What Issues Should I Consider When Reviewing My Existing Annuity?

Checklist for evaluating whether to keep, exchange, or surrender an existing annuity contract.

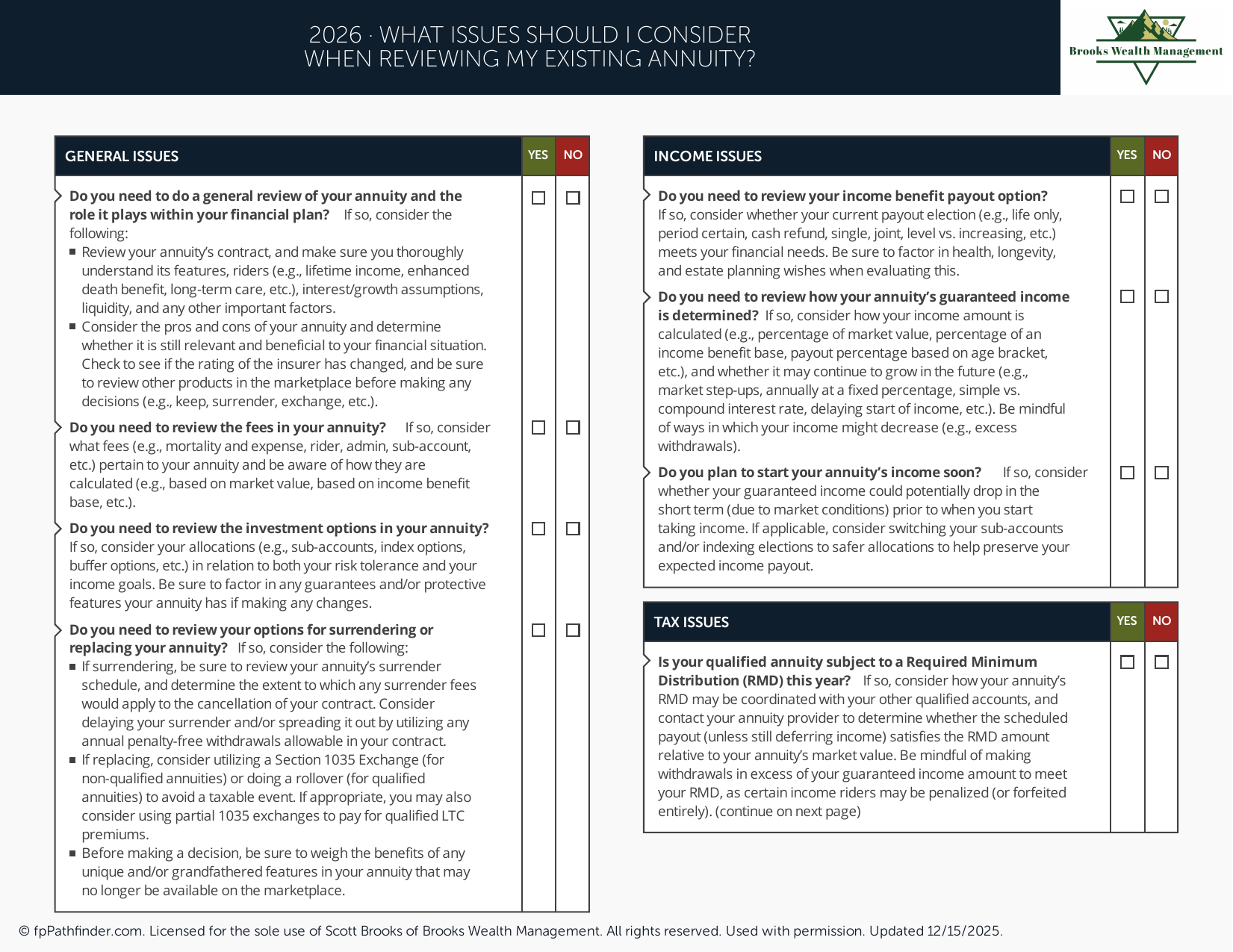

Should I Review My Existing Annuity?

Annuities are often purchased to help address retirement income needs, tax deferral, principal protection, or other long-term financial objectives. Because financial goals, contract features, and personal circumstances may change over time, many individuals periodically review existing annuity contracts as part of their overall financial plan.

If you currently own an annuity, there are several issues that may be appropriate to review before making decisions regarding the contract.

Review Why the Annuity Was Originally Purchased

Annuities can serve different purposes depending on the type of contract and the objectives of the owner.

Individuals often review:

- Whether the annuity was purchased for retirement income

- Whether the annuity was intended for tax-deferred growth

- Whether principal protection was a primary objective

- Whether the contract was purchased for estate or legacy planning purposes

- Whether the original goals remain consistent with current financial objectives

Understanding the original purpose of the annuity may help provide context when evaluating current contract features and benefits.

Review Contract Features and Benefits

Annuity contracts may contain a variety of features that affect how the contract operates over time.

Common items reviewed include:

- Guaranteed income provisions

- Death benefit provisions

- Living benefit riders

- Withdrawal provisions

- Interest crediting methods

- Investment options within the contract

Contract terms vary significantly among annuity providers, making it important to understand the specific provisions applicable to a particular contract.

Review Fees, Expenses, and Surrender Charges

Some annuity contracts may include fees, expenses, or surrender charge schedules that affect future flexibility.

Individuals often review:

- Mortality and expense charges

- Administrative fees

- Underlying investment expenses

- Optional rider costs

- Remaining surrender charge periods

- Withdrawal limitations

Understanding these provisions may help individuals evaluate how the annuity fits within their broader financial strategy.

Review Tax Considerations

Annuities generally provide tax-deferred growth, which means earnings are not taxed until withdrawn.

Individuals often review:

- Potential tax treatment of future withdrawals

- Early withdrawal penalties before age 59½

- Required Minimum Distribution considerations when applicable

- Beneficiary tax implications

- Potential use of Section 1035 exchanges

Tax consequences vary based on the type of annuity, ownership structure, and individual circumstances.

For additional information, review our resources on Roth conversions and retirement withdrawal strategies.

Review How the Annuity Fits Within Your Overall Financial Plan

Annuities are often one component of a broader retirement and investment strategy.

Individuals commonly review:

- Retirement income needs

- Liquidity requirements

- Investment account balances

- Risk tolerance

- Estate planning objectives

- Tax planning considerations

Periodic reviews may help determine whether an annuity continues to align with current financial goals and planning priorities.

For additional educational resources, visit our free resources. You may also find our guide on retirement planning considerations helpful.

About This Resource

This resource provides general educational information regarding annuities and annuity contract reviews. It is not intended as investment, tax, insurance, legal, or financial advice. Contract provisions, fees, benefits, and tax treatment vary by provider and individual circumstances.

If you would like to discuss how an existing annuity fits within your broader financial plan, we invite you to schedule an introductory conversation.