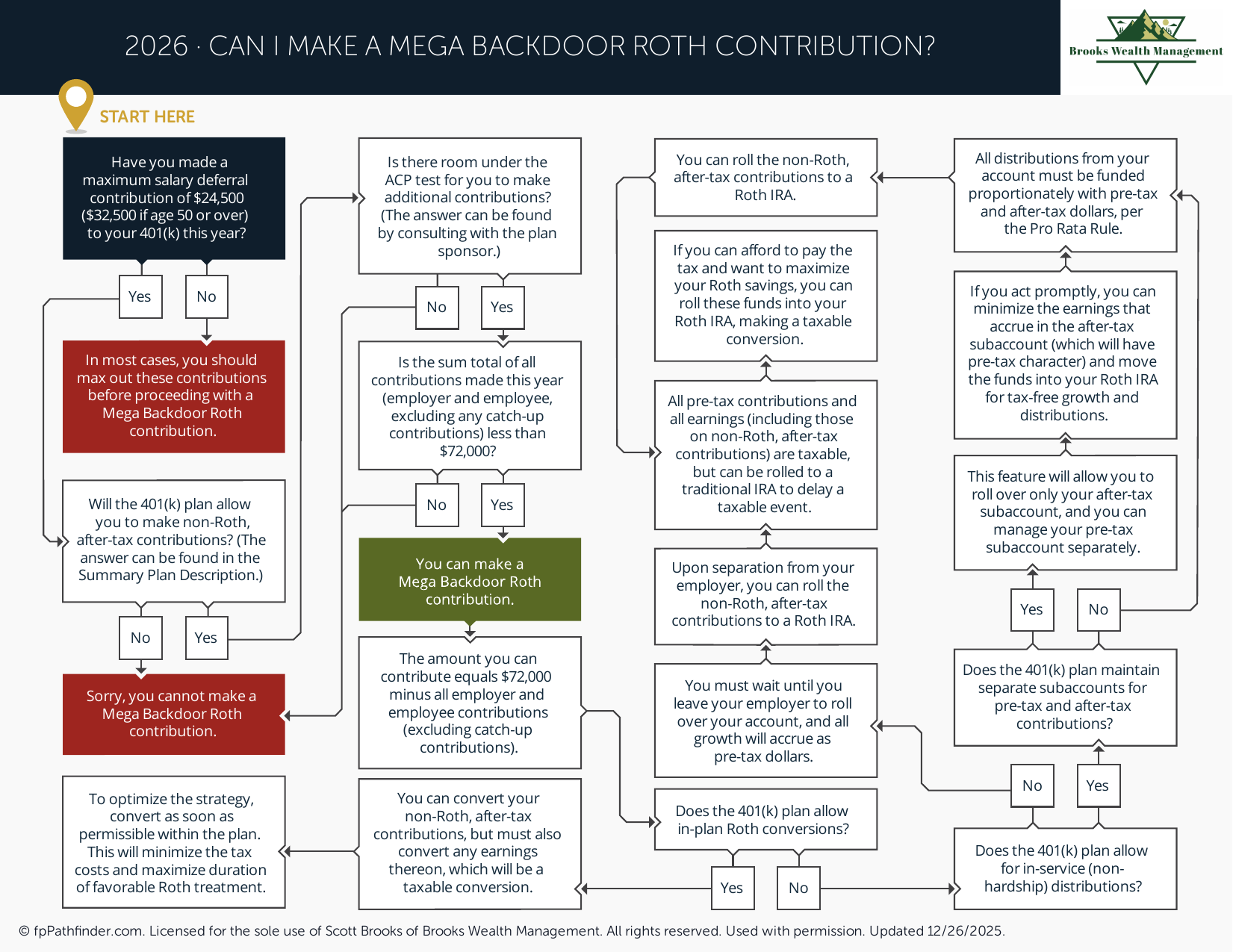

Can I Make a Mega Backdoor Roth Contribution?

Flowchart to determine eligibility and steps for making after-tax 401(k) contributions and converting to Roth.

Can I Make a Mega Backdoor Roth Contribution?

A mega backdoor Roth contribution may allow certain individuals to move additional retirement savings into Roth accounts beyond standard employee contribution limits. Whether this strategy is available depends primarily on the provisions of an employer-sponsored retirement plan and the individual's contribution capacity.

