Common Deductible Charitable Gifts

Reference guide to types of charitable gifts that qualify for a federal income tax deduction.

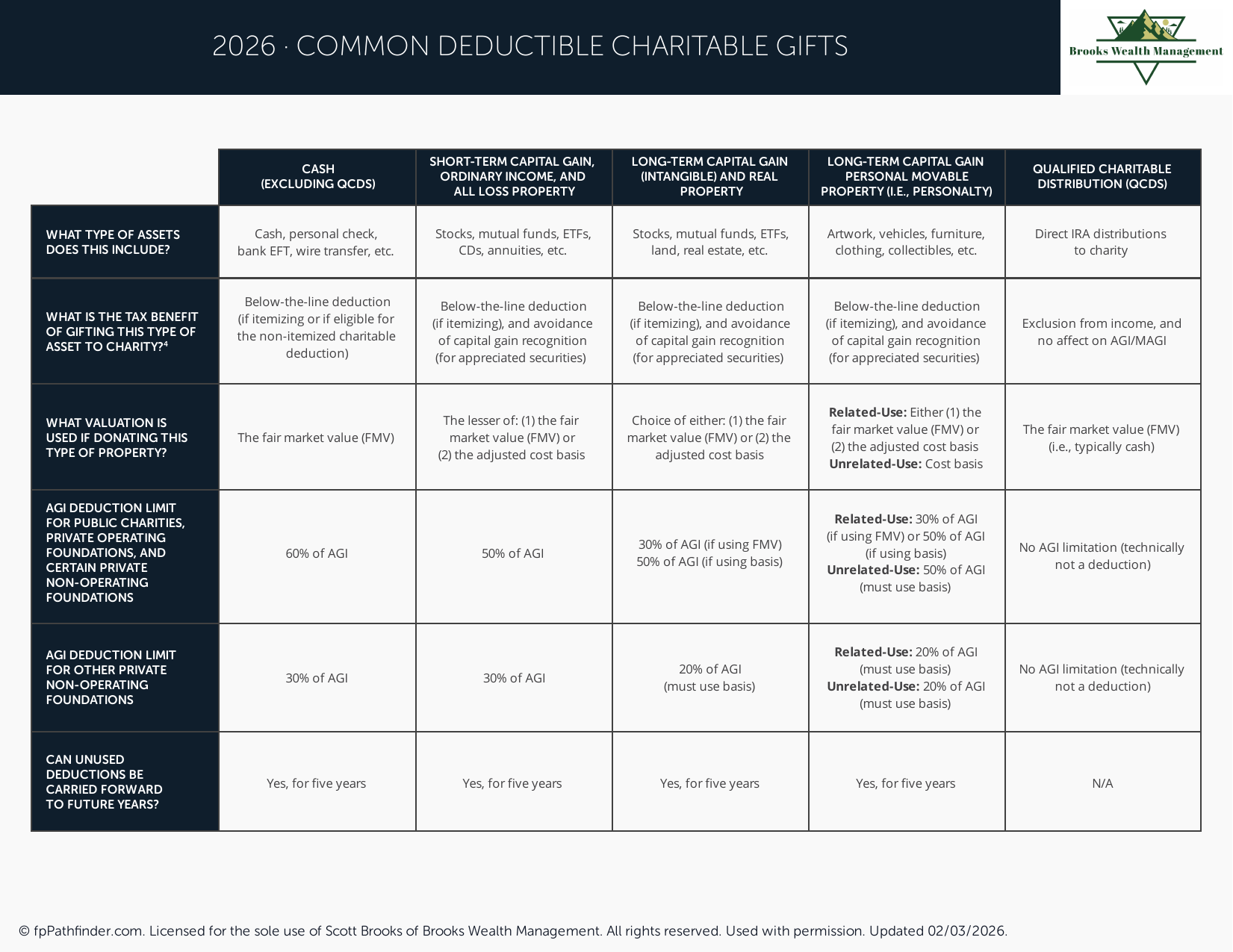

Understanding Qualified Charitable Distributions (QCDs) from Your IRA

As a high-income professional or business owner, you're likely looking for smart ways to manage your finances, especially as you approach or navigate retirement. One powerful strategy that often goes overlooked, particularly for those charitably inclined, is the Qualified Charitable Distribution (QCD) from an Individual Retirement Account (IRA). This allows you to directly transfer funds from your IRA to an eligible charity, offering significant tax advantages.

What is a Qualified Charitable Distribution (QCD)?

