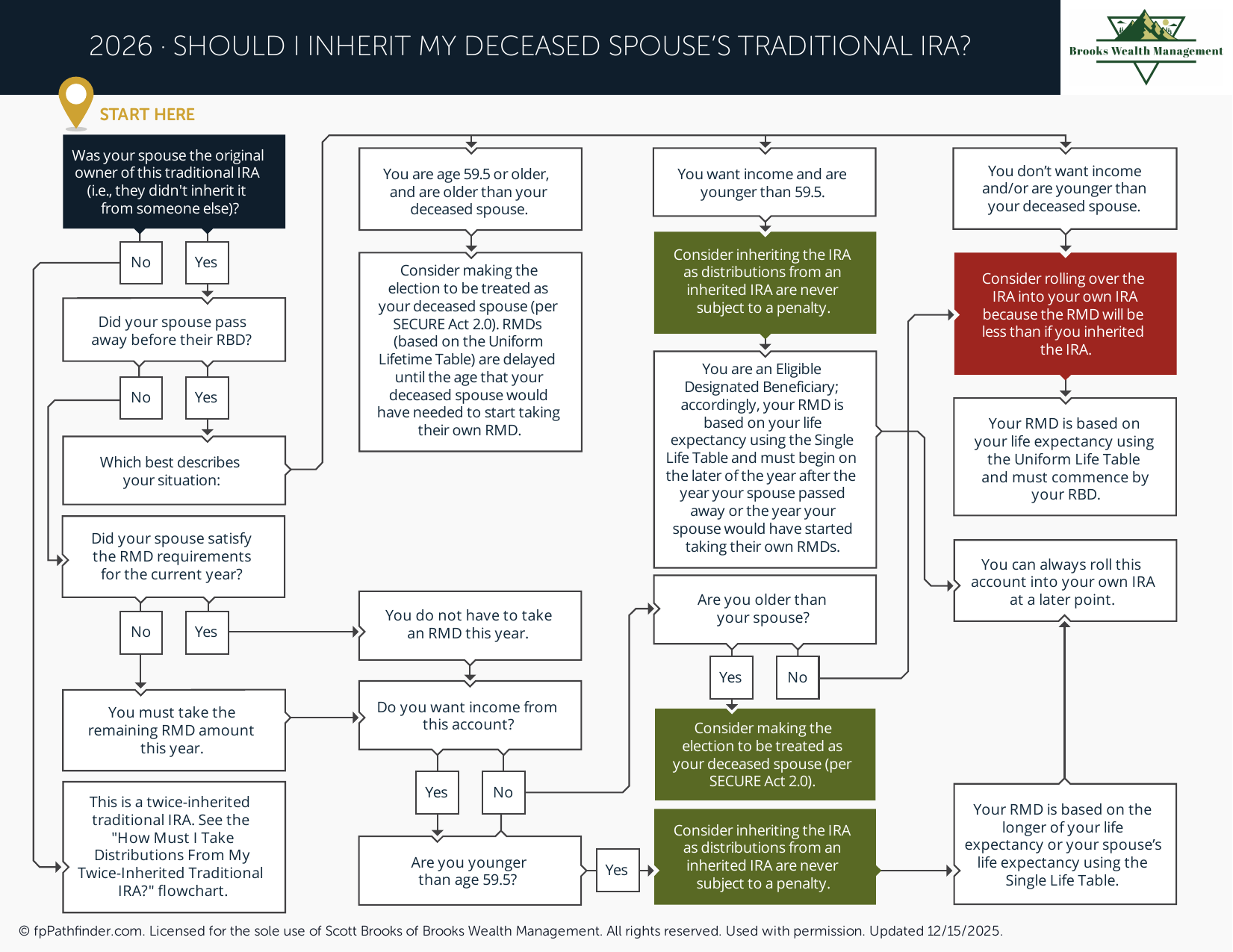

Should I Inherit My Deceased Spouse's Traditional IRA?

Decision flowchart for spousal IRA inheritance options and tax implications.

What Should I Consider If I Inherit a Traditional IRA From My Spouse?

When a spouse inherits a Traditional IRA, several options may be available depending on age, financial circumstances, retirement goals, and income needs. The decisions made after inheriting a retirement account can affect future required minimum distributions, tax planning opportunities, retirement income flexibility, and long-term wealth transfer objectives.

Because surviving spouses generally receive more favorable treatment under IRS rules than other beneficiaries, individuals often review all available options before deciding how to handle an inherited Traditional IRA.

Review Your Available Options as a Surviving Spouse

A surviving spouse generally has several choices when inheriting a Traditional IRA.

Common options may include:

- Rolling the assets into their own IRA.

- Treating the account as their own IRA.

- Maintaining the account as an inherited IRA.

- Taking distributions from the account.

Each option may affect future taxes, required minimum distributions, withdrawal flexibility, and retirement planning considerations.

