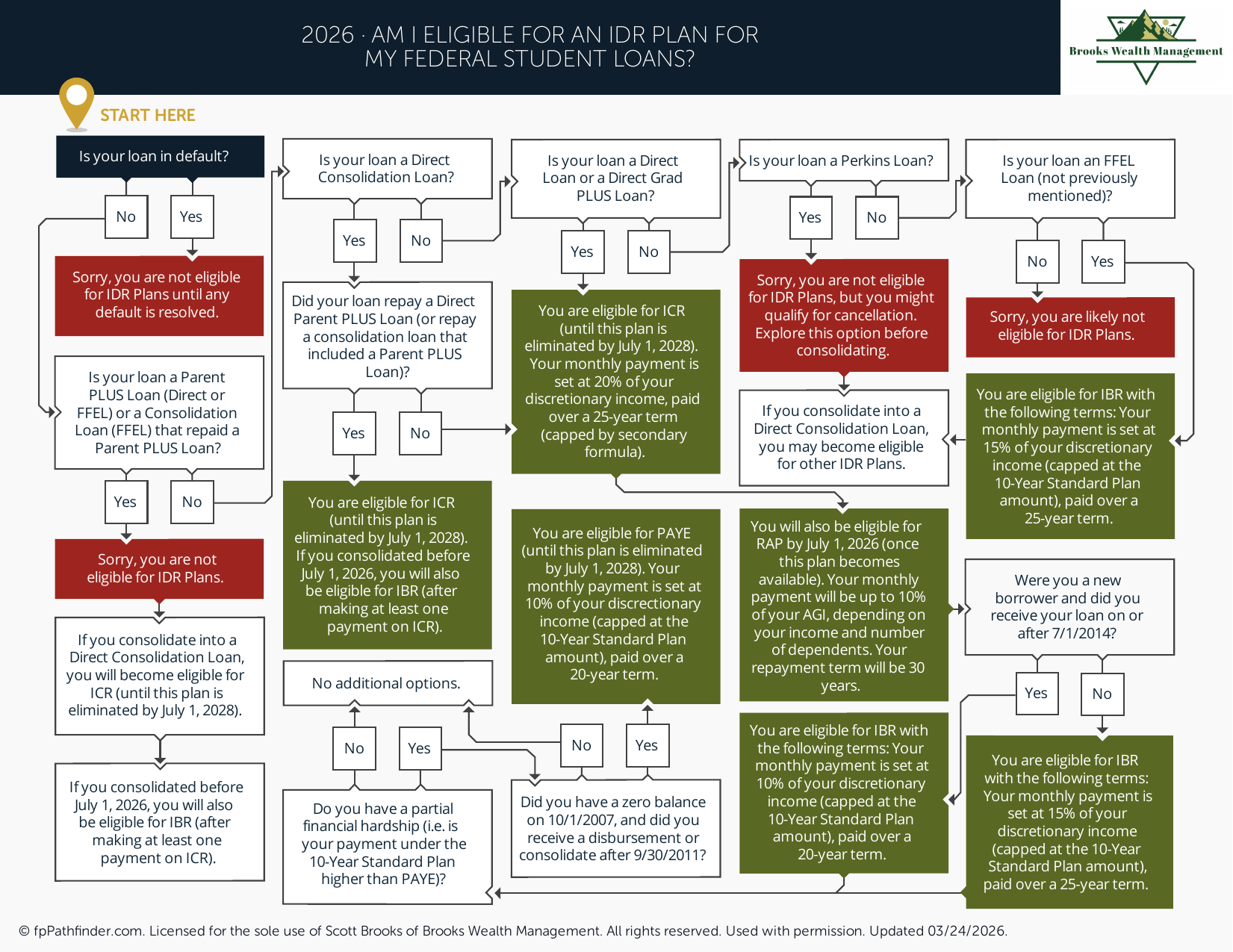

Am I Eligible for an IDR Plan for My Federal Student Loans?

Flowchart to determine eligibility for income-driven repayment (IDR) plans for federal student loans.

Am I Eligible for an Income-Driven Repayment (IDR) Plan for My Federal Student Loans?

Federal student loan borrowers often have multiple repayment options available to them, and one category that receives significant attention is income-driven repayment (IDR) plans. These plans generally calculate monthly payments based on factors such as income, family size, and loan type rather than relying solely on the amount borrowed.

This decision flowchart is designed to help borrowers evaluate whether they may be eligible for an income-driven repayment plan and understand some of the factors that can influence eligibility. Because federal student loan programs and repayment rules can change over time, reviewing current requirements before making a repayment decision is an important part of the process.

