What Issues Should I Consider Regarding My Restricted Stock Units?

Checklist of vesting, tax withholding, and planning considerations for restricted stock units (RSUs).

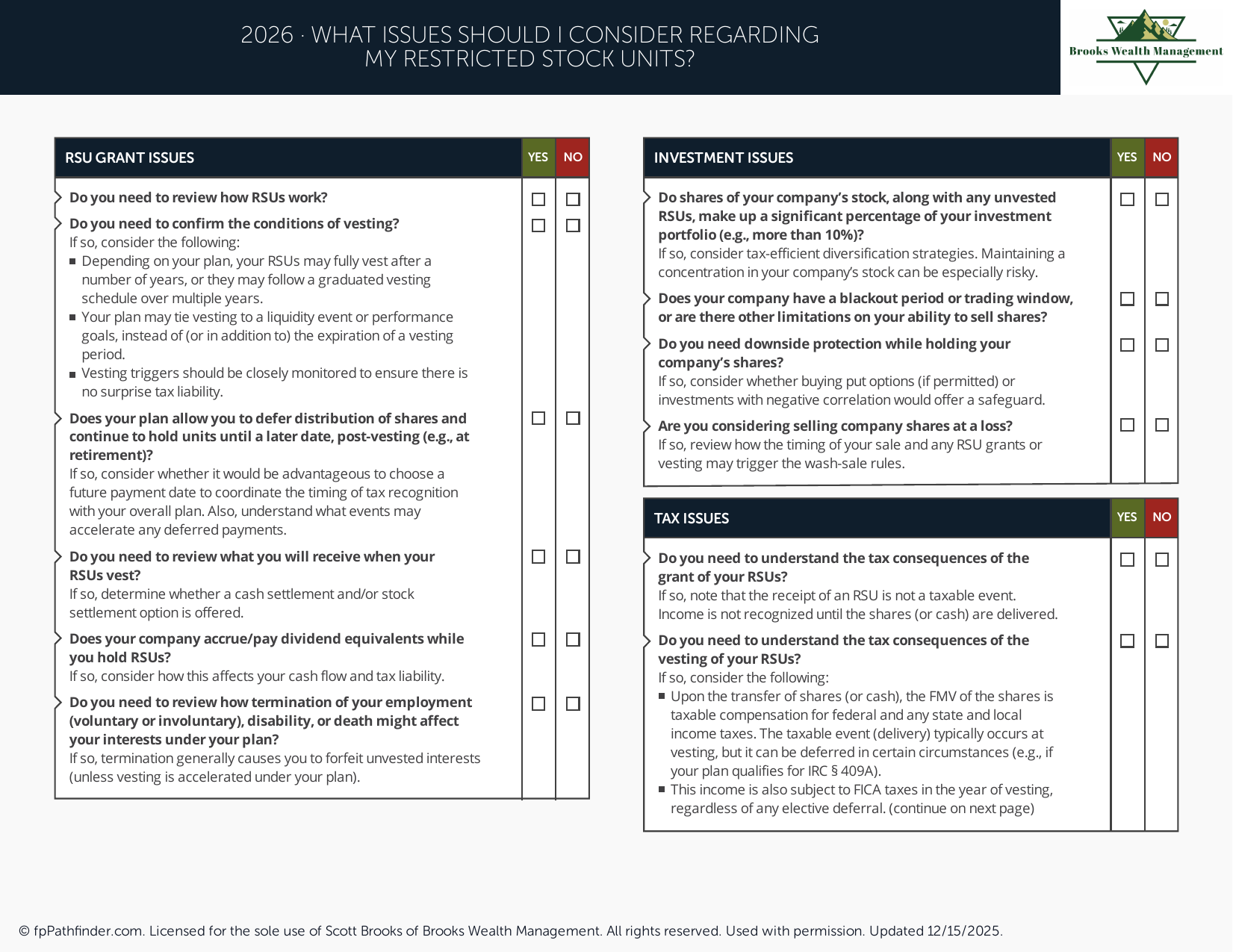

What Should I Consider When Managing Restricted Stock Units (RSUs)?

Restricted Stock Units (RSUs) are a common form of equity compensation offered by employers. While RSUs can represent a meaningful component of total compensation, they also introduce tax, investment, and financial planning considerations that may differ from traditional salary and bonus income.

Understanding how RSUs work, when they become taxable, and how they fit within your broader financial plan can help support more informed decision-making.

What Are Restricted Stock Units?

