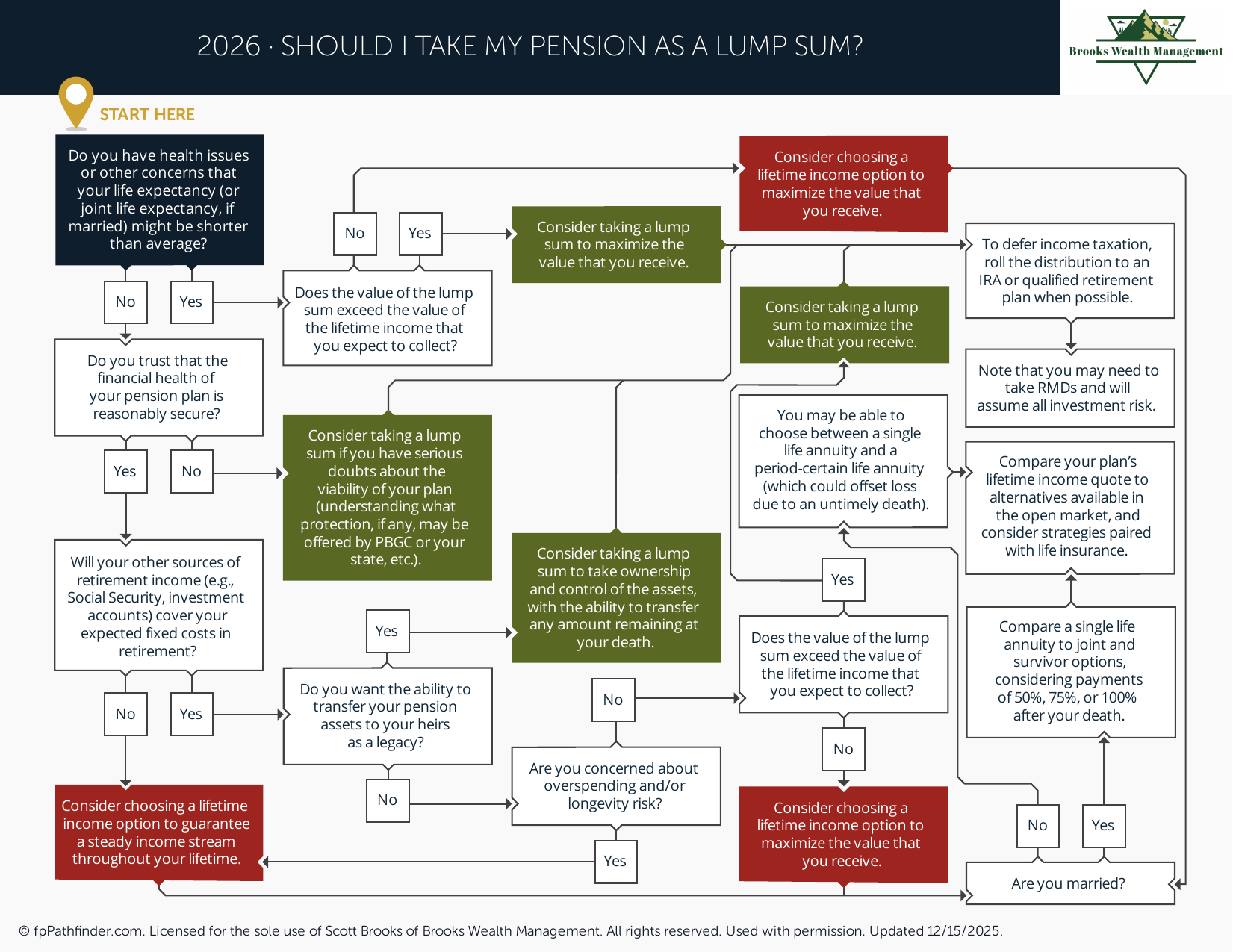

Should I Take My Pension as a Lump Sum?

Decision flowchart to evaluate lump-sum vs. annuity pension payout options.

Should I Take My Pension as a Lump Sum?

When retiring from a pension plan, individuals are often faced with an important decision: receive a lifetime stream of income through pension payments or elect a pension lump sum. The right choice depends on personal circumstances, retirement income needs, tax considerations, longevity expectations, and overall financial planning goals.

Because pension elections are often irreversible, many individuals review both options carefully before making a final decision. Evaluating how a pension fits within a broader retirement plan can help clarify the potential benefits and tradeoffs of each approach.

Review How a Pension Lump Sum Works

A pension lump sum is generally a one-time payment representing the present value of future pension benefits. Instead of receiving monthly payments from the pension plan, the participant receives a single distribution that may be rolled into an IRA or other eligible retirement account.

