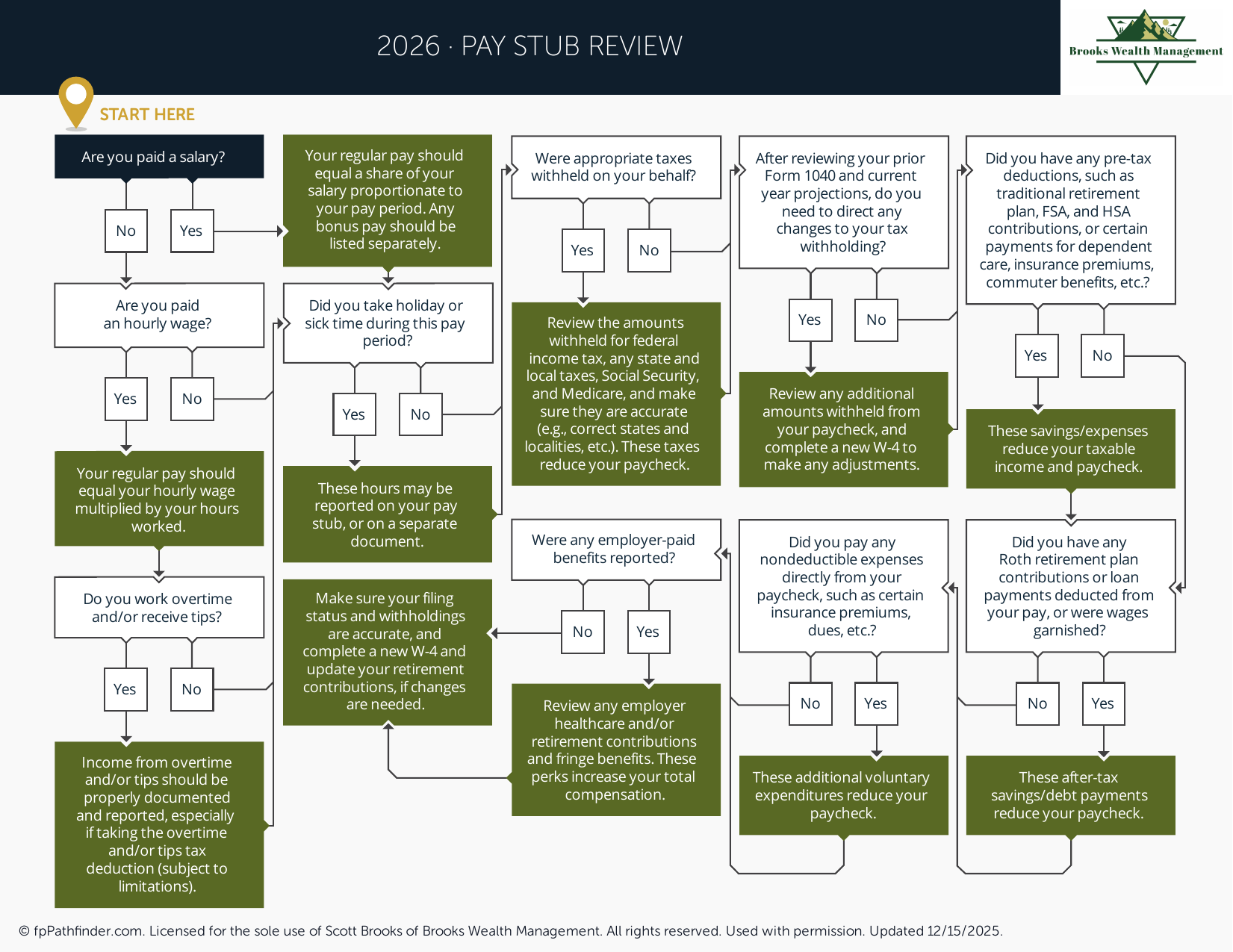

Pay Stub Review

Guide to reviewing your pay stub to ensure correct tax withholding and benefit elections.

What Should I Review on My Pay Stub?

Your pay stub contains more than just your take-home pay. It provides important information about compensation, tax withholding, retirement contributions, employee benefits, and payroll deductions. Reviewing your pay stub periodically can help ensure that your compensation and deductions are being processed accurately and that your financial planning assumptions remain aligned with reality.

