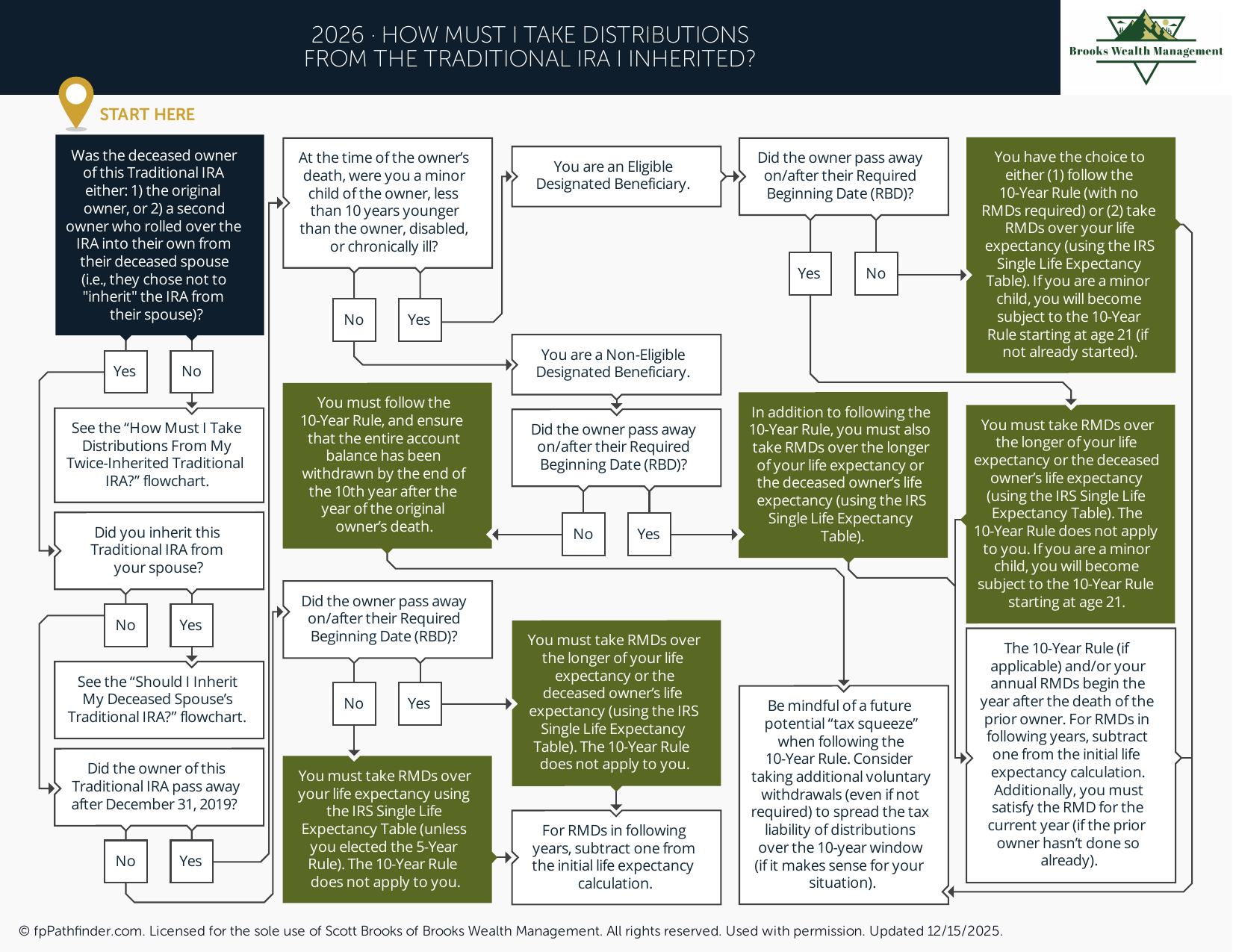

How Must I Take Distributions from the Traditional IRA I Inherited?

Decision flowchart for RMD rules on an inherited traditional IRA.

