Common Annuity Products

Reference guide comparing fixed, variable, indexed, and income annuity product types.

What Should You Review Before Purchasing an Annuity Product?

Annuity products are insurance contracts that may provide tax-deferred growth, future income payments, principal protection features, or a combination of these benefits. Whether an annuity is appropriate depends on an individual's financial goals, income needs, liquidity requirements, and overall retirement strategy.

Because annuities can vary significantly in structure and cost, individuals often review the specific features, risks, and limitations of a contract before making a decision.

Review What an Annuity Product Is

An annuity is a contract issued by an insurance company. In exchange for a lump-sum contribution or a series of payments, the insurer agrees to provide certain contractual benefits, which may include future income payments, accumulation opportunities, or death benefit provisions.

Common considerations include:

- When income payments may begin.

- Whether account values fluctuate with investment markets.

- How withdrawals are treated.

- What guarantees are provided by the contract.

- The financial strength of the issuing insurance company.

Annuities are often reviewed alongside other retirement planning tools, including employer-sponsored retirement plans, IRAs, taxable investment accounts, pensions, and Social Security benefits.

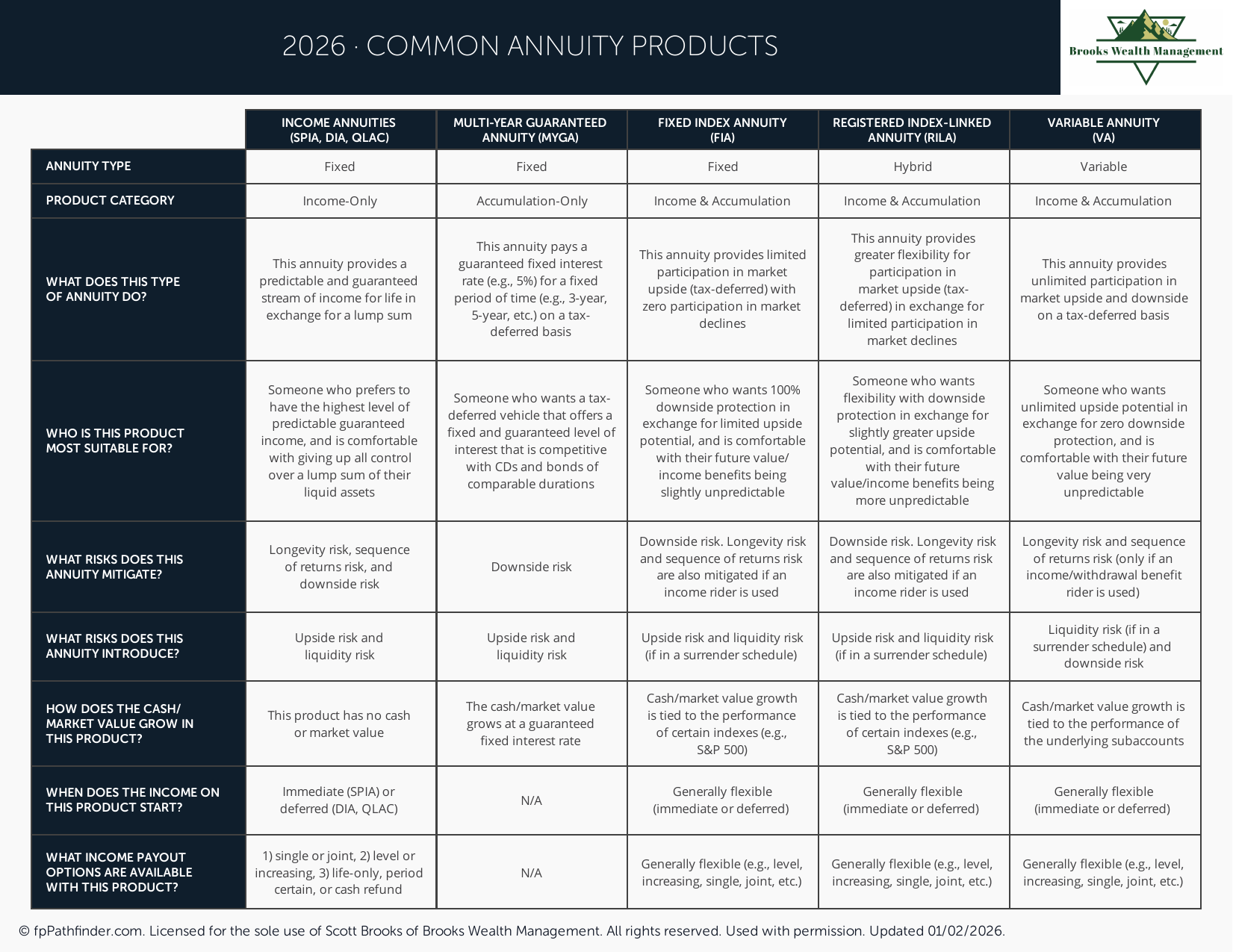

Review Fixed Annuity Products

Fixed annuities generally provide a stated rate of interest or a guaranteed accumulation schedule for a specified period.

Individuals often review fixed annuities when seeking:

- Predictable growth.

- Reduced market exposure.

- Principal protection features.

- Future guaranteed income options.

Because returns are generally determined by contract provisions rather than market performance, fixed annuities may appeal to individuals who prioritize stability and predictability.

Review Variable Annuity Products

Variable annuities allow contract owners to invest in underlying investment options whose values may increase or decrease based on market performance.

Common considerations include:

- Market risk.

- Investment expenses.

- Mortality and expense charges.

- Optional rider costs.

- Income benefit features.

- Tax-deferred growth opportunities.

Variable annuities may provide greater growth potential than fixed annuities, but contract values and future income benefits can vary depending on investment performance and contract provisions.

Review Indexed Annuity Products

Indexed annuities, sometimes referred to as fixed indexed annuities, generally credit interest based on the performance of a market index while also providing varying levels of downside protection.

Common contract features may include:

- Participation rates.

- Interest rate caps.

- Spreads or margin adjustments.

- Minimum guaranteed values.

- Surrender charge schedules.