Review Your Federal Student Loan Types

Not every federal student loan is treated the same way for repayment purposes. Eligibility for various repayment options often depends on the type of loan involved, how the loan was originated, and whether the borrower has completed any necessary administrative steps.

When evaluating eligibility, borrowers may wish to review:

- The types of federal student loans they currently hold

- Whether loans are held directly by the federal government

- Whether loans have been consolidated

- The repayment status of each loan

- Any prior repayment elections that may affect eligibility

Understanding the underlying loan structure is often the first step when determining whether an income-driven repayment plan may be available.

Review How Income-Driven Repayment Plans Work

Income-driven repayment plans are generally designed to tie monthly student loan payments to a borrower's financial circumstances. Rather than focusing exclusively on the outstanding loan balance, these plans typically incorporate income-related factors when calculating required payments.

Depending on the program and individual circumstances, repayment calculations may consider:

- Reported income

- Family size

- Tax filing status

- Household financial circumstances

- The type of federal loans being repaid

Because these factors can change over time, borrowers enrolled in an income-driven repayment plan may periodically update information to maintain eligibility and ensure payment calculations remain accurate.

Review Eligibility Factors Beyond Income

Although the term "income-driven repayment" emphasizes income, eligibility is often influenced by more than earnings alone. Loan type, repayment history, consolidation status, and administrative requirements may all affect whether a borrower qualifies.

Questions worth reviewing may include:

- Are all loans eligible under the repayment program being considered?

- Has any required consolidation been completed?

- Are loans currently in good standing?

- Have all required applications and certifications been submitted?

- Have repayment program requirements changed since the loans originated?

Eligibility can be more complex than many borrowers initially expect, making it important to review both loan characteristics and personal financial circumstances.

Review Potential Benefits and Tradeoffs

Income-driven repayment plans may offer advantages for certain borrowers, but they are not necessarily appropriate for every situation. Understanding both potential benefits and limitations can help borrowers make more informed decisions.

Considerations often include:

- Monthly payment flexibility

- Cash flow management

- Changes in payment obligations as income changes

- Total repayment costs over time

- Long-term repayment objectives

- Potential loan forgiveness provisions that may apply under certain programs

Evaluating these factors within the context of a broader financial plan can help borrowers understand how student loan repayment decisions may affect other financial goals.

Review How Student Loans Fit Into Your Broader Financial Plan

Student loan repayment decisions rarely exist in isolation. Borrowers are often simultaneously balancing retirement savings, emergency reserves, housing goals, education funding for children, investment decisions, and other financial priorities.

As a result, many individuals find it helpful to evaluate repayment options alongside broader financial planning considerations.

Questions that may be helpful include:

- How do student loan payments affect monthly cash flow?

- Are retirement savings goals remaining on track?

- How does debt repayment interact with other financial priorities?

- Are there competing savings objectives that require attention?

- Would changes in income alter the repayment strategy?

Additional resources that may be helpful include Where Should My Next Dollar Go?, What Accounts Should I Consider If I Want to Save More?, and What Issues Should I Consider Before I Retire?.

Review Ongoing Monitoring Requirements

Borrowers who qualify for an income-driven repayment plan may need to periodically review and update information. Changes in income, family circumstances, employment, tax filing status, or federal program rules can affect repayment obligations and eligibility.

Periodic review may help borrowers:

- Maintain eligibility for the selected repayment program

- Understand changes to monthly payment requirements

- Monitor the impact of income changes

- Evaluate whether a different repayment option may become appropriate

- Stay informed regarding updates to federal student loan programs

Because repayment plans can extend over many years, ongoing review may be just as important as the initial enrollment decision.

Review Documentation and Recordkeeping

Maintaining accurate records can help simplify repayment management and support future decision-making. Documentation may be particularly important when repayment calculations depend on income information or other personal circumstances.

Records borrowers commonly retain include:

- Loan statements

- Repayment plan documentation

- Income verification records

- Tax returns and related filings

- Program correspondence and notices

- Repayment history records

Organized recordkeeping may help borrowers navigate future program updates and maintain a clear understanding of their repayment status.

About This Resource

This decision flowchart was created to help borrowers evaluate whether they may be eligible for an income-driven repayment plan for federal student loans. The objective is to provide a structured framework for reviewing common considerations such as loan type, income factors, repayment requirements, ongoing eligibility obligations, and broader financial planning implications.

Every borrower's circumstances are unique. Factors such as income, family size, loan structure, repayment objectives, and future financial goals can all influence eligibility and repayment decisions. Reviewing these issues carefully may help borrowers better understand available options and how those options fit within their overall financial picture.

This resource is provided for educational purposes only and should not be construed as financial, tax, legal, or student loan advice. Individuals should consult appropriate professionals and official program resources regarding their specific circumstances before making repayment decisions.