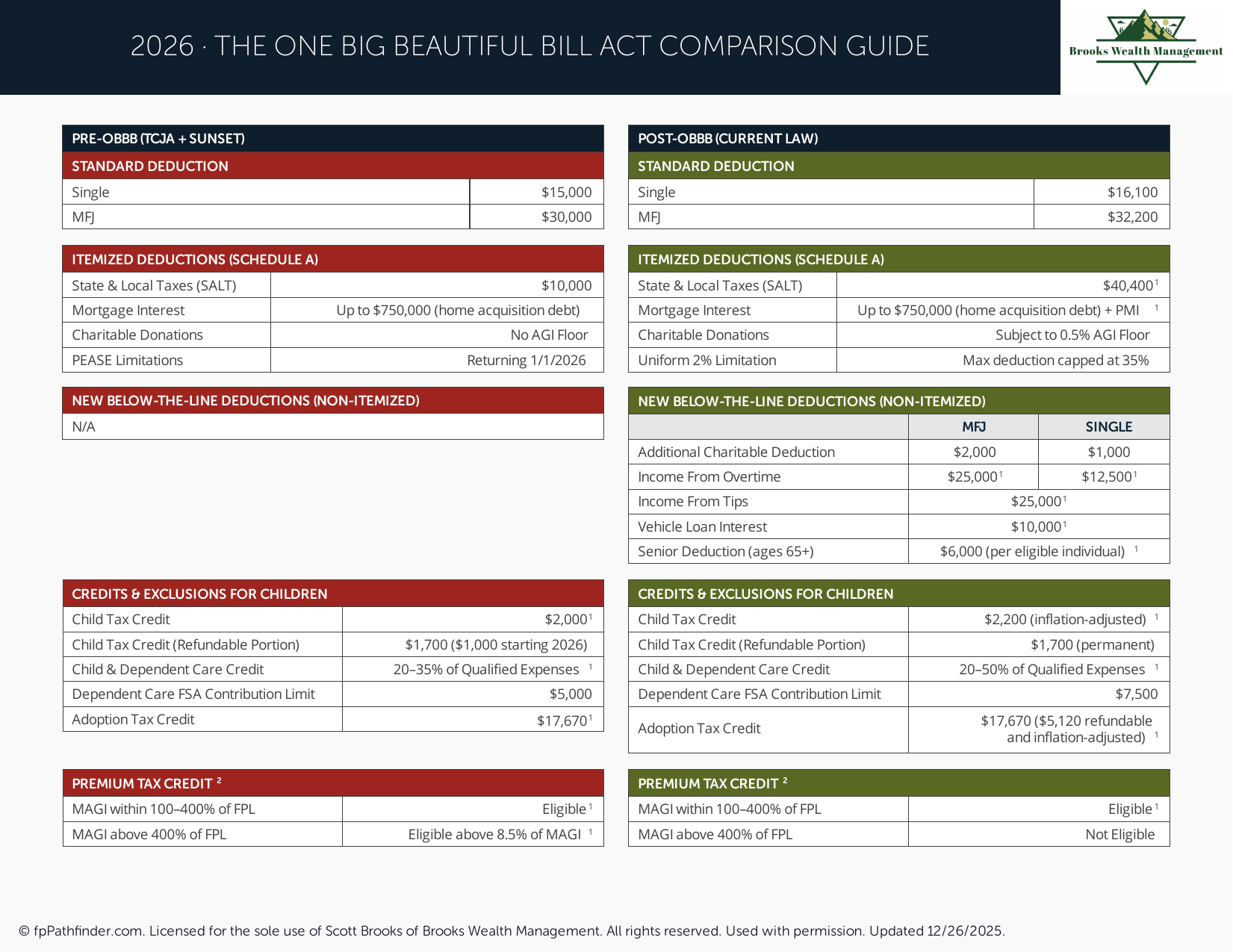

The One Big Beautiful Bill Act — Comparison Guide 2026

Side-by-side comparison guide of key tax and financial planning changes under the One Big Beautiful Bill Act.

What Important Issues Should I Consider Regarding Changes Made by the OBBBA?

The One Big Beautiful Bill Act, commonly referred to as the OBBBA, was signed into law on July 4, 2025, as Public Law 119-21. The law includes a broad range of federal tax, deduction, credit, business, healthcare, and savings provisions that may affect individual taxpayers, families, retirees, employees, and business owners.

Because many provisions apply differently based on income, filing status, age, employment type, business ownership, and timing, individuals often review the OBBBA as part of a broader tax and financial planning process.

Review Individual Income Tax Changes

The OBBBA includes several provisions affecting individual income taxes, deductions, credits, and filing considerations. Some provisions apply beginning with the 2025 tax year, while others may apply in later years or only for a limited period.

