Will I Have to Pay Tax on the Sale of My Investment?

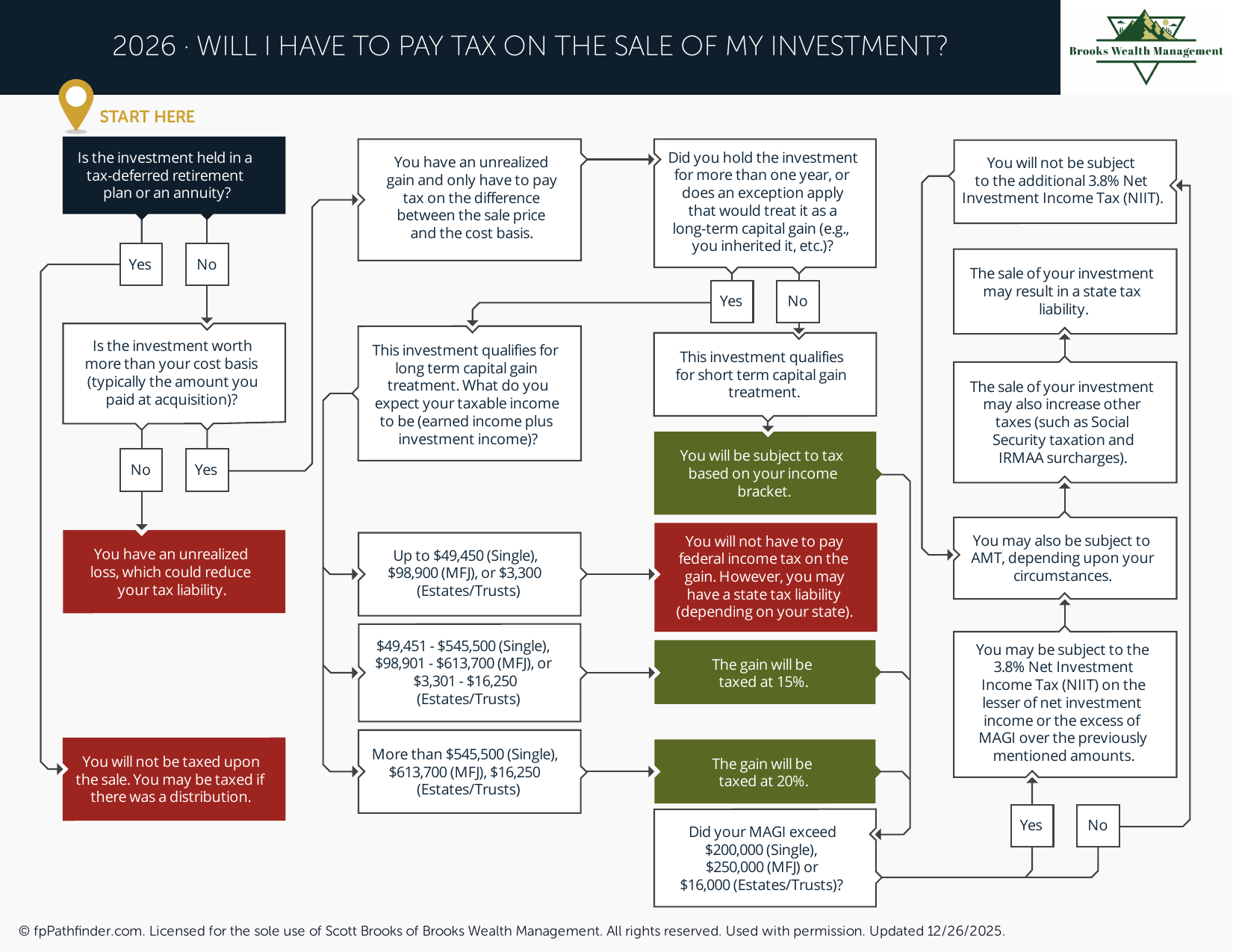

Flowchart to determine the tax treatment of investment sales including capital gains rates and exclusions.

Will I Have to Pay Tax on the Sale of My Investment?

In many cases, selling an investment may result in a taxable gain or loss. The amount of tax owed, if any, depends on several factors, including the type of investment, your cost basis, how long the investment was held, your taxable income, and whether the asset is held inside a taxable or tax-advantaged account.

Understanding how investment gains are taxed can help investors make more informed decisions and better evaluate the potential after-tax impact of selling an asset.

