RMD Tables Summary Guide

Reference guide with IRS Uniform Lifetime Table and other RMD tables for calculating required minimum distributions.

Which RMD Table Applies to Me?

Required Minimum Distributions (RMDs) are mandatory withdrawals that generally apply to certain retirement accounts once an individual reaches the applicable RMD age. The IRS uses life expectancy tables to determine the minimum amount that must be distributed each year.

Many retirees review IRS RMD tables annually to understand which table applies to their situation and how their required distribution is calculated.

This resource outlines the primary IRS RMD tables and several issues individuals commonly review when calculating Required Minimum Distributions.

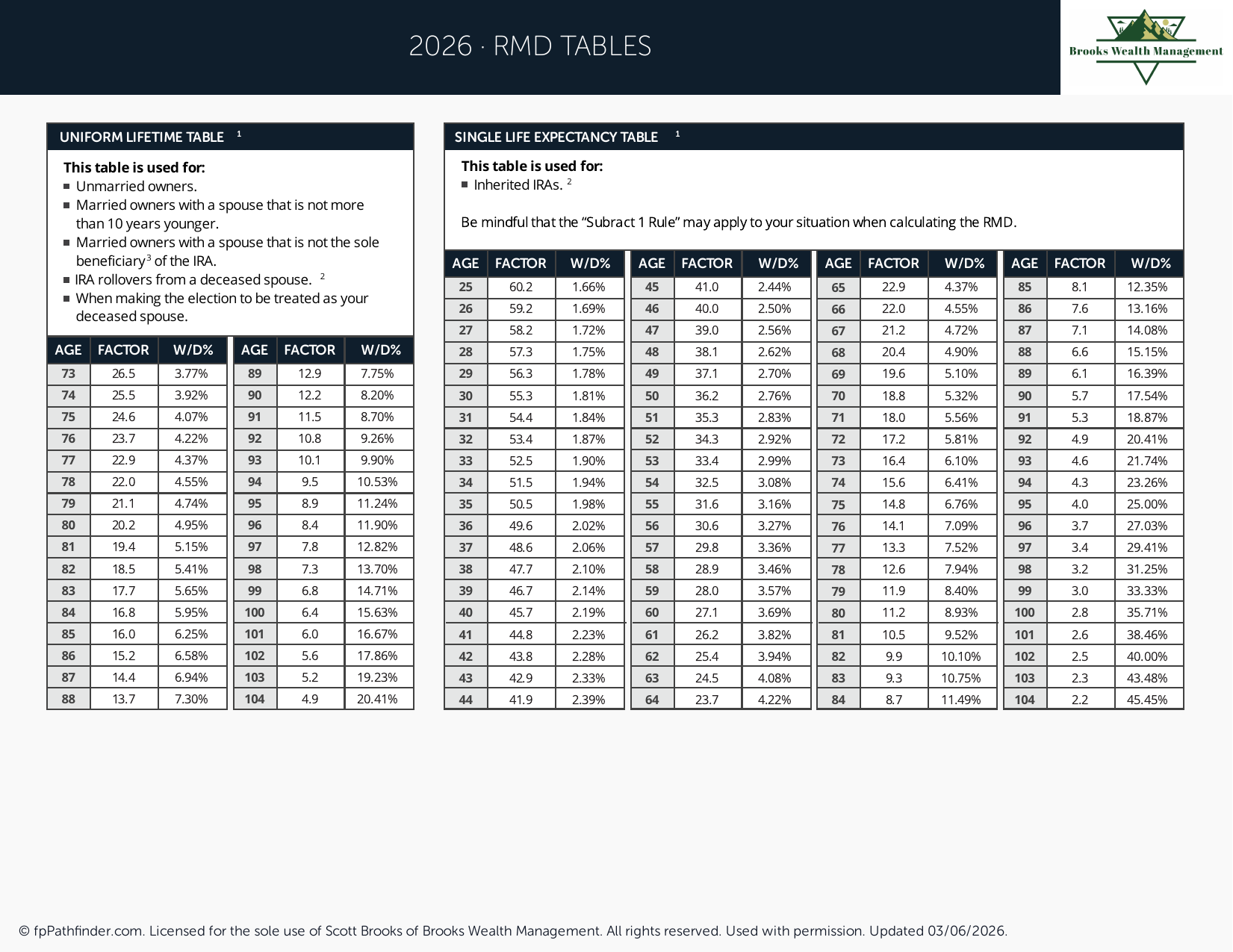

Understanding IRS RMD Tables

The IRS publishes life expectancy tables used to calculate annual Required Minimum Distributions from retirement accounts.

The three primary tables include:

- Uniform Lifetime Table

- Joint Life and Last Survivor Expectancy Table

- Single Life Expectancy Table

The table used depends on the type of retirement account, beneficiary designation, and individual circumstances.

Review Whether the Uniform Lifetime Table Applies

Most retirement account owners use the Uniform Lifetime Table.

This table generally applies to individuals who own:

- Traditional IRAs

- SEP IRAs

- SIMPLE IRAs

- 401(k) plans

- 403(b) plans

- Other employer-sponsored retirement plans subject to RMD rules

For many retirees, the Uniform Lifetime Table provides the life expectancy factor used to calculate annual Required Minimum Distributions.

Review Whether the Joint Life Table Applies

The Joint Life and Last Survivor Expectancy Table may apply when a spouse is the sole beneficiary of the retirement account and is more than ten years younger than the account owner.

Because this table generally produces a longer life expectancy factor, the resulting Required Minimum Distribution may be lower than under the Uniform Lifetime Table.

Many married retirees review beneficiary designations periodically to ensure beneficiary information remains current.

Review Whether the Single Life Expectancy Table Applies

The Single Life Expectancy Table is generally used for certain inherited retirement accounts.

Beneficiaries often review:

- Inherited IRA rules

- Required distribution schedules

- Beneficiary classifications

- SECURE Act distribution requirements

Inherited retirement account distribution rules can differ significantly from those that apply to original account owners.

How RMD Tables Are Used

Required Minimum Distributions are generally calculated using two pieces of information:

- The retirement account balance as of December 31 of the previous year

- The applicable life expectancy factor from the IRS table

The account balance is divided by the applicable distribution factor to determine the minimum amount required to be distributed for the year.

Individuals commonly review account balances, beneficiary designations, and applicable IRS tables before calculating annual RMDs.

Review Your Current RMD Age

Required Minimum Distribution ages have changed under recent legislation.

Many retirees review whether they have reached their applicable RMD age and whether distributions must begin.

Current rules generally provide:

- RMD age 73 for many current retirees

- RMD age 75 for certain younger individuals based on year of birth

Because retirement legislation can change over time, individuals often review current IRS guidance and retirement account requirements periodically.

Review Tax Considerations Related to RMDs

Required Minimum Distributions may affect several areas of retirement planning.

Individuals often review:

- Federal income taxes

- State income taxes

- Medicare IRMAA surcharges

- Social Security taxation

- Retirement withdrawal strategies

- Qualified Charitable Distributions (QCDs)

Many retirees evaluate RMDs as part of a broader retirement income and tax planning review.

Additional information is available in our resources covering:

About This Resource

This resource provides general educational information regarding IRS RMD tables and Required Minimum Distributions. It is not intended as investment, tax, legal, or financial advice. IRS regulations and retirement account rules may change over time.

If you would like to discuss retirement income planning, Required Minimum Distributions, or broader retirement planning considerations, we invite you to schedule an introductory conversation.