Can I Deduct My Traditional IRA Contribution?

Flowchart to determine whether your traditional IRA contribution is tax-deductible.

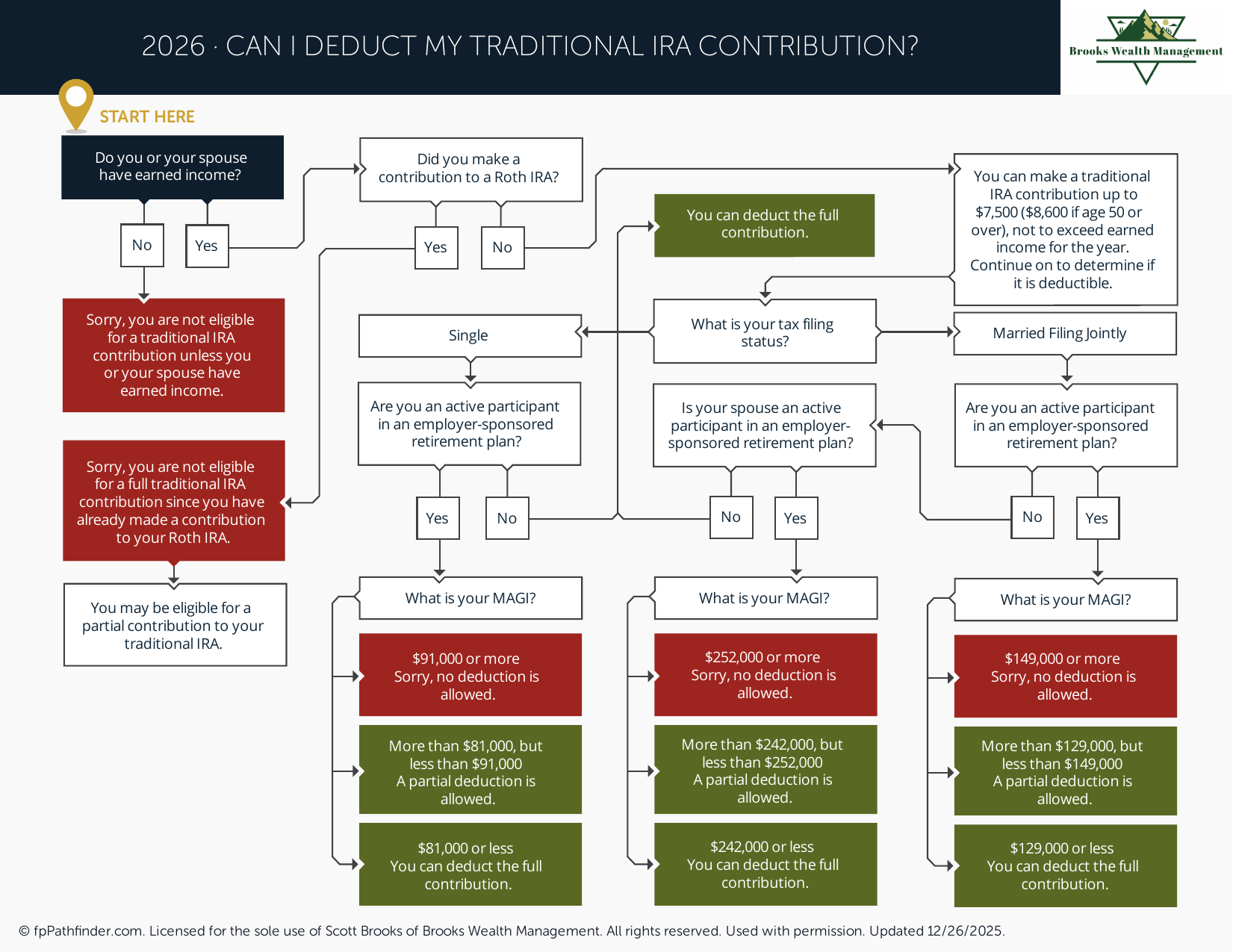

Can I Deduct My Traditional IRA Contribution in 2026?

