Taxation Guide to Withdrawals and Income Sources

Reference guide summarizing the federal income tax treatment of common retirement income sources and withdrawals.

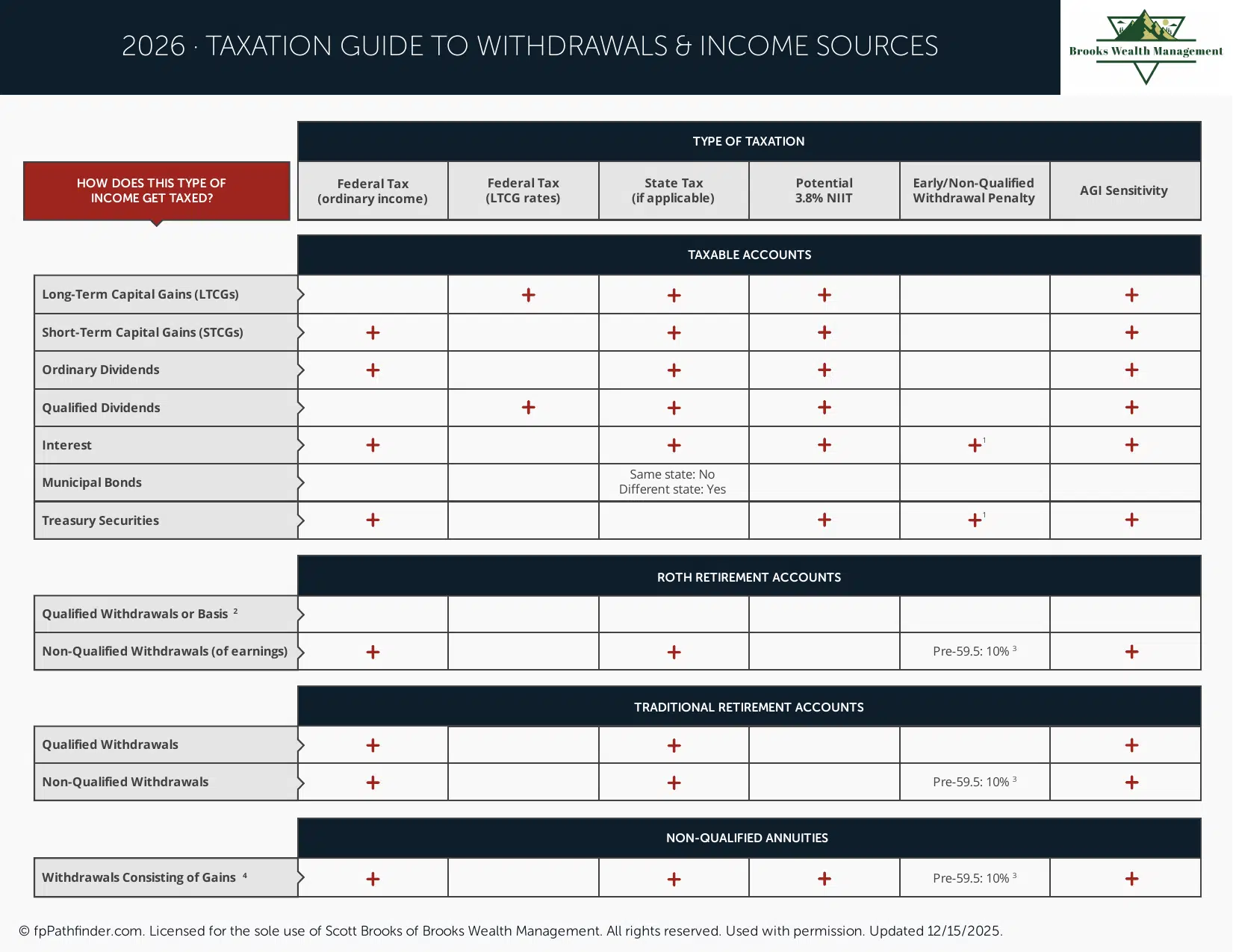

How Are Withdrawals From Different Accounts Taxed?

The tax treatment of withdrawals depends on the type of account, the source of the funds, and the circumstances surrounding the distribution. Understanding how different accounts are taxed may help individuals evaluate retirement income strategies, tax planning opportunities, and long-term financial decisions.

Because different accounts receive different tax treatment, many investors review withdrawals within the context of their overall financial plan rather than evaluating each account independently.

Traditional IRAs and Employer Retirement Plans

Distributions from traditional IRAs, traditional 401(k) plans, traditional 403(b) plans, and similar pre-tax retirement accounts are generally taxed as ordinary income when withdrawn.