What Should I Know About Inherited IRA Distributions?

Inherited IRA distribution rules depend on your relationship to the original account owner, the type of IRA inherited, and whether the original owner had already begun taking required minimum distributions. Understanding these rules is important because distribution requirements can affect taxes, investment growth, and long-term financial planning.

Many beneficiaries discover that inherited IRAs come with deadlines and distribution requirements that differ significantly from their own retirement accounts. Reviewing these issues early may help avoid penalties and unexpected tax consequences.

Review Your Beneficiary Classification

The distribution rules for an inherited IRA often begin with determining how the IRS classifies the beneficiary. Different categories of beneficiaries may be subject to different distribution schedules.

- Surviving spouse

- Eligible designated beneficiary

- Non-spouse designated beneficiary

- Trust, estate, or other entity beneficiary

Your beneficiary classification may determine whether distributions can be stretched over life expectancy or whether the 10-year rule applies.

Review Whether the 10-Year Rule Applies

Many inherited IRAs are now subject to the SECURE Act 10-year distribution rule. Under this rule, the entire account balance generally must be distributed by the end of the tenth year following the original owner's death.

- Date of death of the original owner

- Beneficiary classification

- IRA type

- Distribution timing considerations

Individuals often review how distributions may be spread across the 10-year period rather than waiting until the final year.

Review Required Minimum Distribution Requirements

Some beneficiaries may be required to take annual required minimum distributions during the 10-year period. Whether annual distributions are required can depend on whether the original owner had already reached their required beginning date.

- Original owner's age at death

- Whether RMDs had started

- Annual withdrawal requirements

- Potential penalties for missed distributions

Distribution requirements have evolved through IRS guidance, making it important to review current rules when planning withdrawals.

Review Traditional IRA Versus Roth IRA Treatment

The tax treatment of inherited IRA distributions often depends on whether the inherited account is a traditional IRA or a Roth IRA.

- Traditional IRA distributions may be taxable as ordinary income

- Qualified Roth IRA distributions are generally tax-free

- Five-year Roth IRA rules may apply

- Distribution timing considerations may differ

Reviewing the account type may help determine how inherited IRA distributions could affect future tax returns.

Review Spousal Beneficiary Options

Surviving spouses typically have more flexibility than other beneficiaries when inheriting an IRA. Several options may be available depending on age, retirement goals, and income needs.

- Treating the IRA as your own

- Completing a spousal rollover

- Maintaining the account as an inherited IRA

- Reviewing future RMD implications

The most appropriate option often depends on individual circumstances and retirement planning objectives.

Review the Tax Impact of Future Distributions

Inherited IRA distributions may affect taxable income, Medicare premiums, tax brackets, and other planning considerations. Individuals often review how distribution timing could affect future tax obligations.

- Current income levels

- Expected future income

- Potential tax bracket changes

- Medicare IRMAA considerations

Spreading distributions over multiple years may be appropriate in some situations, while other circumstances may favor larger withdrawals earlier or later.

Review How the Inherited IRA Fits Into Your Broader Financial Plan

An inherited IRA may affect retirement planning, estate planning, tax planning, and investment strategy. Reviewing the inherited account alongside other assets may help create a more coordinated financial plan.

- Retirement income planning

- Estate planning goals

- Investment allocation

- Tax-efficient withdrawal strategies

Additional resources that may be helpful include Roth conversions, retirement planning considerations, and account selection decisions available in the free resource library.

About This Resource

This resource provides general educational information regarding inherited IRA distributions and beneficiary planning. Individuals often review inherited IRA rules when evaluating distribution requirements, tax consequences, retirement planning opportunities, and estate planning considerations.

The rules governing inherited IRAs depend on multiple factors, including beneficiary classification, account type, and the age of the original account owner at death. Distribution requirements and tax rules may change over time.

This resource is intended to help identify the major issues that may be relevant when evaluating inherited IRA distribution options.

If you would like to discuss how this topic fits into your broader financial plan, we invite you to schedule an introductory conversation.