How Capital Gains Are Calculated

When an investment is sold, the gain or loss is generally determined by comparing the sale proceeds to the investment's adjusted cost basis. Cost basis is often the original purchase price, adjusted for factors such as reinvested dividends, commissions, corporate actions, or prior adjustments.

If the sale price exceeds the adjusted basis, a capital gain may result. If the sale price is less than the adjusted basis, a capital loss may occur. The tax treatment of the gain or loss depends on several additional factors, including the holding period.

Short-Term vs. Long-Term Capital Gains

The length of time an investment is held generally affects how gains are taxed.

- Short-term capital gains generally apply to investments held for one year or less. These gains are typically taxed at ordinary income tax rates.

- Long-term capital gains generally apply to investments held for more than one year. Long-term gains may qualify for preferential federal tax rates depending on taxable income and other factors.

Because tax rates and thresholds can change over time, investors should review current IRS guidance and consult qualified tax professionals when evaluating potential tax consequences.

Factors That May Affect Investment Sale Taxes

Several variables can influence the tax impact of selling an investment. These may include the investor's taxable income, filing status, state of residence, holding period, available capital losses, and whether the investment is held within a taxable account or a tax-advantaged retirement account.

Investors may also be subject to additional taxes under certain circumstances. For example, some higher-income taxpayers may be subject to the Net Investment Income Tax (NIIT), which can apply to certain investment income, including capital gains.

If you are evaluating broader tax planning opportunities, you may find our guide on Roth conversions helpful.

Using Capital Losses to Offset Gains

Capital losses may be used to offset capital gains, subject to applicable tax rules. If losses exceed gains during a tax year, a limited amount of excess losses may generally be used to offset ordinary income, with remaining losses potentially carried forward to future years.

This concept is commonly referred to as tax-loss harvesting when implemented as part of an overall investment strategy. Whether tax-loss harvesting is appropriate depends on an individual's investment objectives, tax situation, and long-term financial plan.

Tax-Advantaged Accounts and Investment Sales

The tax treatment of investment sales may differ depending on the type of account in which the investment is held. Investments held within retirement accounts such as traditional IRAs, Roth IRAs, 401(k) plans, and other tax-advantaged accounts are often subject to different tax rules than investments held in taxable brokerage accounts.

Understanding how different account types work together may help investors evaluate where assets are held and how future withdrawals may be taxed. For additional information, see our guide on accounts to consider if you want to save more.

Special Considerations for Business Owners and Equity Compensation

Some investors may hold concentrated positions through employer stock, stock options, restricted stock units (RSUs), deferred compensation arrangements, or ownership interests in closely held businesses. These assets can involve additional tax considerations that may differ from traditional investment accounts.

Business sales, equity compensation strategies, and concentrated stock positions often require separate analysis because the tax consequences can vary significantly depending on the structure of the transaction and the type of asset involved.

Investment Sales Within a Financial Plan

The decision to sell an investment should generally be evaluated within the context of an overall financial plan rather than based solely on taxes. Investment objectives, diversification, liquidity needs, risk management, retirement planning, charitable goals, and estate planning considerations may all influence whether selling an investment is appropriate.

While taxes are an important consideration, avoiding taxes alone may not always support broader financial goals. Reviewing investment decisions within the context of a comprehensive financial plan can help align actions with long-term objectives.

For additional educational content, visit our free resource library.

About This Resource

This resource provides general educational information regarding investment sales, capital gains, capital losses, and related tax concepts. Every investor's circumstances are different, and tax consequences should be evaluated based on individual facts, applicable laws, and personal financial goals.

Brooks Wealth Management works with professionals, business owners, retirees, and families on a wide range of financial planning topics, including tax-aware financial planning and wealth management. If you would like to discuss your situation, we invite you to schedule an introductory conversation or learn more about our approach on our pricing page.

Have Questions About Your Situation?

This resource is intended for educational purposes only. If you would like to discuss your circumstances, schedule an introductory conversation with Scott Brooks, CFP®.

Schedule an Introductory ConversationVentura County, California · Serving Clients Throughout California and Across the United States

Brooks Wealth Management is a Registered Investment Adviser registered with the State of California. Registration does not imply a certain level of skill or training. This content is provided for informational and educational purposes only and should not be construed as investment, tax, legal, or accounting advice. Advisory services are offered only to clients or prospective clients where Brooks Wealth Management and its representatives are properly licensed or exempt from licensure. Investing involves risk, including the potential loss of principal. CFP® is a certification mark owned by the Certified Financial Planner Board of Standards, Inc. Scott Brooks, CFP® · CRD #7227609 · Firm CRD #332237