Restricted Stock Units are a form of employer-provided compensation that generally entitles an employee to receive company shares or the cash equivalent after certain conditions have been satisfied. These conditions often involve continued employment through a specified vesting schedule.

Unlike stock options, RSUs generally do not require an employee to purchase shares. Once vested, the shares are typically delivered directly to the employee and become part of the employee's investment portfolio.

Understanding Vesting Schedules

The vesting schedule determines when ownership of RSU shares transfers to the employee. Vesting schedules vary by employer and may include cliff vesting, graded vesting, or other structures.

Because vesting events often create taxable income, understanding future vesting dates may help employees prepare for cash flow needs, tax obligations, and broader financial planning decisions.

Employees who receive RSUs regularly may wish to track future vesting schedules as part of their overall compensation planning process.

How RSUs Are Generally Taxed

In general, RSUs become taxable when they vest. The fair market value of the shares received at vesting is typically treated as ordinary compensation income and may be subject to federal income taxes, state income taxes (where applicable), Social Security taxes, and Medicare taxes.

Employers often withhold a portion of the shares or cash proceeds to satisfy withholding requirements. However, withholding amounts may not always fully cover an individual's ultimate tax liability, particularly for employees in higher tax brackets.

After vesting, future appreciation or depreciation of the shares is generally treated under capital gains tax rules when the shares are sold.

If you are evaluating broader tax planning opportunities, you may find our resource on Roth conversions helpful.

Concentration Risk and Diversification Considerations

Many employees accumulate company stock through RSUs, employee stock purchase plans (ESPPs), stock options, or other equity compensation arrangements. As a result, a significant portion of an individual's net worth may become concentrated in a single company.

Concentrated positions may introduce risks that differ from a diversified investment portfolio. Evaluating company stock exposure within the context of overall assets, income sources, and financial goals may help provide additional perspective when making decisions regarding vested shares.

Diversification considerations should be evaluated alongside tax consequences, investment objectives, liquidity needs, and risk tolerance.

How RSUs Fit Within a Broader Financial Plan

RSUs often represent only one component of a larger compensation package. Salary, bonuses, retirement plans, stock options, ESPPs, deferred compensation plans, and other benefits may all interact with RSU planning decisions.

Employees may wish to evaluate how future vesting events affect retirement savings, investment allocation, tax planning, cash flow needs, education funding goals, charitable giving, or other financial priorities.

For additional savings and investment planning ideas, you may find our guide on accounts to consider if you want to save more helpful.

Planning for Future Vesting Events

Future RSU vesting events may increase taxable income in a given year and potentially affect withholding requirements, estimated tax payments, tax credits, deductions, Medicare premiums, or other financial planning considerations.

Reviewing projected vesting schedules in advance may help individuals prepare for upcoming tax obligations and evaluate how future compensation fits into their overall financial strategy.

Individuals approaching retirement may also wish to evaluate how unvested and vested RSUs fit within their retirement planning strategy. You may find our guide on issues to consider before retirement helpful.

When Professional Guidance May Be Helpful

RSUs can involve multiple tax, investment, and cash flow considerations. Employees who receive significant equity compensation may benefit from coordinating with qualified tax professionals and financial advisors when evaluating available options.

Brooks Wealth Management works with professionals, business owners, retirees, and families on a wide range of financial planning topics, including equity compensation planning, tax-aware financial planning, and wealth management. You can learn more about our approach on our pricing page or explore additional educational content through our free resource library.

About This Resource

This resource provides general educational information regarding Restricted Stock Units (RSUs), equity compensation, taxation, diversification considerations, and related financial planning concepts. Every individual's circumstances are different, and financial decisions should be evaluated based on personal goals, tax considerations, employer plan provisions, and overall financial resources.

If you would like to discuss your situation, we invite you to schedule an introductory conversation.

Have Questions About Your Situation?

This resource is intended for educational purposes only. If you would like to discuss your circumstances, schedule an introductory conversation with Scott Brooks, CFP®.

Schedule an Introductory ConversationVentura County, California · Serving Clients Throughout California and Across the United States

Brooks Wealth Management is a Registered Investment Adviser registered with the State of California. Registration does not imply a certain level of skill or training. This content is provided for informational and educational purposes only and should not be construed as investment, tax, legal, or accounting advice. Advisory services are offered only to clients or prospective clients where Brooks Wealth Management and its representatives are properly licensed or exempt from licensure. Investing involves risk, including the potential loss of principal. CFP® is a certification mark owned by the Certified Financial Planner Board of Standards, Inc. Scott Brooks, CFP® · CRD #7227609 · Firm CRD #332237