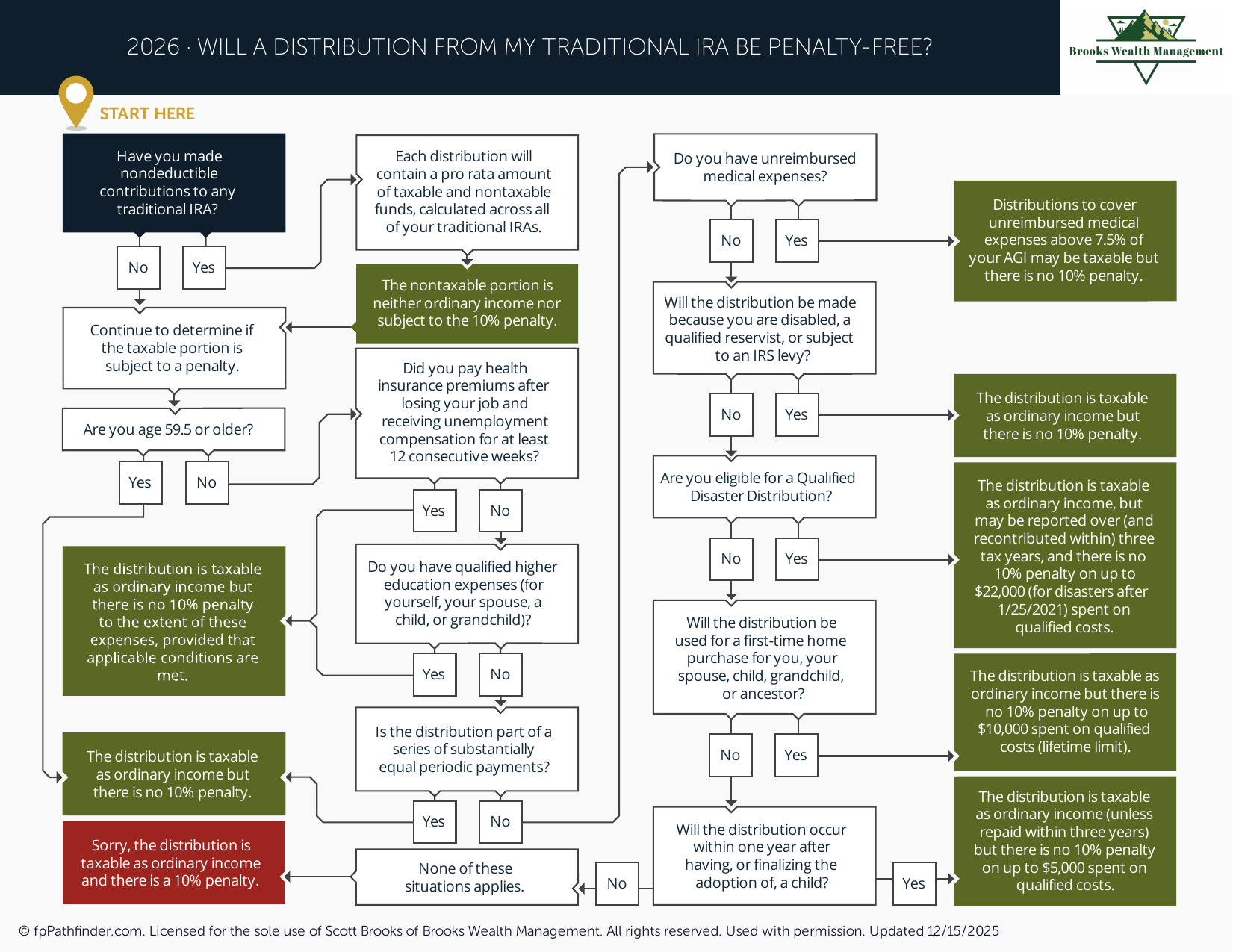

Will a Distribution from My Traditional IRA Be Penalty-Free?

Flowchart to determine whether a traditional IRA distribution avoids the 10% penalty.

Can I Take an IRA Withdrawal Without Paying the 10% Early Withdrawal Penalty?

In general, withdrawals from a Traditional IRA before age 59½ may be subject to a 10% early withdrawal penalty in addition to ordinary income taxes. However, the IRS provides several exceptions that may allow individuals to take an IRA distribution without incurring the penalty.

Whether an IRA withdrawal qualifies for an exception depends on the purpose of the distribution, the account owner's circumstances, and applicable IRS rules. Understanding these exceptions is often an important part of retirement and cash flow planning.

Review the General Early Withdrawal Rules

Traditional IRAs are designed primarily for retirement savings. As a result, distributions taken before age 59½ are generally subject to both ordinary income tax and an additional 10% early withdrawal penalty.

Common considerations include:

- Your age at the time of the distribution.

- The type of IRA involved.

- The purpose of the withdrawal.

- The amount withdrawn.