Whether a traditional IRA contribution is deductible in 2026 depends on income, tax filing status, and whether the individual or spouse is covered by a workplace retirement plan. Some individuals may qualify for a full deduction, while others may receive a partial deduction or no deduction.

Individuals often review traditional IRA deduction rules as part of broader retirement and tax planning. The contribution may still be allowed even when the deduction is limited or unavailable, but the tax treatment can vary based on individual circumstances.

Review Workplace Retirement Plan Coverage

One of the first issues to review is whether the individual, or spouse if married, is covered by a retirement plan at work. Common examples include a 401(k), 403(b), SIMPLE IRA, SEP IRA, or pension plan.

If neither spouse is covered by a workplace retirement plan, a traditional IRA contribution may generally be deductible, subject to the annual IRA contribution limit. If either spouse is covered by a workplace plan, income limits may reduce or eliminate the deduction.

- Whether the individual is covered by a workplace retirement plan

- Whether a spouse is covered by a workplace retirement plan

- Tax filing status

- Modified adjusted gross income

- Annual IRA contribution limits

Individuals reviewing retirement savings options may also find it helpful to review what accounts to consider when saving more.

Review Income Phase-Out Rules

The traditional IRA deduction may be reduced or eliminated when modified adjusted gross income falls within or above IRS phase-out ranges. These ranges can change over time and may differ depending on filing status and workplace plan coverage.

For individuals covered by a workplace retirement plan, the deduction is generally phased out once income reaches certain levels. For married couples filing jointly, the rules may also depend on whether one spouse, both spouses, or neither spouse is covered by a workplace plan.

- A full deduction may be available below the applicable phase-out range

- A partial deduction may apply within the phase-out range

- No deduction may be available above the applicable phase-out range

- Different phase-out rules may apply when only one spouse is covered by a workplace plan

Because these limits can change, individuals often review current IRS guidance before making or deducting a traditional IRA contribution.

Review Non-Deductible Traditional IRA Contributions

If an individual’s income is too high to claim a traditional IRA deduction, they may still be able to make a non-deductible traditional IRA contribution. A non-deductible contribution does not provide an upfront tax deduction, but it may still affect long-term retirement planning.

Non-deductible IRA contributions require careful recordkeeping. IRS Form 8606 is generally used to track basis in traditional IRAs, which may affect how future distributions or conversions are taxed.

- Whether the contribution is deductible or non-deductible

- Whether Form 8606 may be required

- Existing pre-tax IRA balances

- Future distribution taxation

- Potential Roth conversion considerations

Review Backdoor Roth IRA Considerations

Some individuals review non-deductible traditional IRA contributions in connection with a potential backdoor Roth IRA strategy. This generally involves making a non-deductible traditional IRA contribution and then converting some or all of the IRA balance to a Roth IRA.

The tax result may be affected by the pro-rata rule if the individual has other pre-tax IRA balances. Because of this, the presence of traditional IRA, SEP IRA, or SIMPLE IRA assets may affect whether the strategy creates additional taxable income.

- Existing pre-tax IRA balances

- Timing of the contribution and conversion

- Application of the pro-rata rule

- Potential taxable income from the conversion

- Recordkeeping requirements

Individuals comparing retirement account options may also wish to review Roth conversion considerations and Roth 401(k) contribution considerations.

Review How a Traditional IRA Fits Into the Broader Plan

A traditional IRA deduction is only one part of retirement and tax planning. Individuals often compare traditional IRAs with workplace retirement plans, Roth accounts, taxable investment accounts, health savings accounts, and other savings vehicles.

Common considerations include:

- Current tax bracket compared with expected future tax bracket

- Availability of employer retirement plan contributions

- Roth versus pre-tax contribution options

- Cash flow needs and savings capacity

- Long-term retirement income planning

Additional educational materials are available through our free financial resources.

About This Resource

This resource provides general educational information regarding traditional IRA deductions. It is not intended as investment, tax, legal, insurance, healthcare, cybersecurity, or financial advice. Individual circumstances vary and rules may change over time.

If you would like to discuss how this topic fits into your broader financial plan, we invite you to schedule an introductory conversation.