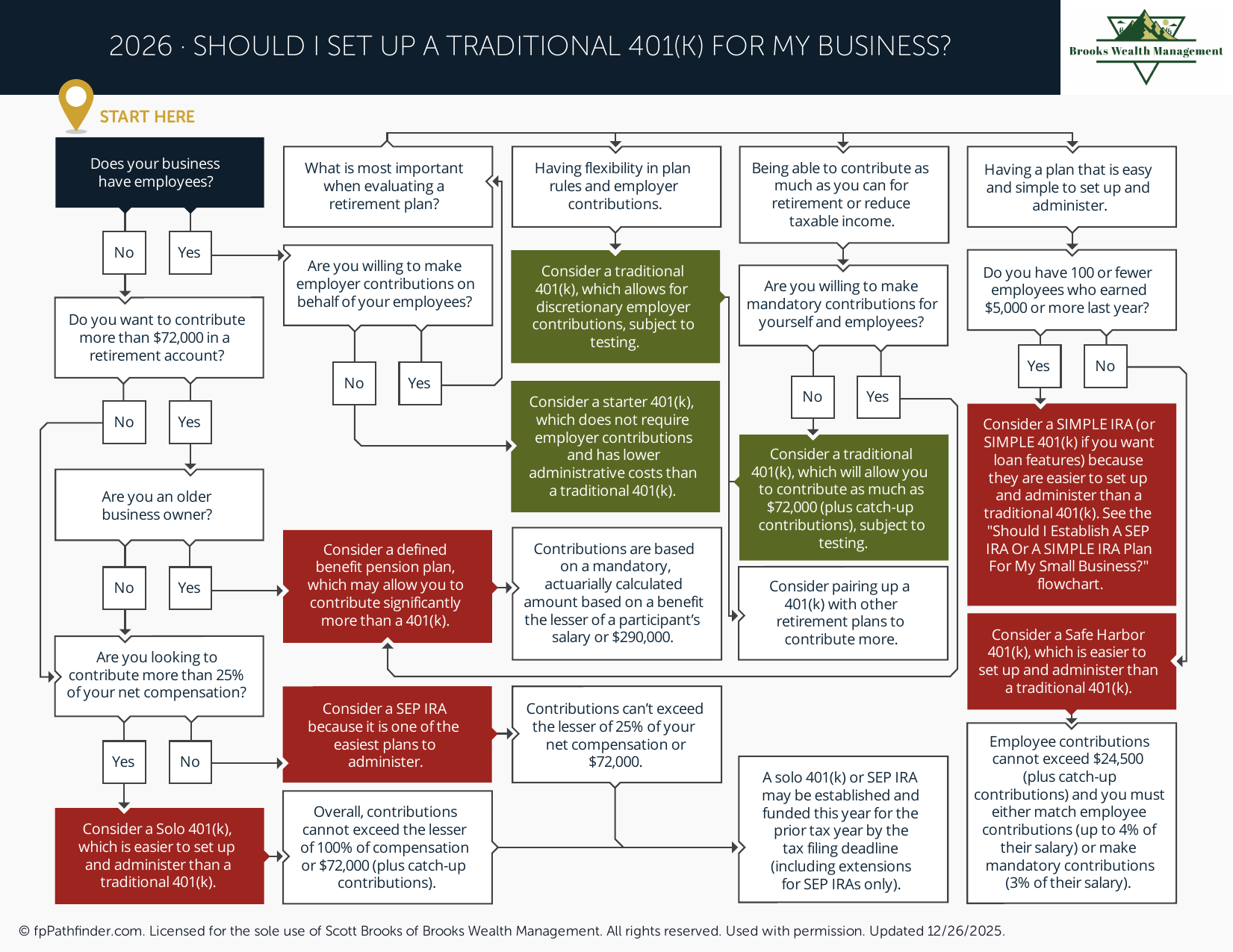

Should I Set Up a Traditional 401(k) for My Business?

Decision flowchart to evaluate whether a traditional 401(k) is right for your business.

Should I Set Up a Traditional 401(k) for My Business?

A Traditional 401(k) plan is one of the most commonly used employer-sponsored retirement plans available to business owners. It allows employees to make salary deferral contributions while providing employers with flexibility in plan design, contribution structures, and retirement benefits.

Whether a Traditional 401(k) is appropriate for a business depends on factors such as company size, employee demographics, business profitability, retirement objectives, administrative capacity, and long-term benefits strategy.

Review How a Traditional 401(k) Works

A Traditional 401(k) allows eligible employees to contribute a portion of their compensation into a retirement account through payroll deductions. Contributions are generally made on a pre-tax basis, and investment earnings grow tax-deferred until withdrawn.

Common plan features may include:

- Employee salary deferrals.

- Employer matching contributions.

- Employer profit-sharing contributions.

- Participant-directed investments.

- Roth contribution options if offered by the plan.