In many cases, contributions to these accounts were made on a pre-tax basis or received tax-deferred treatment while invested. As a result, distributions are generally included in taxable income when withdrawn.

Additional rules may apply to withdrawals made before age 59½, although certain exceptions may be available under specific circumstances.

Roth IRAs and Roth Retirement Accounts

Roth accounts are generally funded with after-tax dollars. Qualified distributions from Roth IRAs and Roth employer-sponsored retirement accounts may be received free from federal income tax if applicable requirements are satisfied.

The tax treatment of Roth withdrawals depends on factors such as account age, the type of withdrawal, and whether applicable distribution requirements have been met.

If you are evaluating tax planning opportunities involving Roth accounts, you may find our resource on Roth conversions helpful.

Taxable Brokerage Accounts

Withdrawals from taxable brokerage accounts are generally not taxable simply because money is transferred from the account. However, taxes may apply when investments are sold and a capital gain is realized.

Capital gains may receive different tax treatment depending on the holding period and other factors. Dividends and interest generated within taxable accounts may also be subject to taxation during the year they are received.

Investment basis, holding periods, and capital gains reporting can all affect the tax consequences associated with taxable investment accounts.

Health Savings Accounts (HSAs)

Health Savings Accounts receive unique tax treatment. Qualified withdrawals used for eligible medical expenses are generally tax-free under current federal tax rules.

Withdrawals used for non-qualified purposes may be subject to income taxes and, in certain circumstances, additional penalties.

Because HSA rules can be complex, individuals should maintain records supporting qualified medical expenses and consult qualified tax professionals when appropriate.

Social Security Benefits

Social Security benefits may be subject to federal income taxation depending on an individual's total income and filing status. The percentage of benefits included in taxable income varies based on applicable IRS rules and individual circumstances.

You may find our guide on Social Security retirement benefits helpful if you are evaluating claiming and income planning decisions.

Rental Income and Other Income Sources

Individuals may also receive income from rental properties, business interests, pensions, annuities, deferred compensation arrangements, trusts, or other financial assets. Each source may have its own tax treatment and reporting requirements.

Depending on the circumstances, income may be taxed as ordinary income, capital gains, return of basis, or another classification under applicable tax rules.

Required Minimum Distributions (RMDs)

Certain retirement accounts are subject to Required Minimum Distribution (RMD) rules. These rules generally require account owners to begin taking distributions once they reach the applicable age established under current law.

Failure to satisfy RMD requirements may result in penalties. Because RMD rules can change over time, individuals should review current IRS guidance and consult qualified professionals when evaluating retirement withdrawal strategies.

Individuals approaching retirement may also find our guide on issues to consider before retirement helpful.

How Withdrawal Decisions Fit Within a Financial Plan

Withdrawals often affect more than just income taxes. Distribution decisions may influence Medicare premiums, Social Security taxation, tax brackets, charitable planning opportunities, estate planning considerations, and long-term retirement projections.

As a result, many individuals evaluate withdrawal decisions within the context of a broader financial plan that considers multiple income sources and long-term objectives.

For additional financial planning resources, visit our free resource library.

When Professional Guidance May Be Helpful

Retirement distributions, taxable investment accounts, Social Security benefits, and other income sources can involve complex tax considerations. Individuals evaluating withdrawal strategies may benefit from coordinating with qualified tax professionals and financial advisors.

Brooks Wealth Management works with professionals, business owners, retirees, and families on a wide range of financial planning topics, including retirement income planning, tax-aware financial planning, and wealth management. You can learn more about our approach on our pricing page.

About This Resource

This resource provides general educational information regarding retirement account withdrawals, taxable investment accounts, Social Security benefits, and related tax concepts. Every individual's circumstances are different, and financial decisions should be evaluated based on personal goals, tax considerations, account structures, and applicable laws.

If you would like to discuss your situation, we invite you to schedule an introductory conversation.

Have Questions About Your Situation?

This resource is intended for educational purposes only. If you would like to discuss your circumstances, schedule an introductory conversation with Scott Brooks, CFP®.

Schedule an Introductory ConversationVentura County, California · Serving Clients Throughout California and Across the United States

Brooks Wealth Management is a Registered Investment Adviser registered with the State of California. Registration does not imply a certain level of skill or training. This content is provided for informational and educational purposes only and should not be construed as investment, tax, legal, or accounting advice. Advisory services are offered only to clients or prospective clients where Brooks Wealth Management and its representatives are properly licensed or exempt from licensure. Investing involves risk, including the potential loss of principal. CFP® is a certification mark owned by the Certified Financial Planner Board of Standards, Inc. Scott Brooks, CFP® · CRD #7227609 · Firm CRD #332237