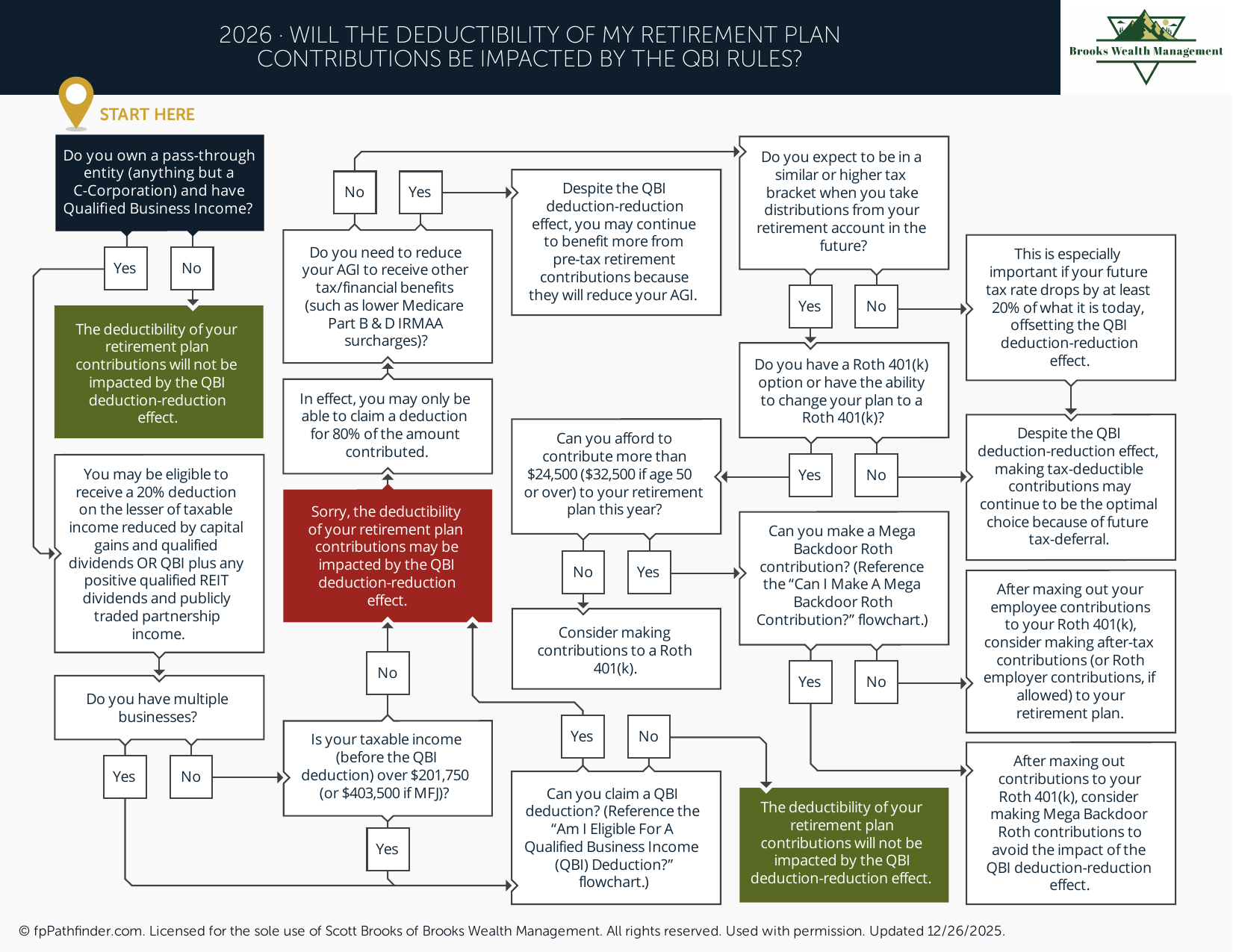

Will the Deductibility of My Retirement Plan Contributions Be Impacted by the QBI Rules?

Flowchart to determine how retirement plan contributions interact with the QBI deduction rules.

How Retirement Contributions Affect the Qualified Business Income (QBI) Deduction

The Qualified Business Income (QBI) deduction can provide a valuable tax benefit for many self-employed individuals and business owners. At the same time, retirement plan contributions often play an important role in reducing current taxable income and building long-term savings. Understanding how these two planning opportunities interact can help inform decisions regarding tax planning and retirement savings.

