What Issues Should I Consider If I Lose My Job?

Checklist of financial, insurance, and benefit steps to take immediately after losing a job.

Losing a job can create immediate financial questions around cash flow, health insurance, employee benefits, retirement accounts, and taxes. A thoughtful job loss financial planning process can help you organize the most important decisions and avoid making rushed choices during a stressful transition.

This guide highlights several financial issues to consider after a job loss. It is intended as a general educational resource, not individualized financial, tax, or legal advice.

Immediate Steps After a Job Loss

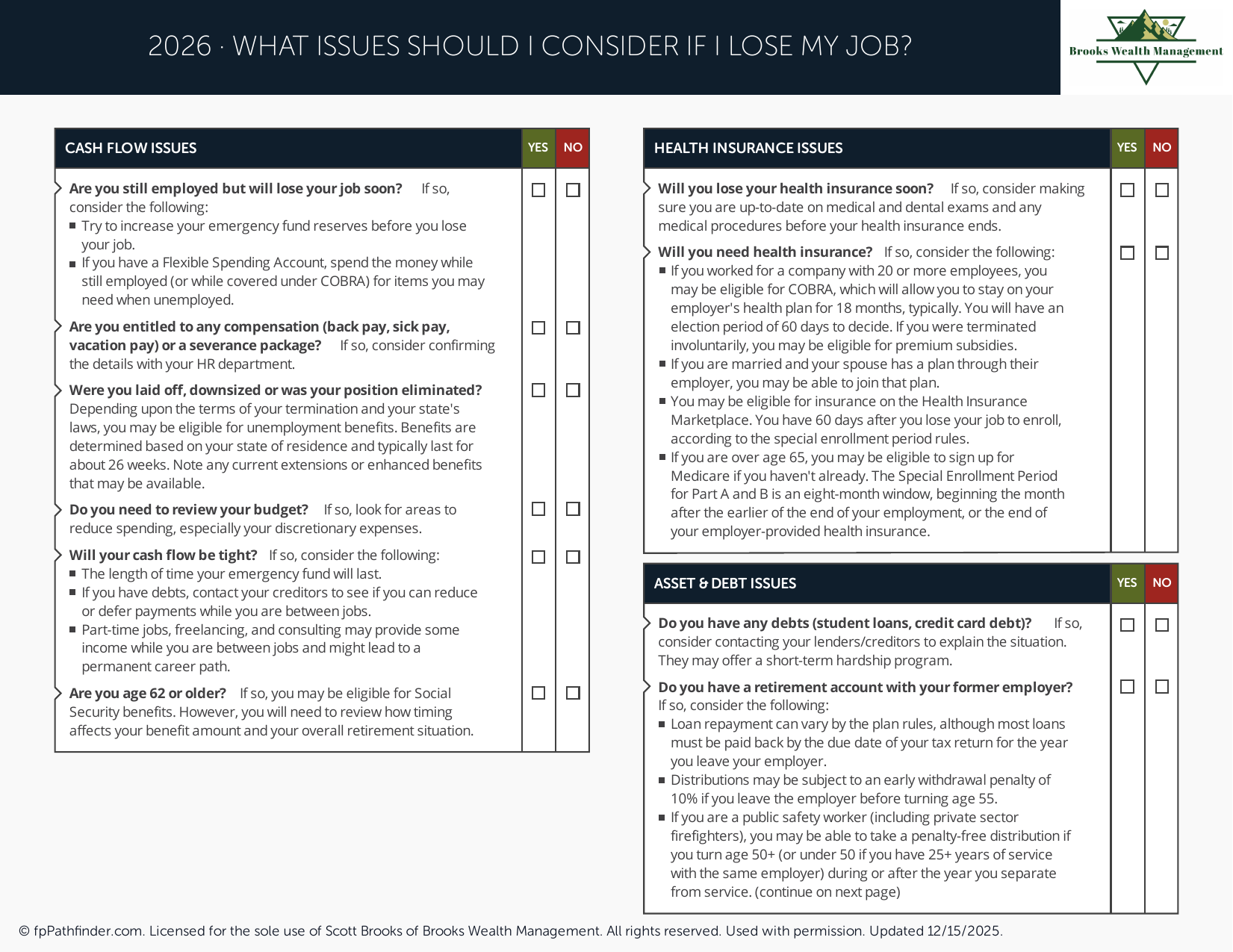

The first step is to review the details of your separation from employment. This may include your final paycheck, severance, unused vacation or PTO, bonus eligibility, equity compensation, deferred compensation, and any deadlines tied to employee benefits. Understanding what income or benefits may still be available can help you build a clearer short-term plan.