- Review whether current federal income tax brackets affect projected taxable income.

- Review whether standard deduction rules may affect itemizing decisions.

- Review whether temporary deductions may apply to your situation.

- Review whether income phaseouts may limit available deductions or credits.

- Review whether withholding or estimated tax payments should be revisited.

Review Temporary Deductions

The OBBBA created or modified several deductions that may apply only under specific circumstances. These provisions may be subject to income limits, documentation requirements, and expiration dates.

- Review whether qualified tip income provisions may apply.

- Review whether qualified overtime pay provisions may apply.

- Review whether auto loan interest deductions may apply for eligible vehicles.

- Review whether age-based deductions may apply for older taxpayers.

- Review whether any temporary provisions require updated tax planning before expiration.

Review Retirement Planning Considerations

Tax law changes may affect retirement planning decisions, including pre-tax contributions, Roth contributions, Roth conversions, retirement account withdrawals, and long-term tax projections.

- Review whether pre-tax or Roth retirement contributions should be evaluated.

- Review whether Roth conversion planning may be affected by current tax rates.

- Review how future required minimum distributions may affect taxable income.

- Review how retirement withdrawals may interact with Social Security, pensions, and investment income.

- Review whether tax planning should be coordinated across multiple tax years.

Individuals preparing for retirement may also wish to review what issues to consider before retirement.

Review Business Owner Planning

The OBBBA includes provisions affecting business deductions, depreciation, research and development costs, reporting thresholds, and other business tax planning issues.

- Review whether business expensing rules may affect planned equipment or property purchases.

- Review whether depreciation provisions may affect cash flow planning.

- Review whether research and development expense rules may apply.

- Review whether qualified business income rules should be evaluated.

- Review whether estimated tax payments should be updated based on projected business income.

- Review whether entity structure remains appropriate under current law.

Business owners may also wish to review issues to consider as a business owner or 1099 worker.

Review Healthcare and HSA Planning

The OBBBA includes provisions that may affect Health Savings Accounts, healthcare planning, and eligibility considerations for certain taxpayers.

- Review whether HSA eligibility rules may affect your ability to contribute.

- Review whether your health insurance plan remains HSA-compatible.

- Review how telehealth coverage may interact with HSA eligibility.

- Review whether current or future medical expenses should be coordinated with HSA planning.

- Review whether HSA contributions fit within your broader savings strategy.

Review Family and Education Savings

Families may want to review how OBBBA provisions affect child-related planning, education savings, and long-term savings for minors.

- Review whether child-related tax credits or deductions may apply.

- Review whether education savings strategies should be revisited.

- Review whether 529 plan strategies remain aligned with family goals.

- Review whether new child savings account provisions may be relevant.

- Review whether beneficiary designations and account ownership should be updated.

Review Investment and Taxable Account Planning

Changes in tax law may affect investment income, taxable accounts, capital gains planning, charitable giving, and withdrawal sequencing.

- Review capital gains planning opportunities.

- Review tax-loss harvesting considerations.

- Review dividend and interest income exposure.

- Review whether portfolio income affects tax thresholds or deductions.

- Review how taxable accounts coordinate with retirement accounts.

Review Estate and Wealth Transfer Planning

Federal tax legislation may affect estate planning, gifting strategies, trust planning, and long-term wealth transfer decisions.

- Review whether estate and gift tax exemption rules affect your plan.

- Review whether existing estate documents reflect current goals.

- Review beneficiary designations on retirement accounts, insurance policies, and taxable accounts.

- Review whether lifetime gifting strategies should be evaluated.

- Review how inherited retirement accounts may be taxed.

Review Timing and Coordination

Many provisions of the OBBBA have different effective dates, expiration dates, phaseouts, and implementation requirements. Timing may affect whether a provision applies and how it interacts with other parts of a financial plan.

- Review which provisions apply to the current tax year.

- Review which provisions begin in future years.

- Review whether temporary provisions are scheduled to expire.

- Review whether additional IRS guidance may be needed.

- Review whether planning should be coordinated with a CPA, attorney, or other tax professional.

About This Resource

This resource provides general educational information regarding the One Big Beautiful Bill Act and related tax and financial planning considerations. The OBBBA includes provisions affecting individual income taxes, deductions, credits, business tax planning, healthcare planning, Health Savings Accounts, family savings, retirement planning, and estate planning.

This checklist is intended to help organize key questions and planning topics associated with the OBBBA. It is not intended to provide recommendations, determine eligibility for any tax benefit, or identify what actions may be appropriate for any particular individual. Individual circumstances vary, and tax rules may change over time.

If you would like to discuss how this topic fits into your broader financial plan, we invite you to schedule an introductory conversation.