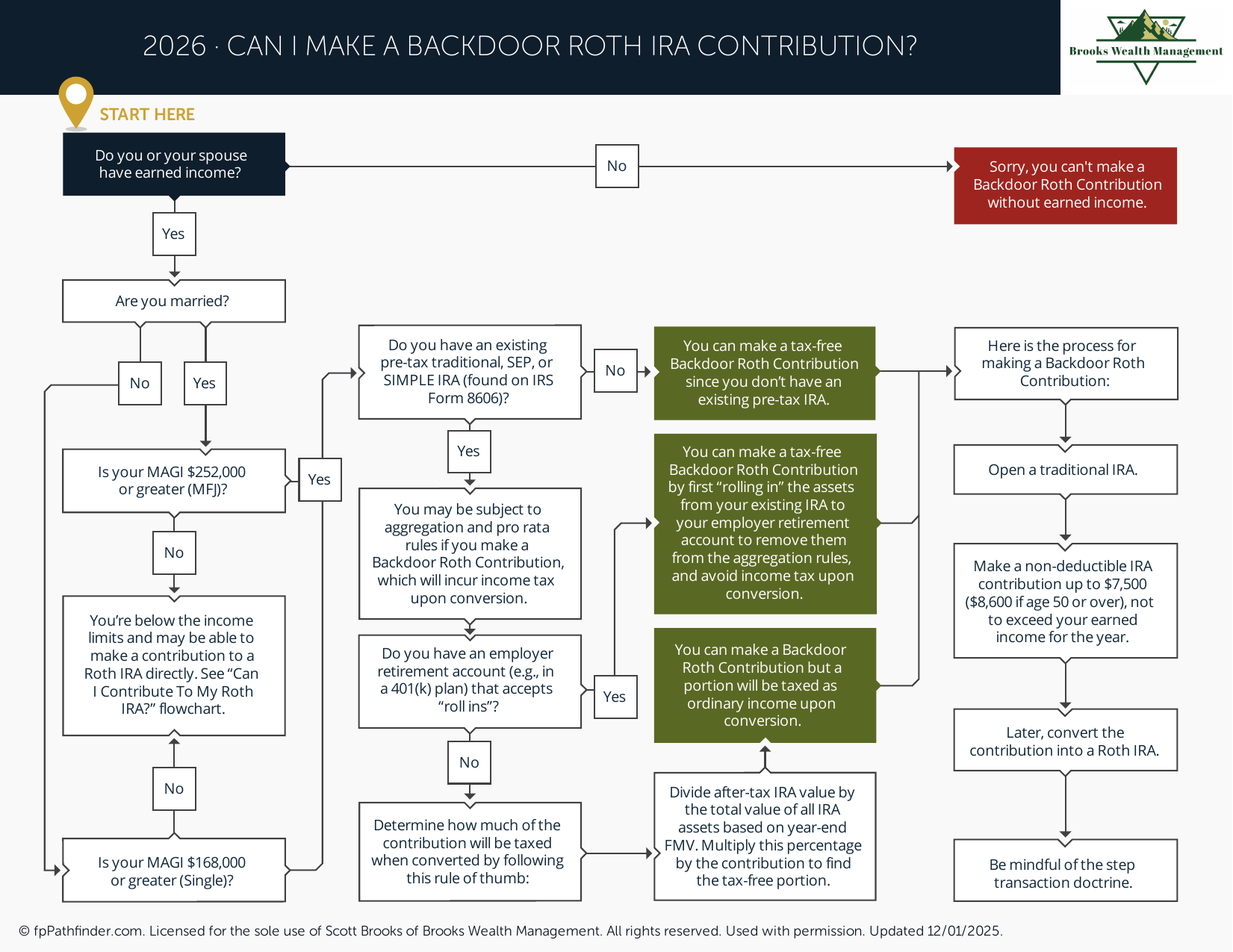

Can I Make a Backdoor Roth IRA Contribution?

Flowchart to determine eligibility and steps for a backdoor Roth IRA contribution.

Can I Make a Backdoor Roth IRA Contribution in 2026? Understanding the Strategy

Many high-income professionals and business owners find themselves in a unique financial position: they earn too much to contribute directly to a Roth IRA, yet they recognize the immense value of tax-free growth and withdrawals in retirement. This is where the **backdoor Roth IRA** strategy becomes a powerful tool. In 2026, the ability to make a **backdoor Roth IRA** contribution remains a viable and important planning technique for those who exceed the income limits for direct Roth contributions. This strategy allows you to effectively bypass the income restrictions and still benefit from a Roth account.

At Brooks Wealth Management, we frequently guide clients through the intricacies of this strategy, ensuring it aligns with their broader financial goals. Understanding the mechanics and potential implications of a **backdoor Roth IRA** is crucial for maximizing your retirement savings.

Why Consider a Backdoor Roth IRA Contribution?

