in business planning, estate planning, charitable objectives, or liquidity planning. Because the purpose of a policy can change over time, periodic reviews may help determine whether the policy continues to align with its original objectives.

Reviewing an existing policy does not necessarily mean changes are required. Rather, it provides an opportunity to better understand how the policy currently functions and whether it continues to serve its intended purpose.

Review the Policy's Original Purpose

One of the first questions to consider is why the policy was purchased in the first place. Understanding the original purpose can provide context when evaluating whether the coverage remains relevant today.

Common reasons individuals purchase life insurance may include:

- Income replacement for family members.

- Mortgage or debt protection.

- Funding future education expenses.

- Business continuity planning.

- Estate planning objectives.

- Liquidity needs for heirs.

- Charitable planning goals.

If the original objective has changed significantly, additional review may be appropriate. Individuals evaluating broader insurance planning topics may also find it helpful to review What Issues Should I Consider When Reviewing My Health and Life Insurance Coverage?.

Review Coverage Amounts and Financial Obligations

Financial obligations often change over time. Mortgages may be reduced or paid off, children may become financially independent, businesses may grow, and retirement assets may accumulate. These changes can affect how a life insurance policy fits within an overall financial strategy.

Questions that may be worth reviewing include:

- Have major debts increased or decreased?

- Have family responsibilities changed?

- Have assets or savings grown significantly?

- Are there new financial obligations that did not exist when the policy was purchased?

- Has retirement planning affected the role of life insurance within the household balance sheet?

Because every situation is different, coverage needs should be evaluated based on individual circumstances rather than generalized rules of thumb.

Review Beneficiary Designations and Ownership Information

Beneficiary designations are among the most important elements of a life insurance policy review. Changes in family circumstances can create a need to revisit beneficiary elections and confirm that policy information remains accurate.

Items that may be reviewed include:

- Primary beneficiary designations.

- Contingent beneficiary designations.

- Policy ownership structure.

- Trust ownership arrangements.

- Contact information on file with the insurance company.

Some individuals also coordinate beneficiary reviews alongside broader estate planning reviews. A related resource that may be helpful is What Issues Should I Consider When Reviewing My Beneficiaries?.

Review Policy Features and Riders

Many life insurance policies contain additional features, riders, or optional benefits that may have been added when the policy was issued. Understanding which provisions remain in force can be an important part of a policy review.

Depending on the policy, items that may warrant review include:

- Premium structures.

- Cash value provisions.

- Loan features.

- Accelerated benefit provisions.

- Disability-related riders.

- Long-term care-related riders.

- Guaranteed insurability provisions.

The objective is not necessarily to add or remove features but rather to understand how they function and whether they continue to align with the policy owner's goals and circumstances.

Review How Life Insurance Fits Within Your Broader Financial Plan

Life insurance is often interconnected with other financial planning areas. Retirement planning, estate planning, tax considerations, business planning, and asset protection strategies may all influence how an existing policy is evaluated.

For example, individuals approaching retirement may also wish to review What Issues Should I Consider Before I Retire?. Those reviewing estate planning topics may find additional resources within the Brooks Wealth Management Resource Library.

Evaluating life insurance within the context of a broader financial plan may provide a more complete understanding of how the policy contributes to overall financial objectives.

Questions Worth Reviewing Periodically

Many policy owners find it helpful to periodically revisit the following questions:

- Why was this policy originally purchased?

- Has the intended purpose changed?

- Have family circumstances changed?

- Have financial obligations changed?

- Are beneficiary designations current?

- Do policy features remain relevant?

- Has retirement planning altered the role of life insurance?

- Does the policy continue to support broader planning objectives?

A structured review process can help ensure important considerations are not overlooked as circumstances evolve over time.

About This Resource

This checklist was created as an educational resource to help individuals better understand common considerations when reviewing an existing life insurance policy. The objective is to provide a framework for evaluating policy details, beneficiary information, coverage considerations, and broader planning factors that may influence future decisions.

Because insurance needs vary based on individual circumstances, this resource should be used for educational purposes only and should not be interpreted as a recommendation regarding any insurance policy, coverage amount, ownership structure, or planning strategy.

If you have questions about how life insurance fits into your broader financial picture, you can schedule an introductory conversation.