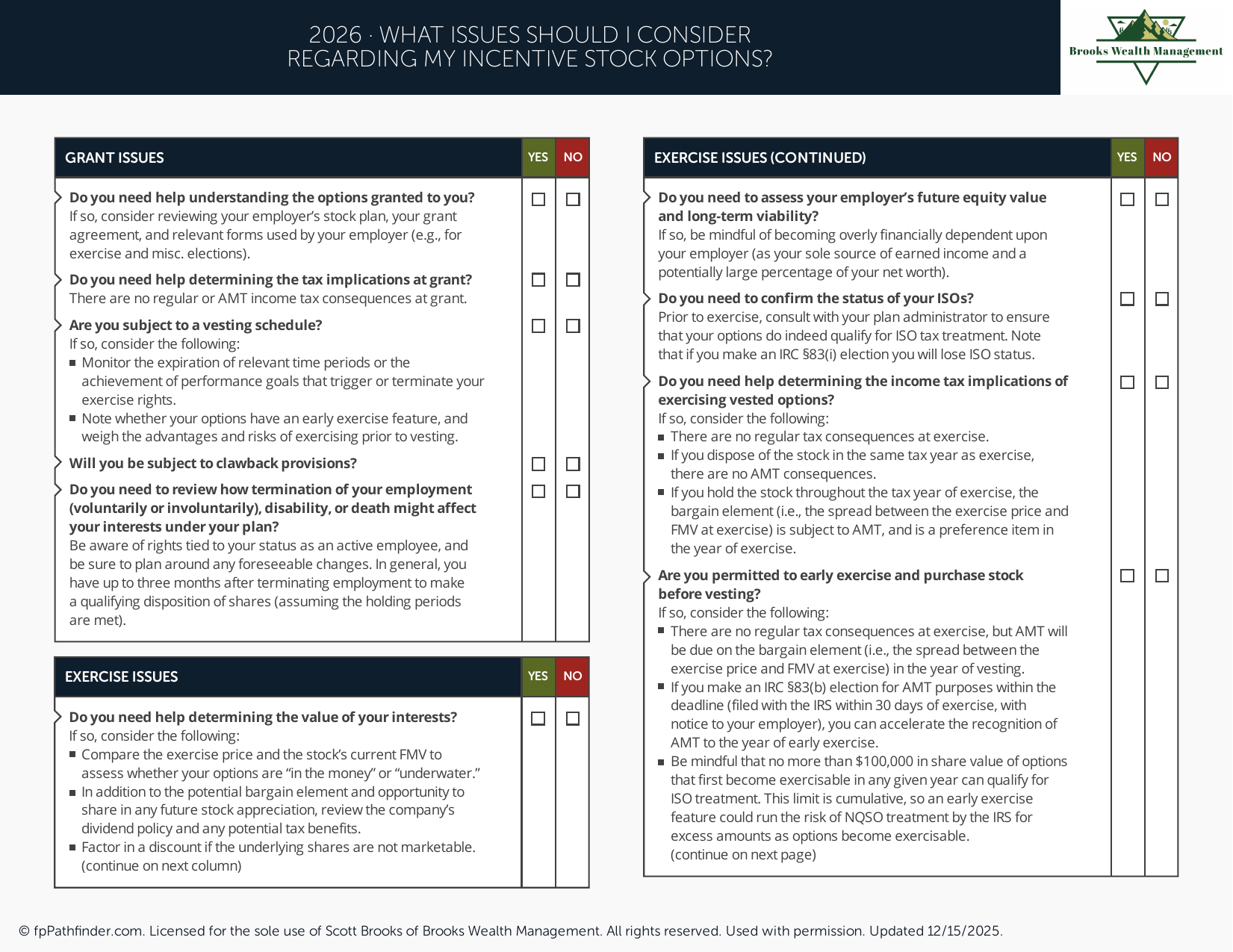

What Issues Should I Consider Regarding My Incentive Stock Options?

Checklist of AMT, exercise timing, and tax planning considerations for incentive stock options (ISOs).

What Should I Consider When Managing Incentive Stock Options (ISOs)?

Incentive Stock Options (ISOs) are a form of equity compensation that may provide employees with the opportunity to purchase company stock at a predetermined exercise price. ISOs are subject to specific tax rules that differ from other forms of equity compensation, including Non-Qualified Stock Options (NQSOs) and Restricted Stock Units (RSUs).

Understanding how ISOs work, how they are taxed, and how they fit within a broader financial plan can help employees make more informed decisions regarding their equity compensation.

What Are Incentive Stock Options?

An Incentive Stock Option generally provides the right to purchase company stock at a specified exercise price established when the option is granted. If the stock's market value rises above the exercise price, the option may have economic value.

ISOs are governed by specific provisions of the Internal Revenue Code and may qualify for different tax treatment than other forms of stock compensation when certain requirements are satisfied.

Employees should review their stock plan documents to understand vesting schedules, exercise windows, expiration dates, and any employer-specific provisions that may affect their options.

Understanding Vesting and Exercise Rights

Most ISO grants are subject to a vesting schedule. Vesting determines when an employee earns the right to exercise the options. Until options vest, they generally cannot be exercised.

