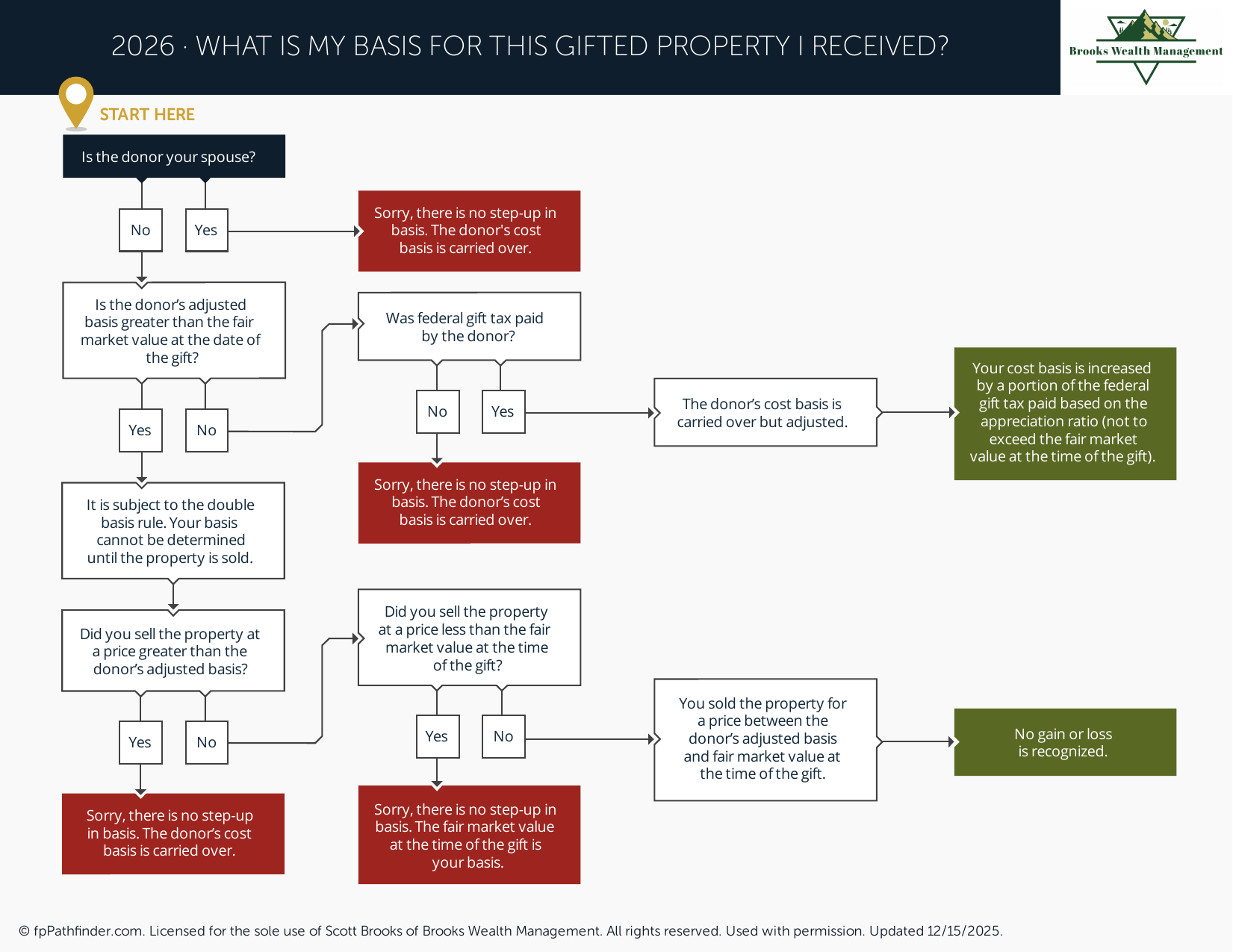

Will I Receive a Step-Up in Basis for This Gifted Property?

Flowchart to determine the cost basis rules for property received as a gift.

Do You Receive a Step-Up in Basis on Gifted Property?

One of the most common questions surrounding estate and tax planning is whether gifted property receives a step-up in basis. While many inherited assets receive favorable tax treatment at death, the rules for gifted property are often different. Understanding these distinctions can help individuals make more informed decisions regarding gifting strategies, estate planning, and future capital gains taxes.

This resource provides a general overview of how basis is typically determined for gifted and inherited property. Because tax rules can be complex and circumstances vary, individuals should consult qualified tax and legal professionals regarding their specific situation.