Business owners often review how these features align with company goals before establishing a retirement plan.

Review Business Owner Retirement Savings Opportunities

One reason many business owners consider a Traditional 401(k) is the ability to save for retirement while also providing benefits to employees.

Common considerations include:

- Annual contribution limits.

- Employer contribution flexibility.

- Catch-up contribution opportunities.

- Coordination with other retirement accounts.

- Long-term retirement planning goals.

Business owners often compare available contribution limits across different retirement plan types when evaluating retirement plan options.

Review Employee Recruitment and Retention Considerations

Retirement benefits are frequently included as part of a broader employee compensation package.

Common questions business owners review include:

- Will a retirement plan improve employee retention?

- Will a retirement plan enhance recruiting efforts?

- What retirement benefits are common within the industry?

- How important are retirement benefits to current employees?

- Should employer contributions be included in the plan design?

Many employers view retirement plans as one component of a broader benefits strategy designed to support workforce stability and employee engagement.

Review Employer Contribution Options

Traditional 401(k) plans generally allow several approaches to employer contributions.

Common options may include:

- Matching contributions.

- Profit-sharing contributions.

- Safe harbor contributions.

- Discretionary employer contributions.

- Combination contribution structures.

The appropriate contribution approach often depends on business cash flow, profitability, workforce demographics, and retirement plan objectives.

Review Tax Considerations

Traditional 401(k) plans may provide tax-related benefits for both employers and employees.

Common considerations include:

- Employer deduction opportunities.

- Tax-deferred employee contributions.

- Tax-deferred investment growth.

- Retirement income tax planning.

- Potential tax credits available to eligible businesses establishing new plans.

Because tax treatment varies based on individual and business circumstances, many business owners review retirement plan decisions alongside broader tax planning objectives.

Review Administrative Responsibilities

Establishing a Traditional 401(k) also creates administrative and compliance responsibilities.

Common considerations include:

- Plan administration requirements.

- Annual reporting obligations.

- Participant communication requirements.

- Plan document maintenance.

- Fiduciary responsibilities.

Business owners often evaluate whether internal resources or outside service providers will be used to support plan administration.

Review Nondiscrimination and Compliance Requirements

Many Traditional 401(k) plans are subject to annual compliance testing designed to ensure retirement plan benefits are not disproportionately concentrated among highly compensated employees.

Common considerations include:

- Employee participation rates.

- Highly compensated employee classifications.

- Annual testing requirements.

- Corrective contribution procedures.

- Safe harbor plan alternatives.

Understanding these requirements may help business owners evaluate whether a Traditional 401(k) structure aligns with their workforce and business objectives.

Review Alternative Retirement Plan Options

Before establishing a Traditional 401(k), many business owners compare it against other retirement plan options.

Common alternatives may include:

- SEP IRAs.

- SIMPLE IRAs.

- Safe Harbor 401(k) plans.

- Solo 401(k) plans.

- Cash balance and defined benefit plans.

Each option has different contribution limits, administrative requirements, costs, and planning considerations.

Individuals interested in broader retirement savings strategies may also find it helpful to review what accounts to consider when saving more.

Review Traditional vs. Roth 401(k) Features

Many employer-sponsored plans allow both Traditional and Roth employee contributions.

Common considerations include:

- Current versus future tax expectations.

- Retirement income planning goals.

- Employee preferences.

- Tax diversification objectives.

- Long-term retirement planning considerations.

Additional information is available in our resource discussing Roth 401(k) contribution considerations.

Review Whether a Traditional 401(k) Fits Your Business Goals

The decision to establish a Traditional 401(k) often extends beyond retirement savings alone.

Common questions business owners review include:

- How important are retirement benefits to the company's overall compensation strategy?

- What level of employer contributions is sustainable?

- How much administrative complexity is acceptable?

- What retirement savings opportunities are desired for owners and employees?

- How does the plan fit within broader business objectives?

Because retirement plans can affect business operations, employee benefits, tax planning, and owner retirement goals, many business owners evaluate these factors together before selecting a plan design.

About This Resource

This resource provides general educational information regarding Traditional 401(k) plans, employer-sponsored retirement plans, business retirement benefits, and related planning considerations. Traditional 401(k) plans can provide retirement savings opportunities for both business owners and employees while introducing administrative, compliance, and fiduciary responsibilities.

Business owners often review retirement plan options when evaluating employee benefits, tax planning opportunities, owner retirement savings goals, workforce retention strategies, and long-term business objectives. The appropriate retirement plan structure depends on company size, employee demographics, profitability, and overall financial planning considerations.

This resource is intended to provide a framework for understanding common Traditional 401(k) planning considerations. It is not intended as investment, tax, legal, insurance, healthcare, cybersecurity, or financial advice. Individual circumstances vary, and applicable rules may change over time.

If you would like to discuss how this topic fits into your broader financial plan, we invite you to schedule an introductory conversation.