A Qualified Charitable Distribution is a direct transfer of funds from your IRA custodian to a qualified charity. For individuals aged 70½ or older, QCDs can be an excellent way to satisfy all or part of your Required Minimum Distribution (RMD) without increasing your adjusted gross income (AGI). This is a crucial benefit, as it can help reduce your Medicare premiums and the taxation of Social Security benefits. Understanding the rules around QCDs is essential for maximizing their impact on your financial plan. For more insights into retirement planning, consider reviewing our resources on what issues should I consider before I retire.

Eligibility Requirements for a QCD from Your IRA

To make a valid Qualified Charitable Distribution, several conditions must be met:

- Age Requirement: You must be 70½ or older at the time of the distribution. This is a key distinction from the RMD age, which is currently 73 for many. Even if you're not yet subject to RMDs, you can still make a QCD if you meet the age 70½ threshold.

- IRA Type: The distribution must come from a traditional IRA, Roth IRA, SEP IRA, or SIMPLE IRA. However, if you have made non-deductible contributions to a traditional IRA, the QCD will be considered to come first from the taxable portion of your IRA.

- Direct Transfer: The funds must be transferred directly from your IRA custodian to the qualified charity. You cannot take the distribution yourself and then donate it; it must be a trustee-to-charity transfer.

- Qualified Charity: The recipient must be a 501(c)(3) organization. Donor-advised funds, private foundations, and supporting organizations are generally not eligible. It's always wise to verify a charity's status before initiating a QCD.

- Maximum Amount: There's an annual limit on the amount you can exclude from income as a QCD, which is $105,000 per taxpayer for 2024 (indexed for inflation). This limit applies per individual, so a married couple filing jointly could exclude up to $210,000 if each spouse makes a QCD from their own IRA.

The Tax Benefits of a Qualified Charitable Distribution

The primary advantage of a Qualified Charitable Distribution is its tax efficiency. Unlike a regular IRA distribution, which is typically taxable income, a QCD is excluded from your gross income. This means:

- Lower AGI: By reducing your AGI, a QCD can help you avoid higher Medicare Part B and D premiums, which are based on your income. It can also reduce the taxable portion of your Social Security benefits. Learn more about Social Security benefits.

- Satisfy RMDs: If you are 73 or older and subject to RMDs, a QCD can count towards satisfying your annual RMD requirement. This is particularly beneficial if you don't need the RMD funds for living expenses and prefer to support a cause you care about.

- No Itemization Needed: You don't need to itemize deductions to receive the tax benefit of a QCD. This is a significant advantage, especially with the higher standard deduction amounts.

How to Initiate a QCD from Your IRA

Initiating a Qualified Charitable Distribution is typically straightforward, but it requires careful coordination with your IRA custodian and the charity. Here's a general process:

- Identify Your Charity: Choose one or more qualified 501(c)(3) organizations you wish to support.

- Contact Your IRA Custodian: Inform your IRA custodian that you intend to make a QCD. They will provide the necessary forms or instructions.

- Direct Transfer: The custodian will issue a check directly to the charity or provide you with a check made out to the charity that you can then forward. Ensure the check is payable to the charity, not to you.

- Keep Records: Maintain thorough records of the transaction, including the amount, the charity's name, and confirmation from your IRA custodian. The charity should also provide an acknowledgment of your donation.

It's crucial to ensure all steps are followed correctly to ensure the distribution qualifies for the tax exclusion. If you have questions about managing your investments or charitable giving strategies, we invite you to explore our free resources or consider our pricing for personalized advice.

Important Considerations for Your QCD Strategy

While the Qualified Charitable Distribution offers compelling benefits, it's important to consider your overall financial picture. For instance, if you're considering other tax-efficient strategies like a Roth conversion, understanding how a QCD interacts with your AGI can be vital. Always consult with a qualified financial advisor to ensure this strategy aligns with your comprehensive financial plan.

About This Resource

At Brooks Wealth Management, we are dedicated to providing clear, actionable financial guidance to high-income professionals and business owners in Denver, Colorado. Our goal is to help you navigate complex financial decisions with confidence. If you have further questions about Qualified Charitable Distributions or wish to discuss your broader financial planning needs, we encourage you to book a consultation with our team. Visit our contact page to schedule your appointment today.

Have Questions About Your Situation?

This resource is a starting point. A free consultation with Scott Brooks, CFP® gives you a personalized perspective.

Book a Free ConsultationBased in Westlake Village, CA · Ventura County · Serving clients across all 50 states

Brooks Wealth Management is a Registered Investment Adviser (RIA) in the State of California. Registration does not imply a certain level of skill or training. This resource is provided for educational and informational purposes only and does not constitute investment, tax, or legal advice. Scott Brooks, CFP® · CRD #7227609 · Firm CRD #332237 · 2555 Townsgate Rd STE 200, Westlake Village, CA 91361