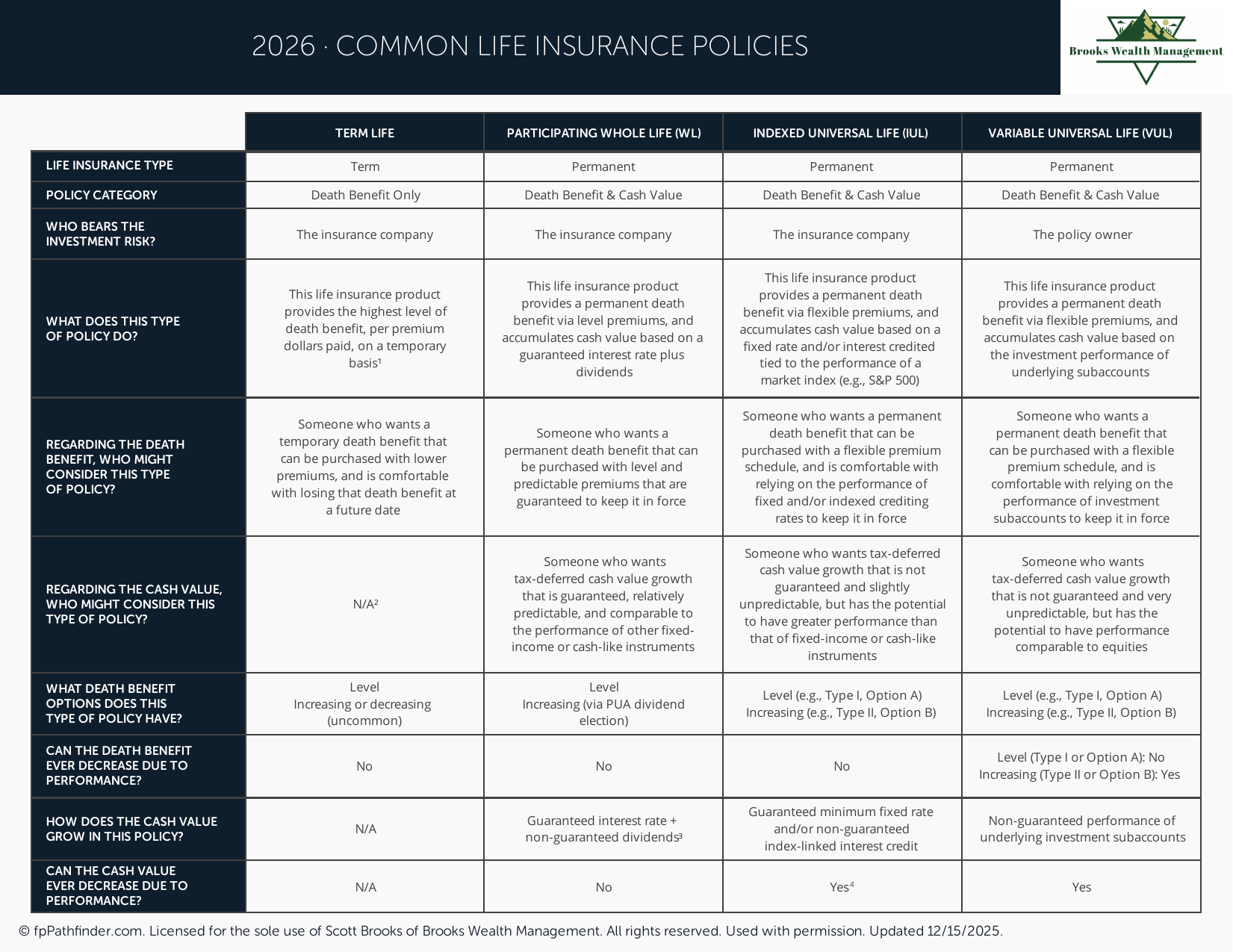

Common Life Insurance Policies

Reference guide comparing term, whole, universal, and variable life insurance policy types.

What Are Common Life Insurance Policies?

Life insurance is often used as part of a broader financial planning strategy to address a variety of goals, including income replacement, family protection, business planning, estate planning, and legacy objectives. Because different types of life insurance policies are designed to address different needs, understanding the common categories can be a helpful first step when evaluating coverage options.

This checklist is designed to provide an overview of common life insurance policy types and the factors individuals often review when comparing them. The objective is not to recommend any particular policy or insurance strategy. Rather, it is intended to provide an educational framework for understanding the characteristics and considerations associated with different forms of coverage.

Review Why Individuals Purchase Life Insurance

Life insurance can serve many different purposes depending on individual circumstances. The role of a policy often depends on family responsibilities, financial obligations, business interests, retirement goals, and estate planning objectives.