The appeal of a Roth IRA lies in its tax-free withdrawals in retirement, provided certain conditions are met. This means that all the growth your investments experience over decades can be accessed without owing a dime in federal income tax. For high-income earners, who are often in their peak earning years, contributing to a traditional Roth IRA is not an option due to IRS income limitations. However, the **backdoor Roth IRA** provides a legal and IRS-sanctioned pathway to access these benefits.

This strategy is particularly attractive for individuals who anticipate being in a higher tax bracket in retirement than they are today, or who simply want to diversify their tax exposure in their retirement portfolio. Having a mix of pre-tax (like a traditional 401(k) or IRA) and post-tax (Roth) accounts offers flexibility in managing your tax liability during your retirement years. It's a key component of a comprehensive retirement plan, often discussed alongside other savings vehicles. For more on optimizing your savings, explore what accounts you should consider if you want to save more.

The Backdoor Roth IRA Process: A Step-by-Step Guide

The **backdoor Roth IRA** isn't a specific type of account, but rather a two-step process involving a non-deductible traditional IRA contribution followed by a conversion to a Roth IRA. Here's a simplified breakdown:

Step 1: Contribute to a Non-Deductible Traditional IRA. First, you contribute to a traditional IRA. For 2026, the contribution limits are expected to be similar to previous years, but always confirm the latest IRS guidelines. The key here is that this contribution is *non-deductible*, meaning you don't take a tax deduction for it on your current year's tax return. This is critical because it establishes a basis of after-tax money in your traditional IRA.

Step 2: Convert the Traditional IRA to a Roth IRA. Shortly after making the non-deductible contribution, you convert that money from your traditional IRA to a Roth IRA. Because your initial contribution was non-deductible, this conversion is generally a tax-free event. The IRS views this as moving after-tax money from one account to another.

It's important to execute these steps correctly and in close succession to minimize any potential tax complications. The timing can be crucial, especially if you have other pre-tax IRA money. This leads us to a critical consideration: the Pro-Rata Rule.

Navigating the Nuances of the Backdoor Roth IRA and the Pro-Rata Rule

While the **backdoor Roth IRA** strategy is straightforward in concept, its execution requires careful attention, particularly concerning the IRS's "Pro-Rata Rule." This rule comes into play if you hold *any* pre-tax money in *any* traditional IRA, SEP IRA, or SIMPLE IRA accounts at the end of the year in which you perform the conversion. The IRS aggregates all your traditional IRA assets to determine the taxable portion of your Roth conversion.

For example, if you have $94,000 in a pre-tax traditional IRA and you contribute $6,000 as a non-deductible contribution to another traditional IRA, then convert that $6,000 to a Roth, the IRS doesn't see it as converting only the $6,000 after-tax money. Instead, they see you converting 6% of your total IRA assets ($6,000 / $100,000 total IRA balance). This means 94% of your $6,000 conversion would be taxable, defeating the purpose of the **backdoor Roth IRA** strategy.

To avoid the Pro-Rata Rule, the ideal scenario is to have no pre-tax money in any traditional IRA accounts when you perform the conversion. Often, clients can roll their pre-tax IRA funds into their current employer's 401(k) plan, if the plan allows. This effectively clears out the traditional IRA, allowing for a clean **backdoor Roth IRA** conversion. This is a complex area, and professional guidance is highly recommended. For more general information on Roth conversions, you might find our article on whether you should consider doing a Roth conversion helpful.

Is a Backdoor Roth IRA Contribution Right for Your Financial Plan?

Deciding whether to implement a **backdoor Roth IRA** strategy involves more than just understanding the steps; it requires a holistic view of your financial situation, tax planning, and long-term goals. While it's an excellent tool for many high-income earners, it's not universally suitable. Factors such as your current income, existing IRA balances, and future tax expectations all play a role.

At Brooks Wealth Management, we specialize in helping high-income professionals, business owners, and Gen X/Y clients navigate these complex decisions. We consider your entire financial picture, including your investment strategy, tax planning, and estate planning needs, to determine if a **backdoor Roth IRA** aligns with your objectives. Our goal is to provide specific, actionable advice that helps you build lasting wealth and achieve financial independence. We offer a range of free resources and transparent pricing to help you get started.

About This Resource

This article provides general information about the backdoor Roth IRA strategy and is not intended as personalized financial or tax advice. The rules and regulations surrounding retirement accounts can be complex and are subject to change. For tailored guidance specific to your unique financial situation, we encourage you to schedule a consultation with a qualified financial advisor at Brooks Wealth Management. You can reach out to us directly through our contact page to book a consultation.

Have Questions About Your Situation?

This resource is a starting point. A free consultation with Scott Brooks, CFP® gives you a personalized perspective.

Book a Free ConsultationBased in Westlake Village, CA · Ventura County · Serving clients across all 50 states

Brooks Wealth Management is a Registered Investment Adviser (RIA) in the State of California. Registration does not imply a certain level of skill or training. This resource is provided for educational and informational purposes only and does not constitute investment, tax, or legal advice. Scott Brooks, CFP® · CRD #7227609 · Firm CRD #332237 · 2555 Townsgate Rd STE 200, Westlake Village, CA 91361