Not all retirement plans permit the features necessary to complete a mega backdoor Roth contribution. Reviewing plan rules and contribution options is typically the first step in determining eligibility.

Review What a Mega Backdoor Roth Contribution Is

A mega backdoor Roth contribution is a retirement savings strategy that generally involves making after-tax contributions to an employer-sponsored retirement plan and subsequently converting those funds to a Roth account.

This strategy differs from a traditional Roth conversion because it typically uses after-tax retirement plan contributions rather than converting pre-tax IRA or retirement account balances.

Common reasons individuals review this strategy include:

- Building additional Roth assets.

- Increasing retirement savings beyond standard employee contribution limits.

- Diversifying future retirement income sources.

- Evaluating long-term tax planning opportunities.

Individuals interested in Roth savings strategies may also find it helpful to review Roth 401(k) contribution considerations.

Review Whether Your Retirement Plan Allows After-Tax Contributions

One of the primary requirements for a mega backdoor Roth contribution is access to a retirement plan that permits after-tax employee contributions.

Many retirement plans allow pre-tax salary deferrals and Roth salary deferrals but do not permit separate after-tax contributions.

Common considerations include:

- Whether after-tax contributions are available.

- Contribution restrictions imposed by the plan.

- Administrative procedures required to make after-tax contributions.

- Coordination with employer matching or profit-sharing contributions.

Plan documents or the plan administrator can generally provide information regarding available contribution types.

Review Whether Your Plan Allows Roth Conversions or Rollovers

In addition to allowing after-tax contributions, a retirement plan generally must permit movement of those funds into a Roth account.

This may occur through:

- An in-service distribution to a Roth IRA.

- An in-plan Roth conversion.

- Other rollover provisions available within the plan.

If a plan does not allow one of these options, implementing a mega backdoor Roth contribution strategy may not be possible.

Individuals often review both requirements before evaluating whether the strategy is available through their employer-sponsored plan.

Review Contribution Limit Considerations

Mega backdoor Roth contributions are often discussed because they may allow additional retirement savings beyond standard employee salary deferral limits.

However, employer retirement plans are subject to annual contribution limits that generally include:

- Employee pre-tax contributions.

- Employee Roth contributions.

- Employer matching contributions.

- Employer profit-sharing contributions.

- After-tax employee contributions.

The amount available for after-tax contributions depends on how much of the applicable annual limit has already been used by other contribution sources.

Because contribution limits may change periodically, individuals often review current IRS limits before implementing this strategy.

Additional retirement savings opportunities may also be explored through other savings account options.

Review Potential Tax Considerations

The primary purpose of a mega backdoor Roth contribution is generally to increase Roth assets that may receive favorable tax treatment if applicable requirements are satisfied.

Common considerations include:

- Tax treatment of earnings generated before conversion.

- Timing of conversions or rollovers.

- Coordination with other retirement accounts.

- Retirement income planning objectives.

- Administrative requirements imposed by the plan provider.

Tax outcomes depend on individual circumstances and the manner in which any conversion or rollover is completed.

Individuals evaluating broader Roth planning strategies may also wish to review Roth conversion considerations.

Review Whether a Mega Backdoor Roth Contribution Fits Your Situation

A mega backdoor Roth contribution is commonly reviewed by individuals who:

- Have already maximized traditional retirement plan contributions.

- Have access to a qualifying employer-sponsored retirement plan.

- Desire additional Roth account assets.

- Are evaluating retirement income diversification strategies.

- Have sufficient cash flow to support additional retirement savings.

Whether this strategy is appropriate depends on individual circumstances, retirement objectives, available plan features, and broader financial planning considerations.

Additional educational resources can be found in our free resources library.

About This Resource

This resource provides general educational information regarding mega backdoor Roth contributions and employer-sponsored retirement plans. It is not intended as investment, tax, legal, insurance, healthcare, cybersecurity, or financial advice. Individual circumstances vary, retirement plan provisions differ, and contribution limits may change over time.

If you would like to discuss how this topic fits into your broader financial plan, we invite you to schedule an introductory conversation.

Can I Make a Mega Backdoor Roth Contribution?