- The potential tax consequences of the distribution.

While many individuals focus on avoiding the penalty, it is also important to understand how an IRA distribution may affect taxable income for the year.

Review Medical Expense Exceptions

Certain medical expenses may qualify for an exception to the 10% early withdrawal penalty.

Individuals often review whether IRA distributions are being used for:

- Unreimbursed medical expenses.

- Qualified medical costs exceeding applicable IRS thresholds.

- Health-related expenses during periods of financial hardship.

Eligibility depends on individual circumstances and the specific requirements outlined by the IRS.

Review Health Insurance Premium Exceptions

Individuals who experience a period of unemployment may qualify for penalty-free IRA distributions used to pay health insurance premiums.

Common considerations include:

- Length of unemployment.

- Receipt of unemployment compensation.

- Timing of the distribution.

- Use of funds for qualified health insurance costs.

Because specific eligibility requirements apply, individuals often review the details carefully before taking a distribution.

Review Higher Education Expense Exceptions

IRA withdrawals may qualify for an exception when used for certain qualified higher education expenses.

Common expenses individuals review include:

- Tuition.

- Required fees.

- Books and supplies.

- Required equipment.

- Certain room and board expenses for eligible students.

The rules may apply to expenses incurred for the account owner, spouse, children, or grandchildren, subject to applicable requirements.

Review First-Time Home Purchase Exceptions

The IRS provides a limited exception for certain first-time home purchase expenses.

Common considerations include:

- Whether the homebuyer meets the applicable first-time homebuyer definition.

- The amount of the planned distribution.

- Timing of the purchase.

- Documentation requirements.

Individuals often review this exception when evaluating funding sources for a home purchase.

Review Disability and Death Exceptions

Certain distributions may qualify for penalty-free treatment when the account owner becomes disabled or when distributions occur following the account owner's death.

Common considerations include:

- Applicable disability requirements.

- Beneficiary distribution rules.

- Inherited IRA requirements.

- Distribution timing considerations.

These situations often involve additional retirement, estate, and tax planning considerations.

Review Substantially Equal Periodic Payments (SEPP)

Some individuals review a strategy commonly referred to as substantially equal periodic payments, or SEPP, under Internal Revenue Code Section 72(t).

This approach generally involves taking a series of scheduled distributions over a required period.

Common considerations include:

- Calculation methods.

- Distribution schedules.

- Required commitment periods.

- Potential consequences of modifying payments.

- Long-term retirement planning implications.

Because these arrangements can be complex, individuals often review them carefully before implementation.

Review the Tax Consequences of an IRA Distribution

Even when a distribution qualifies for an exception to the 10% early withdrawal penalty, ordinary income taxes may still apply.

Common considerations include:

- The amount of taxable income generated.

- Current tax bracket considerations.

- Potential effects on deductions and credits.

- State income tax implications.

- The impact on future tax planning opportunities.

Individuals often evaluate both the penalty and income tax consequences before withdrawing retirement assets.

Review Alternative Sources of Funds

Before taking an IRA distribution, many individuals review whether other resources may be available.

Common considerations include:

- Emergency savings.

- Taxable investment accounts.

- Cash reserves.

- Employer-sponsored retirement plan options.

- Available borrowing alternatives.

Because IRA withdrawals permanently reduce retirement assets, reviewing alternative funding sources may be an important part of the decision-making process.

Individuals evaluating broader savings strategies may also find it helpful to review what accounts to consider when saving more.

Review How an IRA Distribution Fits Within Your Financial Plan

An IRA withdrawal may affect retirement readiness, future tax obligations, investment strategy, and long-term financial goals.

Common questions individuals review include:

- Is the withdrawal necessary to meet current financial needs?

- How will the distribution affect retirement projections?

- Are there other available sources of liquidity?

- Will the distribution create unexpected tax consequences?

- Does the withdrawal align with broader financial planning objectives?

Because retirement accounts often represent a significant portion of long-term savings, distribution decisions are frequently evaluated within the context of a broader financial plan.

Additional retirement planning considerations can be found in our guide discussing issues to consider before retirement.

About This Resource

This resource provides general educational information regarding IRA withdrawals, early withdrawal penalties, and IRS penalty exceptions. The rules governing IRA distributions can be complex and may vary depending on the type of IRA, the purpose of the withdrawal, and individual circumstances.

Individuals often review penalty-free withdrawal provisions when evaluating healthcare expenses, education costs, home purchases, retirement transitions, disability situations, and broader cash flow planning needs. Understanding both the penalty rules and potential income tax consequences is an important part of making informed retirement account decisions.

This resource is intended to provide a framework for understanding common IRA withdrawal considerations. It is not intended as investment, tax, legal, insurance, healthcare, cybersecurity, or financial advice. Individual circumstances vary, and tax rules may change over time.

If you would like to discuss how this topic fits into your broader financial plan, we invite you to schedule an introductory conversation.