Next, review your cash reserves and near-term spending needs. Many households use this period to separate essential expenses from discretionary expenses and determine how long their emergency fund may last. If you are eligible for unemployment benefits, applying promptly may help provide temporary income while you evaluate your next opportunity.

Managing Cash Flow During Unemployment

Cash flow planning becomes especially important after a job loss. This does not always mean cutting every expense immediately, but it does mean being intentional about what continues, what pauses, and what can be reduced temporarily. The goal is to preserve flexibility while you assess your next steps.

Debt payments should also be reviewed carefully. If you have high-interest debt, mortgage payments, student loans, or other obligations, it may be worth understanding available options before cash becomes tight. For more context on debt decisions, you may find our resource on whether you should pay off your debts helpful.

Health Insurance and Employee Benefits

Health insurance is often one of the most important items to address after a job loss. Depending on your situation, you may have access to COBRA, coverage through a spouse or partner’s employer plan, or coverage through the Health Insurance Marketplace or a state exchange. A job loss is generally considered a qualifying life event, which may allow you to enroll outside of the normal open enrollment period.

You should also review other employee benefits, including life insurance, disability insurance, health savings accounts, flexible spending accounts, stock compensation, and any benefits with deadlines. Some decisions may need to be made within a limited window after employment ends.

Retirement Accounts and Tax Planning

Retirement accounts deserve careful attention during a job transition. If you have a 401(k), 403(b), or other employer retirement plan, you may have several options, including leaving the assets in the plan, rolling them into an IRA, moving them to a new employer plan, or taking a distribution. Each option may have different investment, fee, tax, creditor protection, and planning considerations.

In many cases, taking retirement account withdrawals before retirement can create taxes, potential penalties, and long-term planning consequences. Before making a decision, it is important to understand how the choice fits into your broader financial plan. For additional context, our article on whether you should consider a Roth conversion may be useful.

Job Loss Financial Planning and Your Longer-Term Goals

A job loss can affect more than your current income. It may also influence your retirement timeline, savings strategy, investment plan, tax picture, insurance needs, and future career choices. Taking time to revisit your financial plan can help you understand what needs to change and what may still be on track.

For some people, this transition may create an opportunity to reevaluate career goals, compensation structure, relocation plans, or the timing of retirement. If you are closer to retirement, our guide on what issues to consider before retirement may provide additional planning context.

When Professional Guidance May Help

Job loss financial planning can involve several connected decisions, including cash flow, health insurance, severance, taxes, retirement accounts, investments, and estate planning. A financial advisor can help organize those decisions and coordinate with your tax and legal professionals where appropriate.

Brooks Wealth Management provides financial planning and wealth management services for professionals, business owners, retirees, and families. You can learn more about our approach on our pricing page or explore additional educational materials through our free resources.

About This Resource

This resource provides general educational information regarding financial considerations that may arise after a job loss, including cash flow planning, employee benefits, health insurance options, retirement accounts, and other financial decisions. Every individual’s circumstances are different, and strategies should be evaluated based on personal goals, financial resources, tax considerations, and employment opportunities.

If you would like to discuss your situation, we invite you to visit our contact page to schedule an introductory conversation.

Have Questions About Your Situation?

This resource is intended for educational purposes only. If you would like to discuss your circumstances, schedule an introductory conversation with Scott Brooks, CFP®.

Schedule an Introductory ConversationVentura County, California · Serving Clients Throughout California and Across the United States

Brooks Wealth Management is a Registered Investment Adviser registered with the State of California. Registration does not imply a certain level of skill or training. This content is provided for informational and educational purposes only and should not be construed as investment, tax, legal, or accounting advice. Advisory services are offered only to clients or prospective clients where Brooks Wealth Management and its representatives are properly licensed or exempt from licensure. Investing involves risk, including the potential loss of principal. CFP® is a certification mark owned by the Certified Financial Planner Board of Standards, Inc. Scott Brooks, CFP® · CRD #7227609 · Firm CRD #332237