Understanding Cost Basis

Cost basis generally represents the amount used to determine gain or loss when an asset is sold. In many cases, basis begins with the original purchase price and may be adjusted over time for improvements, depreciation, reinvested dividends, or other factors.

When property changes ownership through a gift or inheritance, special tax rules often determine how basis is transferred to the new owner. Those rules can significantly affect future capital gains taxes when the property is eventually sold.

How Basis Works for Inherited Property

Assets inherited from a decedent often receive a basis adjustment to their fair market value as of the date of death or an alternate valuation date if applicable. This adjustment is commonly referred to as a "step-up in basis," although basis may also step down if the asset has declined in value.

Because the basis is generally adjusted to current market value, inherited assets may have little or no built-in taxable gain immediately after inheritance. This treatment is one reason estate planning considerations can play an important role in long-term tax planning.

If retirement planning and wealth transfer are part of your broader financial plan, you may also find our guide on issues to consider before retirement helpful.

How Basis Works for Gifted Property

Gifted property is generally subject to different rules. In many situations, the recipient receives the donor's adjusted basis rather than receiving a step-up in basis. This is commonly referred to as a carryover basis.

For example, if an individual purchased an asset for $100,000 and later gifted it when it was worth $500,000, the recipient may generally inherit the original $100,000 basis. If the recipient later sells the asset for $500,000, the resulting gain may be calculated using the donor's original basis rather than the asset's value on the date of the gift.

As a result, gifted assets often carry built-in capital gains that may eventually be recognized by the recipient when the property is sold.

The Double-Basis Rule for Certain Gifts

Additional rules may apply when property has declined in value before being gifted. In certain circumstances, one basis may be used for determining gains and a different basis may be used for determining losses. This treatment is commonly referred to as the double-basis rule.

These rules are intended to prevent taxpayers from transferring unrealized losses through gifts. Because the calculations can become complex, taxpayers should consult qualified tax professionals before making decisions involving depreciated assets.

When Does a Step-Up in Basis Apply?

In general, a step-up in basis is more commonly associated with assets included in a decedent's taxable estate rather than assets transferred through lifetime gifts. Whether a basis adjustment applies depends on the specific facts and circumstances, applicable tax laws, and how the property is transferred.

As a result, gifting highly appreciated assets during life may produce different tax outcomes than retaining those assets and transferring them at death. The appropriate strategy depends on a variety of factors, including estate planning objectives, tax considerations, liquidity needs, and family circumstances.

For additional estate planning education, you may find our estate planning checklist helpful.

Planning Considerations for Gifting Appreciated Assets

When evaluating gifting strategies, it may be beneficial to consider both gift tax and income tax consequences. While gifting can be an effective estate planning tool in certain situations, the potential impact on basis should also be reviewed.

Individuals often evaluate gifting decisions within the context of broader financial planning goals, including retirement planning, charitable giving, wealth transfer, and tax management. Understanding how basis transfers may affect future capital gains taxes can help support more informed decision-making.

For related planning topics, you may also find our resources on debt management and mortgage refinancing useful as part of a broader financial planning process.

When Professional Guidance May Be Helpful

Gift tax rules, basis calculations, estate planning considerations, and capital gains taxes can all interact in complex ways. Individuals considering significant gifts or transfers of appreciated assets may benefit from coordinating with qualified tax professionals, attorneys, and financial advisors.

Brooks Wealth Management works with professionals, business owners, retirees, and families on a wide range of financial planning topics, including estate planning coordination, tax-aware financial planning, and wealth management. You can learn more about our approach on our pricing page or explore additional educational materials through our free resource library.

About This Resource

This resource provides general educational information regarding gifted property, inherited assets, cost basis rules, and related tax planning concepts. Every individual's circumstances are different, and tax strategies should be evaluated based on applicable laws and personal circumstances.

If you would like to discuss your situation, we invite you to schedule an introductory conversation.

Have Questions About Your Situation?

This resource is intended for educational purposes only. If you would like to discuss your circumstances, schedule an introductory conversation with Scott Brooks, CFP®.

Schedule an Introductory ConversationVentura County, California · Serving Clients Throughout California and Across the United States

Brooks Wealth Management is a Registered Investment Adviser registered with the State of California. Registration does not imply a certain level of skill or training. This content is provided for informational and educational purposes only and should not be construed as investment, tax, legal, or accounting advice. Advisory services are offered only to clients or prospective clients where Brooks Wealth Management and its representatives are properly licensed or exempt from licensure. Investing involves risk, including the potential loss of principal. CFP® is a certification mark owned by the Certified Financial Planner Board of Standards, Inc. Scott Brooks, CFP® · CRD #7227609 · Firm CRD #332237