Although indexed annuities reference market indexes, actual contract performance may differ substantially from the performance of the index itself because of these contractual limitations.

Review Liquidity Considerations

Annuities are generally designed as long-term financial products. Accessing funds before the end of a surrender period may result in charges or restrictions.

Individuals often review:

- Surrender charge schedules.

- Free withdrawal provisions.

- Required access to emergency funds.

- Upcoming retirement spending needs.

- Other available liquid assets.

Maintaining adequate liquidity outside of annuity contracts is a common consideration when evaluating how an annuity fits within an overall financial plan.

Review Costs and Fees

Not all annuities have the same fee structure. Understanding contract costs can be an important part of evaluating the potential benefits and limitations of a particular product.

Depending on the annuity type, common costs may include:

- Mortality and expense charges.

- Administrative fees.

- Investment management expenses.

- Optional rider charges.

- Surrender charges.

Individuals often review both the contractual benefits and associated costs before purchasing an annuity product.

Review Tax Considerations

Annuities generally provide tax-deferred growth, meaning earnings are not typically taxed until withdrawn.

Common considerations include:

- Tax treatment of withdrawals.

- Ordinary income taxation of earnings.

- Early withdrawal penalties when applicable.

- Required minimum distribution rules for qualified contracts.

- Coordination with other retirement income sources.

Tax outcomes depend on individual circumstances and may affect how annuities are incorporated into a broader retirement income strategy.

Individuals reviewing retirement planning strategies may also find it helpful to explore information regarding different savings vehicles, retirement planning considerations, and Roth conversions.

Review How Annuities May Fit Within a Retirement Income Plan

Annuities are often evaluated as one component of a broader retirement income strategy rather than as a standalone solution.

Common questions individuals review include:

- How much guaranteed income is needed to cover essential expenses?

- How much flexibility and liquidity should remain available?

- What role should market-based investments play in retirement?

- How important is leaving assets to beneficiaries?

- How might inflation affect future purchasing power?

The answers to these questions may affect whether an annuity product is appropriate, unnecessary, or suitable only for a portion of a retirement plan.

About This Resource

This resource provides general educational information regarding annuity products and retirement income planning. It is not intended as investment, tax, legal, insurance, healthcare, cybersecurity, or financial advice. Individual circumstances vary, and annuity contract provisions differ among insurance companies.

If you would like to discuss how this topic fits into your broader financial plan, we invite you to schedule an introductory conversation.