Because the rules surrounding the QBI deduction can be complex, it is important to understand how retirement contributions may affect qualified business income, taxable income, and overall tax outcomes. This resource provides a general overview of several key considerations.

Understanding the Qualified Business Income (QBI) Deduction

The Qualified Business Income deduction, commonly referred to as the QBI deduction or Section 199A deduction, generally allows eligible owners of pass-through businesses to deduct up to 20% of qualified business income, subject to various limitations and requirements.

The deduction may be available to sole proprietors, independent contractors, partnerships, S corporation owners, and certain trust or estate beneficiaries. Eligibility and deduction amounts can depend on multiple factors, including taxable income, business type, W-2 wages, qualified property, and other provisions contained within Internal Revenue Code Section 199A.

Because income thresholds and limitations may change periodically, business owners should review current IRS guidance and consult qualified tax professionals when evaluating potential tax strategies.

How Retirement Contributions May Affect QBI Calculations

Retirement plan contributions can affect both taxable income and qualified business income, depending on the type of retirement plan and the structure of the business. Contributions to retirement plans such as SEP IRAs, Solo 401(k)s, SIMPLE IRAs, and certain employer-sponsored retirement plans may reduce business income or adjusted gross income, which can influence the calculation of the QBI deduction.

In some situations, reducing taxable income through retirement contributions may help a taxpayer remain below income thresholds where QBI limitations become more significant. In other situations, retirement contributions may reduce the amount of qualified business income used in the QBI calculation. The overall outcome depends on the taxpayer's specific facts and circumstances.

As a result, retirement contributions should generally be evaluated within the context of a broader tax and financial planning strategy rather than focusing exclusively on maximizing a single deduction.

Retirement Savings and Tax Planning Considerations

Many business owners and self-employed individuals use retirement plans to save for long-term goals while potentially reducing current-year taxable income. Available options may include Solo 401(k)s, SEP IRAs, SIMPLE IRAs, defined benefit plans, and other retirement arrangements, depending on eligibility and business structure.

The decision between pre-tax and Roth contributions may also affect overall tax planning outcomes. Pre-tax contributions generally reduce current taxable income, while Roth contributions are typically made with after-tax dollars and may provide tax-free qualified withdrawals in retirement.

If you are evaluating retirement contribution options, you may find our guide on Roth 401(k) versus traditional retirement contributions helpful. You may also wish to review our resource on accounts to consider if you want to save more.

Balancing QBI Benefits and Retirement Contributions

For many business owners, the goal is not necessarily to maximize a single deduction but rather to optimize their overall financial picture. This may involve evaluating taxable income, retirement savings opportunities, cash flow needs, future tax expectations, and long-term financial objectives.

Because retirement contributions and the QBI deduction can affect one another, the most appropriate strategy often depends on income levels, business structure, available retirement plans, and future planning goals. In some years, maximizing retirement contributions may provide the greatest overall benefit. In other years, a different approach may be appropriate.

When Additional Guidance May Be Helpful

The interaction between retirement contributions and the QBI deduction can involve complex tax calculations and planning decisions. Business owners may benefit from coordinating with qualified tax professionals and financial advisors when evaluating available options.

Brooks Wealth Management works with professionals, business owners, retirees, and families on a wide range of financial planning topics, including retirement planning, tax-aware financial planning, and wealth management. You can learn more about our approach on our pricing page or explore additional educational materials through our free resource library.

About This Resource

This resource provides general educational information regarding the Qualified Business Income (QBI) deduction and retirement planning considerations for self-employed individuals and business owners. Every taxpayer's circumstances are different, and tax strategies should be evaluated based on individual facts, income levels, business structure, and applicable tax rules.

If you would like to discuss your situation, we invite you to schedule an introductory conversation.

Have Questions About Your Situation?

This resource is intended for educational purposes only. If you would like to discuss your circumstances, schedule an introductory conversation with Scott Brooks, CFP®.

Schedule an Introductory ConversationVentura County, California · Serving Clients Throughout California and Across the United States

Brooks Wealth Management is a Registered Investment Adviser registered with the State of California. Registration does not imply a certain level of skill or training. This content is provided for informational and educational purposes only and should not be construed as investment, tax, legal, or accounting advice. Advisory services are offered only to clients or prospective clients where Brooks Wealth Management and its representatives are properly licensed or exempt from licensure. Investing involves risk, including the potential loss of principal. CFP® is a certification mark owned by the Certified Financial Planner Board of Standards, Inc. Scott Brooks, CFP® · CRD #7227609 · Firm CRD #332237