Can I Make a Deductible Contribution to My HSA?

Flowchart to determine eligibility for making a tax-deductible HSA contribution.

Can I Make a Deductible Contribution to My HSA?

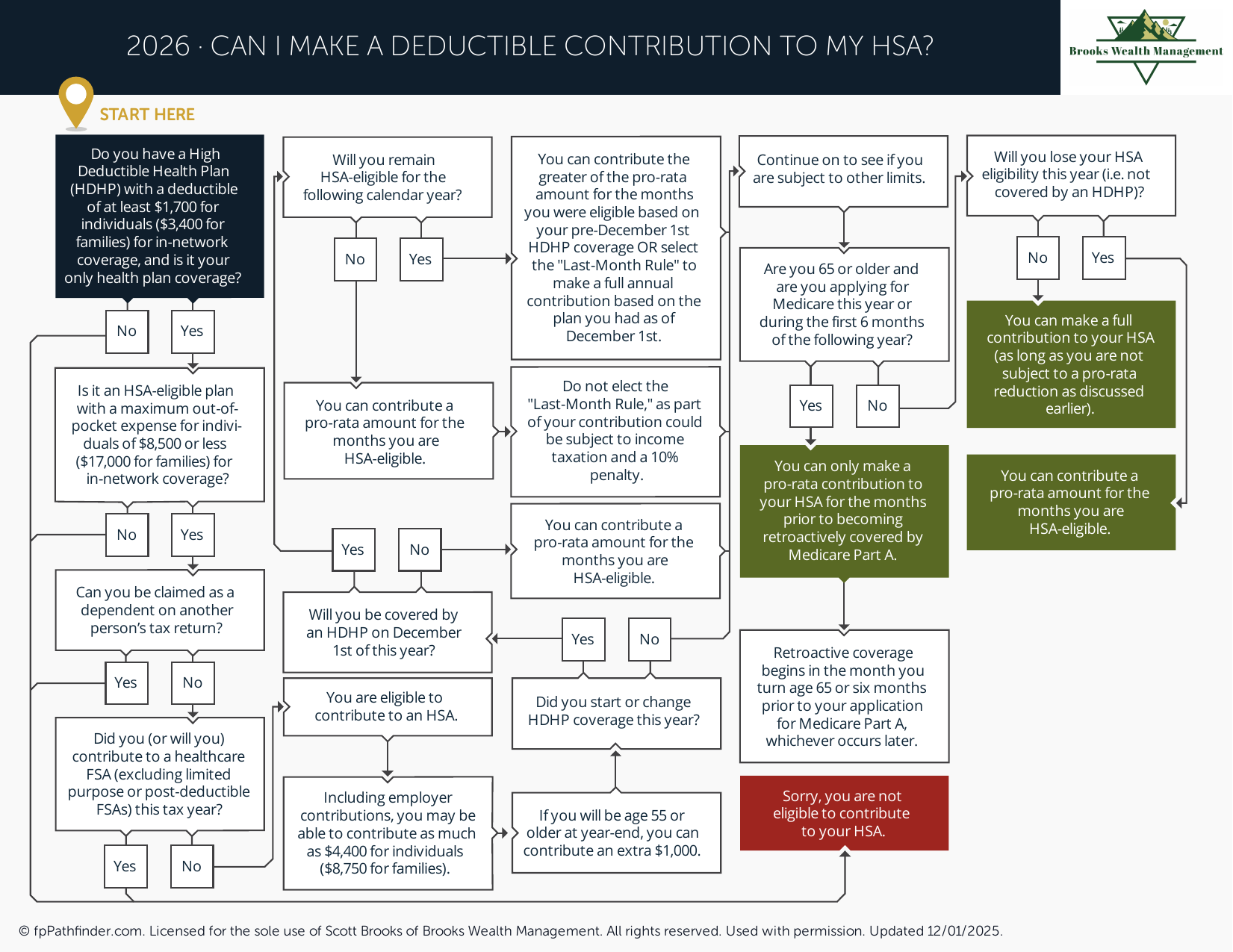

Many individuals who are covered by a qualifying High Deductible Health Plan (HDHP) may be eligible to make deductible contributions to a Health Savings Account (HSA). Eligibility depends on several factors, including health coverage, Medicare enrollment status, and whether an individual can be claimed as a dependent on another taxpayer's return.

HSAs are often reviewed because they may provide favorable tax treatment for qualified medical expenses. Understanding eligibility requirements and contribution rules is an important first step before making contributions.

Review HSA Eligibility Requirements

Before making a deductible HSA contribution, individuals generally must meet specific eligibility requirements.

Common requirements include:

- Coverage under a qualifying High Deductible Health Plan (HDHP).

- No disqualifying health coverage in addition to the HDHP.

- Not being enrolled in Medicare.

- Not being claimed as a dependent on another person's tax return.

Eligibility may change during the year if health coverage changes, so many individuals review their status annually before making contributions.

Review HDHP Coverage Requirements

Health Savings Accounts are generally available only to individuals covered by a qualifying HDHP.

Common considerations include:

- The plan's annual deductible.

- Maximum out-of-pocket limits.

- Whether additional health coverage exists.

- Whether family or self-only coverage applies.

Because IRS requirements may change periodically, individuals often review current HDHP standards before making contributions.

Review HSA Contribution Limits

Annual HSA contribution limits are established by the IRS and may change from year to year.

The amount an individual may contribute generally depends on:

- Whether coverage is self-only or family coverage.

- How long HSA eligibility is maintained during the year.

- Whether employer contributions are made.

- Whether the individual qualifies for catch-up contributions.

Individuals age 55 and older may be eligible to make additional catch-up contributions, subject to applicable IRS rules.

Because both personal and employer contributions count toward annual limits, reviewing total contributions throughout the year may help avoid excess contribution issues.

Review How HSA Contributions Are Made

HSA contributions may be made through payroll deductions, employer contributions, or direct personal contributions.

Common considerations include:

- Employer contribution programs.

- Payroll deduction opportunities.

- Direct contributions made outside payroll.

- Contribution deadlines.

- Record-keeping requirements.

Individuals often review available contribution methods to determine which approach best aligns with their overall financial and tax planning objectives.

Those evaluating broader savings opportunities may also find it helpful to review what accounts to consider when saving more.

Review How HSAs May Fit Into Long-Term Planning

Many individuals use HSAs to pay current medical expenses, while others review whether retaining HSA assets for future healthcare costs may be appropriate.

Common considerations include:

- Current healthcare spending needs.

- Future healthcare expenses.

- Available emergency savings.

- Retirement planning goals.

- Investment options available within the HSA.

Depending on individual circumstances, some account owners choose to maintain a cash balance for near-term expenses, while others review investment options for longer-term growth potential.

HSAs are often evaluated alongside other tax-advantaged accounts such as Roth 401(k) accounts and broader retirement planning strategies.

Review Common HSA Contribution Mistakes

Several common issues may affect HSA eligibility or contribution treatment.

Individuals often review:

- Changes in health insurance coverage.

- Enrollment in Medicare.

- Excess contributions.

- Use of funds for non-qualified expenses.

- Documentation supporting qualified medical expenses.

Maintaining records of contributions, distributions, and medical expenses may help support compliance with applicable tax rules.

Additional educational information is available through our free resources library.

About This Resource

This resource provides general educational information regarding Health Savings Accounts and deductible HSA contributions. It is not intended as investment, tax, legal, insurance, healthcare, cybersecurity, or financial advice. Individual circumstances vary, and contribution limits and eligibility rules may change over time.

If you would like to discuss how this topic fits into your broader financial plan, we invite you to schedule an introductory conversation.