Flowchart to determine eligibility and steps for making after-tax 401(k) contributions and converting to Roth.

Can I Make a Mega Backdoor Roth Contribution?

A mega backdoor Roth contribution is a retirement savings strategy that may allow individuals to move additional funds into Roth accounts beyond the standard Roth IRA contribution limits. The strategy generally involves making after-tax contributions to an employer-sponsored retirement plan and subsequently converting those funds to a Roth account.

Whether this strategy is available depends largely on the provisions of an employer's retirement plan. Not all plans permit the features necessary to implement a mega backdoor Roth contribution.

Review What a Mega Backdoor Roth Contribution Is

A mega backdoor Roth contribution is distinct from both a direct Roth IRA contribution and a traditional Roth conversion.

The strategy generally involves three steps:

- Making after-tax contributions to a qualified employer retirement plan.

- Accumulating funds within the plan.

- Converting or rolling those after-tax contributions into a Roth account.

Individuals often review this strategy after maximizing traditional employee salary deferrals and other available retirement savings opportunities.

Those evaluating Roth savings options may also wish to review whether a Roth 401(k) contribution may be appropriate.

Review Whether Your Retirement Plan Allows After-Tax Contributions

The first requirement for a mega backdoor Roth strategy is that the employer retirement plan permits after-tax employee contributions.

Many plans allow traditional pre-tax contributions and Roth salary deferrals but do not permit separate after-tax contributions.

Common considerations include:

- Whether after-tax contributions are available.

- Contribution limits established by the plan.

- Administrative procedures required by the plan provider.

- Restrictions on contribution timing.

Plan documents or the plan administrator can typically provide information regarding available contribution types.

Review Whether the Plan Allows Roth Conversions or Rollovers

In addition to allowing after-tax contributions, a retirement plan generally must permit movement of those funds into a Roth account.

This may occur through:

- An in-plan Roth conversion.

- An in-service distribution to a Roth IRA.

- Other rollover provisions available within the plan.

Without one of these mechanisms, implementing a mega backdoor Roth strategy may not be possible even if after-tax contributions are allowed.

Individuals often review both requirements together before evaluating whether this strategy is available.

Review Contribution Limit Considerations

Mega backdoor Roth strategies are often discussed because they may allow individuals to contribute amounts beyond standard employee salary deferral limits.

However, retirement plans are subject to overall annual contribution limits that generally include:

- Employee pre-tax contributions.

- Employee Roth contributions.

- Employer matching contributions.

- Employer profit-sharing contributions.

- After-tax employee contributions.

The amount available for after-tax contributions may depend on how much of the annual limit has already been used by other contribution sources.

Because retirement plan limits can change periodically, individuals often review current IRS limits before implementing this strategy.

Review Potential Tax Considerations

One reason individuals consider a mega backdoor Roth contribution is the possibility of moving funds into a Roth environment where future qualified withdrawals may receive favorable tax treatment.

Common considerations include:

- Tax treatment of earnings generated before conversion.

- Timing of conversions.

- Coordination with existing retirement accounts.

- Plan-specific administrative procedures.

- Potential reporting requirements.

The tax treatment of any transaction depends on individual circumstances and the manner in which the conversion is completed.

Review Whether a Mega Backdoor Roth Strategy Fits Your Situation

A mega backdoor Roth contribution is commonly reviewed by individuals who:

- Have already maximized traditional retirement contributions.

- Have access to a qualifying employer retirement plan.

- Desire additional Roth assets.

- Are evaluating long-term retirement income planning strategies.

- Have sufficient cash flow to support additional retirement savings.

Whether this strategy is appropriate depends on a variety of factors, including current income needs, future retirement goals, tax considerations, and available plan features.

Individuals evaluating additional savings opportunities may also find it helpful to review what accounts to consider when saving more and Roth conversion considerations.

About This Resource

This resource provides general educational information regarding mega backdoor Roth contributions and employer-sponsored retirement plans. It is not intended as investment, tax, legal, insurance, healthcare, cybersecurity, or financial advice. Individual circumstances vary, retirement plan provisions differ, and contribution limits may change over time.

If you would like to discuss how this topic fits into your broader financial plan, we invite you to schedule an introductory conversation.