Common reasons individuals evaluate life insurance include:

- Income replacement for dependents.

- Mortgage or debt protection.

- Funding future education expenses.

- Business succession planning.

- Estate planning considerations.

- Liquidity needs for beneficiaries.

- Charitable planning objectives.

Because life insurance can serve different purposes, understanding the objective behind the coverage is often an important part of evaluating available policy types.

Review Term Life Insurance

Term life insurance is one of the most commonly discussed forms of life insurance. These policies generally provide coverage for a specified period of time and are often evaluated when individuals seek a death benefit for a defined need or time horizon.

Topics individuals may review when evaluating term life insurance include:

- Coverage duration.

- Death benefit amounts.

- Renewal provisions.

- Conversion features.

- Premium structures.

Term life insurance is often evaluated alongside family protection needs, debt obligations, and other temporary financial responsibilities.

Review Whole Life Insurance

Whole life insurance is a form of permanent life insurance that is generally designed to remain in force for the insured's lifetime if policy requirements are satisfied. These policies often include both a death benefit component and an accumulated value component within the policy.

Individuals evaluating whole life insurance may review:

- Policy guarantees.

- Premium requirements.

- Cash value features.

- Policy loans.

- Death benefit provisions.

- Long-term policy objectives.

As with all insurance products, policy provisions vary and should be reviewed carefully when comparing available options.

Review Universal Life Insurance

Universal life insurance is another form of permanent coverage. These policies often include features that may provide flexibility regarding certain policy elements, subject to policy provisions and limitations.

Topics that individuals sometimes review include:

- Premium flexibility.

- Death benefit options.

- Cash value accumulation.

- Policy funding requirements.

- Long-term policy sustainability.

Because universal life policies can vary significantly by design, understanding how a particular policy operates is often an important part of the evaluation process.

Review Variable and Market-Linked Life Insurance Policies

Some life insurance products include features that may be linked to investment performance or market-based crediting methods. These policies are often more complex than traditional term or permanent life insurance products.

Examples may include:

- Variable life insurance.

- Variable universal life insurance.

- Indexed universal life insurance.

When evaluating these policies, individuals often review factors such as investment-related risks, policy expenses, cash value fluctuations, crediting methodologies, and overall policy objectives.

Because product structures vary significantly, reviewing policy details carefully may help improve understanding of how these policies function.

Review Life Insurance Policies with Additional Features

Some policies may include optional riders or provisions designed to address additional planning objectives. Depending on the policy, available features may vary.

Examples of provisions that individuals sometimes review include:

- Accelerated benefit provisions.

- Long-term care-related riders.

- Disability-related riders.

- Guaranteed insurability provisions.

- Waiver of premium provisions.

Understanding available features can help provide context when comparing policy structures and coverage options.

Review Life Insurance Within the Context of Your Financial Plan

Life insurance decisions are often interconnected with other areas of financial planning. Retirement planning, estate planning, healthcare planning, tax considerations, business ownership, and family circumstances may all influence how life insurance is evaluated.

Related educational resources that may be helpful include:

- What Issues Should I Consider When Purchasing a Life Insurance Policy?

- What Issues Should I Consider When Reviewing My Existing Life Insurance Policy?

- What Issues Should I Consider When Reviewing My Beneficiaries?

Individuals may also find additional planning resources within the Brooks Wealth Management Resource Library.

Questions Worth Reviewing When Comparing Life Insurance Policies

Many individuals find it helpful to review the following questions when evaluating different policy types:

- What purpose is the policy intended to serve?

- How long is coverage needed?

- Are permanent or temporary coverage needs involved?

- What policy features are most important?

- How does the policy fit within broader financial goals?

- How does the policy interact with estate planning objectives?

- What flexibility is desired in the future?

- What policy provisions deserve additional review?

A structured review process can help organize these considerations before evaluating specific products or policies.

How to Use This Checklist

This checklist is intended to serve as an educational resource that introduces common life insurance policy types and planning considerations. It may be useful when beginning research, comparing coverage options, or reviewing life insurance within the context of a broader financial plan.

The checklist does not provide recommendations regarding any insurance carrier, policy type, coverage amount, or planning strategy. Instead, it is designed to help identify topics and questions that may warrant additional review.

About This Resource

This checklist was created as an educational resource to help individuals better understand common life insurance policy types and the planning considerations associated with them. The objective is to provide a framework for reviewing policy characteristics, coverage objectives, and broader financial planning factors.

Because insurance needs vary significantly based on individual circumstances, this resource should be used for educational purposes only and should not be interpreted as a recommendation regarding any insurance product, coverage election, or planning strategy.

If you have questions about how life insurance fits into your broader financial picture, you can schedule an introductory conversation.