Common considerations include:

- The amount of the lump sum offer.

- The monthly pension payment available.

- Interest rates used in the calculation.

- Life expectancy assumptions.

- Available survivor benefit options.

Individuals often request pension illustrations showing multiple payout options before evaluating a final decision.

Review Guaranteed Income Considerations

One of the primary advantages of a traditional pension is the ability to receive guaranteed income for life.

Common questions individuals review include:

- How much monthly income will the pension provide?

- Will income continue for a spouse after death?

- How much of retirement spending will be covered by guaranteed sources?

- What other income sources exist, such as Social Security or annuities?

- How important is income certainty during retirement?

For some retirees, maintaining a predictable monthly income stream may be an important part of retirement planning.

Review Investment Control and Flexibility

A pension lump sum generally provides greater control over retirement assets.

Common considerations include:

- Investment flexibility.

- Control over withdrawals.

- Ability to adjust investment strategy over time.

- Access to a broader range of investment options.

- Potential coordination with existing retirement accounts.

Individuals who prefer greater control over their retirement assets often review whether a lump sum aligns with their investment preferences and long-term objectives.

Review Longevity Considerations

Life expectancy is often a significant factor when evaluating pension options.

Common considerations include:

- Personal health history.

- Family longevity trends.

- Current age.

- Expected retirement spending needs.

- Potential healthcare costs later in life.

Individuals who expect a longer retirement may evaluate guaranteed lifetime income differently than those with shorter planning horizons.

Review Tax Implications

The tax treatment of a pension lump sum often depends on how the distribution is handled.

Common considerations include:

- Whether the lump sum will be rolled into an IRA.

- Potential taxation if funds are distributed directly.

- Future required minimum distribution considerations.

- Long-term retirement income tax planning.

- Potential Roth conversion opportunities after rollover.

Many individuals review distribution options carefully to avoid unintended tax consequences.

Additional information is available in our resource discussing Roth conversion considerations.

Review Survivor and Estate Planning Considerations

The treatment of pension benefits after death may vary significantly between a lump sum election and a lifetime income option.

Common questions individuals review include:

- Will benefits continue for a surviving spouse?

- Can remaining assets pass to heirs?

- How does each option affect estate planning goals?

- What beneficiary options are available?

- How important is leaving assets to future generations?

A pension lump sum may provide more flexibility for wealth transfer planning, while certain pension options may prioritize lifetime income protection.

Review Inflation and Purchasing Power Risks

Many pensions provide fixed monthly payments that may not increase over time.

Common considerations include:

- Expected inflation rates.

- Whether cost-of-living adjustments are available.

- Future purchasing power concerns.

- Expected retirement spending patterns.

- Long-term healthcare and living expenses.

Individuals often review how inflation may affect future retirement income needs when comparing pension alternatives.

Review Overall Retirement Income Planning

A pension decision should generally be evaluated within the context of an overall retirement income plan.

Common considerations include:

- Social Security benefits.

- IRA and 401(k) balances.

- Taxable investment accounts.

- Other pension income.

- Expected retirement spending needs.

Because pensions represent only one component of retirement income, many individuals review how the decision affects their broader retirement strategy.

Additional retirement planning considerations can be found in our guide discussing issues to consider before retirement.

Review Questions to Ask Before Making a Pension Election

Before making a final pension decision, individuals often review the following questions:

- How much guaranteed income do I need during retirement?

- What other retirement income sources are available?

- Am I comfortable managing investments?

- How important is leaving assets to heirs?

- How does each option affect my tax situation?

- How does each option affect my spouse or beneficiaries?

- Does one option provide greater flexibility for future planning?

These questions can help frame the analysis before selecting either a pension lump sum or a lifetime income option.

About This Resource

This resource provides general educational information regarding pension lump sums, pension income options, retirement planning considerations, and related tax and estate planning issues. Pension elections can have long-term financial implications and are often influenced by factors such as retirement income needs, longevity expectations, investment preferences, tax considerations, and beneficiary objectives.

Individuals often review pension decisions alongside Social Security planning, retirement income projections, investment strategies, estate planning goals, and broader financial planning considerations. Because pension elections are frequently irreversible, careful evaluation of available options may be appropriate before making a final decision.

This resource is intended to provide a framework for understanding common pension planning considerations. It is not intended as investment, tax, legal, insurance, healthcare, cybersecurity, or financial advice. Individual circumstances vary, and applicable rules may change over time.

If you would like to discuss how this topic fits into your broader financial plan, we invite you to schedule an introductory conversation.