Review a Spousal IRA Rollover

A spousal rollover generally allows the inherited Traditional IRA to be moved into the surviving spouse's own IRA.

Common considerations include:

- Future required minimum distribution timing.

- Long-term tax deferral opportunities.

- Retirement income planning flexibility.

- Beneficiary designation options.

- Coordination with existing retirement accounts.

Individuals often review whether consolidating retirement assets into a personal IRA aligns with their broader retirement planning objectives.

Review Maintaining the Account as an Inherited IRA

Some surviving spouses choose to maintain the account as an inherited IRA rather than completing a rollover.

Common considerations include:

- Current age.

- Expected need for withdrawals.

- Early retirement considerations.

- Penalty rules for distributions.

- Required minimum distribution requirements.

Maintaining inherited IRA status may provide flexibility in certain situations, particularly when retirement assets may be needed before age 59½.

Review Required Minimum Distribution Rules

Required minimum distribution rules are often one of the most important factors when evaluating inherited IRA options.

Common questions individuals review include:

- When will required minimum distributions begin?

- How are distributions calculated?

- Will annual distributions be required?

- How will future distributions affect taxable income?

- How do the rules differ between a rollover and an inherited IRA?

Because distribution requirements may vary depending on the option selected, many surviving spouses evaluate these rules carefully before making a decision.

Review Tax Planning Considerations

Distributions from a Traditional IRA are generally subject to ordinary income taxation.

Common considerations include:

- Current tax bracket.

- Future income expectations.

- Timing of withdrawals.

- Coordination with Social Security and retirement income.

- Long-term retirement tax planning objectives.

Individuals often review how inherited IRA distributions may affect future taxable income before selecting a distribution strategy.

Review Withdrawal Flexibility

Withdrawal flexibility may differ depending on whether the inherited IRA remains a beneficiary IRA or becomes the surviving spouse's own IRA.

Common considerations include:

- Current age.

- Expected cash flow needs.

- Retirement timeline.

- Potential penalty considerations.

- Emergency liquidity needs.

For some individuals, access to retirement assets may be an important factor in determining which inherited IRA option is most appropriate.

Review Roth Conversion Opportunities

Inherited retirement assets may lead some individuals to evaluate broader tax planning opportunities, including Roth conversion strategies involving their own retirement accounts.

Common considerations include:

- Current versus future tax rates.

- Projected retirement income.

- Required minimum distributions.

- Estate planning goals.

- Long-term tax diversification objectives.

Additional information is available in our guide discussing Roth conversion considerations.

Review Beneficiary and Estate Planning Considerations

After inheriting a Traditional IRA, many individuals review beneficiary designations and estate planning documents.

Common considerations include:

- Updating beneficiaries.

- Coordinating retirement accounts with estate documents.

- Future wealth transfer goals.

- Potential tax consequences for heirs.

- Long-term family planning objectives.

Reviewing beneficiary designations may help ensure inherited assets align with current wishes and planning objectives.

Review How the Inherited IRA Fits Within Your Retirement Plan

An inherited Traditional IRA may significantly affect retirement income planning, investment strategy, and long-term financial goals.

Common questions individuals review include:

- How does the inherited IRA affect retirement readiness?

- Should the assets remain invested for long-term growth?

- How do future distributions affect retirement cash flow?

- What tax planning opportunities exist?

- How does the account fit within broader financial goals?

Because inherited retirement accounts often represent a substantial financial asset, many surviving spouses evaluate these decisions within the context of a comprehensive retirement plan.

Additional retirement planning considerations can be found in our guide discussing issues to consider before retirement.

Review Questions Before Making a Decision

Before choosing how to handle an inherited Traditional IRA, individuals often review the following questions:

- Will retirement assets be needed before age 59½?

- How important is delaying required minimum distributions?

- What are the current and expected future tax implications?

- How does the inherited IRA affect retirement income planning?

- Which option provides the greatest flexibility based on current circumstances?

These questions can help frame the decision before electing a rollover or maintaining inherited IRA status.

About This Resource

This resource provides general educational information regarding Traditional IRAs inherited from a spouse, spousal rollover options, inherited IRA considerations, required minimum distributions, and related retirement planning issues. Surviving spouses generally have several options available, each of which may affect taxes, distributions, retirement planning flexibility, and long-term financial goals.

Individuals often review inherited IRA decisions alongside retirement income planning, tax planning, beneficiary planning, and broader wealth management considerations. Because inherited retirement account decisions can have long-term implications, evaluating available options carefully may be appropriate before taking action.

This resource is intended to provide a framework for understanding common inherited Traditional IRA considerations. It is not intended as investment, tax, legal, insurance, healthcare, cybersecurity, or financial advice. Individual circumstances vary, and applicable rules may change over time.

If you would like to discuss how this topic fits into your broader financial plan, we invite you to schedule an introductory conversation.