While payroll systems are generally automated, mistakes can occur. Taking a few minutes to review your pay stub throughout the year may help identify issues before they become larger tax, cash flow, or benefit-related problems.

Verify Personal and Employment Information

One of the first items to review is your personal information. Confirm that your name, address, employee identification information, and other relevant details are accurate. Errors in payroll records can sometimes create issues with tax reporting, benefit administration, or year-end tax forms.

You should also confirm that the pay period dates, payment date, and compensation information accurately reflect your employment arrangement.

Review Gross Pay and Compensation

Your gross pay represents earnings before taxes and deductions. Reviewing gross pay can help ensure that salary, hourly wages, overtime, bonuses, commissions, equity compensation, or other forms of compensation have been processed correctly.

Individuals who receive variable compensation may wish to compare current pay periods against prior statements to verify consistency and identify any unexpected changes.

Check Retirement Contributions and Pre-Tax Deductions

Many employees make contributions to retirement plans, health savings accounts (HSAs), flexible spending accounts (FSAs), or other employer-sponsored benefit programs through payroll deductions. Reviewing these deductions periodically may help ensure contributions match your elections and financial goals.

If retirement savings is a current priority, you may find our guide on accounts to consider if you want to save more helpful.

Employees participating in traditional or Roth retirement plans may also wish to verify that contributions are being directed to the intended account type and at the intended contribution rate.

Review Tax Withholding Amounts

Your pay stub typically includes federal income tax withholding, state income tax withholding (where applicable), Social Security taxes, and Medicare taxes. Reviewing these amounts may help you determine whether your current withholding elections remain appropriate.

Life events such as marriage, divorce, children, changes in income, bonuses, stock compensation, or multiple sources of household income may affect withholding needs. Periodically reviewing your Form W-4 elections can help ensure withholding remains aligned with your overall tax situation.

Understand Benefit Deductions

Many employers provide benefits such as health insurance, dental insurance, vision coverage, disability insurance, life insurance, employee stock purchase plans, and other workplace benefits. Reviewing your pay stub can help confirm that deductions related to these programs are accurate and consistent with your enrollment elections.

If changes occur during open enrollment or after a qualifying life event, reviewing future pay stubs can help confirm those changes have been implemented correctly.

Confirm Net Pay and Cash Flow

Net pay represents the amount received after taxes and deductions. Reviewing net pay can help identify unexpected changes in compensation, withholding, or deductions that may affect monthly cash flow.

Comparing your pay stub to your bank deposit may also help ensure payroll transactions are being processed correctly.

For a broader discussion of cash flow planning, budgeting, and spending decisions, you may find our free resource library helpful.

How Pay Stub Reviews Fit Into Financial Planning

Your pay stub can provide valuable information about compensation, savings rates, tax withholding, and employee benefits. Regular reviews may help ensure that your financial plan reflects your current income and workplace benefits while identifying potential issues that warrant further attention.

For many professionals, compensation packages extend beyond salary and may include bonuses, stock compensation, deferred compensation plans, retirement benefits, and other incentives. Understanding how those items appear on your pay stub can support more informed financial decision-making.

About This Resource

This resource provides general educational information regarding pay stubs, payroll deductions, employee benefits, tax withholding, and related financial planning considerations. Every individual's circumstances are different, and financial decisions should be evaluated based on personal goals, income, tax considerations, and available benefits.

Brooks Wealth Management works with professionals, business owners, retirees, and families on a wide range of financial planning topics. If you would like to discuss your situation, we invite you to schedule an introductory conversation or learn more about our approach on our pricing page.

Have Questions About Your Situation?

This resource is intended for educational purposes only. If you would like to discuss your circumstances, schedule an introductory conversation with Scott Brooks, CFP®.

Schedule an Introductory ConversationVentura County, California · Serving Clients Throughout California and Across the United States

Brooks Wealth Management is a Registered Investment Adviser registered with the State of California. Registration does not imply a certain level of skill or training. This content is provided for informational and educational purposes only and should not be construed as investment, tax, legal, or accounting advice. Advisory services are offered only to clients or prospective clients where Brooks Wealth Management and its representatives are properly licensed or exempt from licensure. Investing involves risk, including the potential loss of principal. CFP® is a certification mark owned by the Certified Financial Planner Board of Standards, Inc. Scott Brooks, CFP® · CRD #7227609 · Firm CRD #332237