Employees should also be aware of expiration dates and any post-employment exercise deadlines. Unexercised options may expire if action is not taken within the applicable time period established by the employer's stock plan.

Tracking vesting schedules and exercise windows may help employees evaluate future planning opportunities and avoid unintentionally forfeiting compensation.

How ISOs Are Generally Taxed

In general, exercising an ISO does not typically create ordinary income for regular federal income tax purposes at the time of exercise. However, the difference between the exercise price and the fair market value of the stock at exercise may be relevant for Alternative Minimum Tax (AMT) calculations.

The potential impact of AMT depends on a variety of factors, including income, deductions, filing status, and other tax considerations. Because tax outcomes can vary significantly, employees should consult qualified tax professionals when evaluating ISO exercise decisions.

Future tax treatment may also depend on how long the shares are held after exercise and whether applicable holding period requirements are satisfied.

If you are evaluating broader tax planning opportunities, you may find our resource on Roth conversions helpful.

Qualifying and Disqualifying Dispositions

The tax treatment of ISO shares may depend on whether a sale qualifies as a qualifying disposition or a disqualifying disposition under applicable tax rules.

In general, a qualifying disposition requires satisfying specific holding period requirements established by the Internal Revenue Code. If those requirements are not met, different tax treatment may apply.

Because the tax consequences can differ substantially between qualifying and disqualifying dispositions, understanding applicable holding periods may be an important part of the planning process.

Liquidity, Cash Flow, and Exercise Considerations

Exercising stock options may require cash to cover the exercise cost, taxes, or both, depending on the circumstances and available exercise methods. Employees may wish to evaluate available liquidity, cash flow needs, and overall financial resources before exercising significant option grants.

Factors that may influence exercise decisions include the stock price, expiration dates, concentration risk, tax implications, available liquidity, and broader financial goals.

Because exercising options may affect future tax obligations and portfolio composition, some individuals review multiple scenarios before making a decision.

Concentration Risk and Diversification

Employees who receive ISOs may accumulate substantial exposure to a single company's stock through stock options, RSUs, employee stock purchase plans (ESPPs), retirement plans, or direct stock ownership.

Concentrated positions may introduce risks that differ from a diversified investment portfolio. Evaluating company stock exposure within the context of overall assets, income sources, and financial goals may help provide additional perspective when making equity compensation decisions.

Diversification considerations should be evaluated alongside tax consequences, liquidity needs, investment objectives, and risk tolerance.

How ISOs Fit Within a Broader Financial Plan

Incentive Stock Options are often one component of a broader compensation package that may include salary, bonuses, RSUs, ESPPs, deferred compensation plans, retirement benefits, and other employer-sponsored programs.

Employees may wish to evaluate how stock option decisions affect retirement planning, investment allocation, tax planning, education funding goals, charitable giving objectives, and other financial priorities.

For additional savings and investment planning ideas, you may find our guide on accounts to consider if you want to save more helpful.

Planning for Future Equity Compensation Events

Future option exercises and stock sales may affect taxable income, AMT calculations, withholding requirements, estimated tax payments, Medicare premiums, tax credits, deductions, and other financial planning considerations.

Reviewing future vesting schedules and exercise opportunities in advance may help individuals evaluate how equity compensation fits within their overall financial strategy.

Employees approaching retirement may also wish to evaluate how stock options fit within their retirement income strategy. You may find our guide on issues to consider before retirement helpful.

When Professional Guidance May Be Helpful

ISOs can involve multiple tax, investment, and cash flow considerations, including potential Alternative Minimum Tax implications. Employees who receive significant equity compensation may benefit from coordinating with qualified tax professionals and financial advisors when evaluating available options.

Brooks Wealth Management works with professionals, business owners, retirees, and families on a wide range of financial planning topics, including equity compensation planning, tax-aware financial planning, and wealth management. You can learn more about our approach on our pricing page or explore additional educational content through our free resource library.

About This Resource

This resource provides general educational information regarding Incentive Stock Options (ISOs), Alternative Minimum Tax considerations, equity compensation, and related financial planning concepts. Every individual's circumstances are different, and financial decisions should be evaluated based on personal goals, tax considerations, employer plan provisions, and overall financial resources.

If you would like to discuss your situation, we invite you to schedule an introductory conversation.

Have Questions About Your Situation?

This resource is intended for educational purposes only. If you would like to discuss your circumstances, schedule an introductory conversation with Scott Brooks, CFP®.

Schedule an Introductory ConversationVentura County, California · Serving Clients Throughout California and Across the United States

Brooks Wealth Management is a Registered Investment Adviser registered with the State of California. Registration does not imply a certain level of skill or training. This content is provided for informational and educational purposes only and should not be construed as investment, tax, legal, or accounting advice. Advisory services are offered only to clients or prospective clients where Brooks Wealth Management and its representatives are properly licensed or exempt from licensure. Investing involves risk, including the potential loss of principal. CFP® is a certification mark owned by the Certified Financial Planner Board of Standards, Inc. Scott Brooks, CFP® · CRD #7227609 · Firm CRD #332237