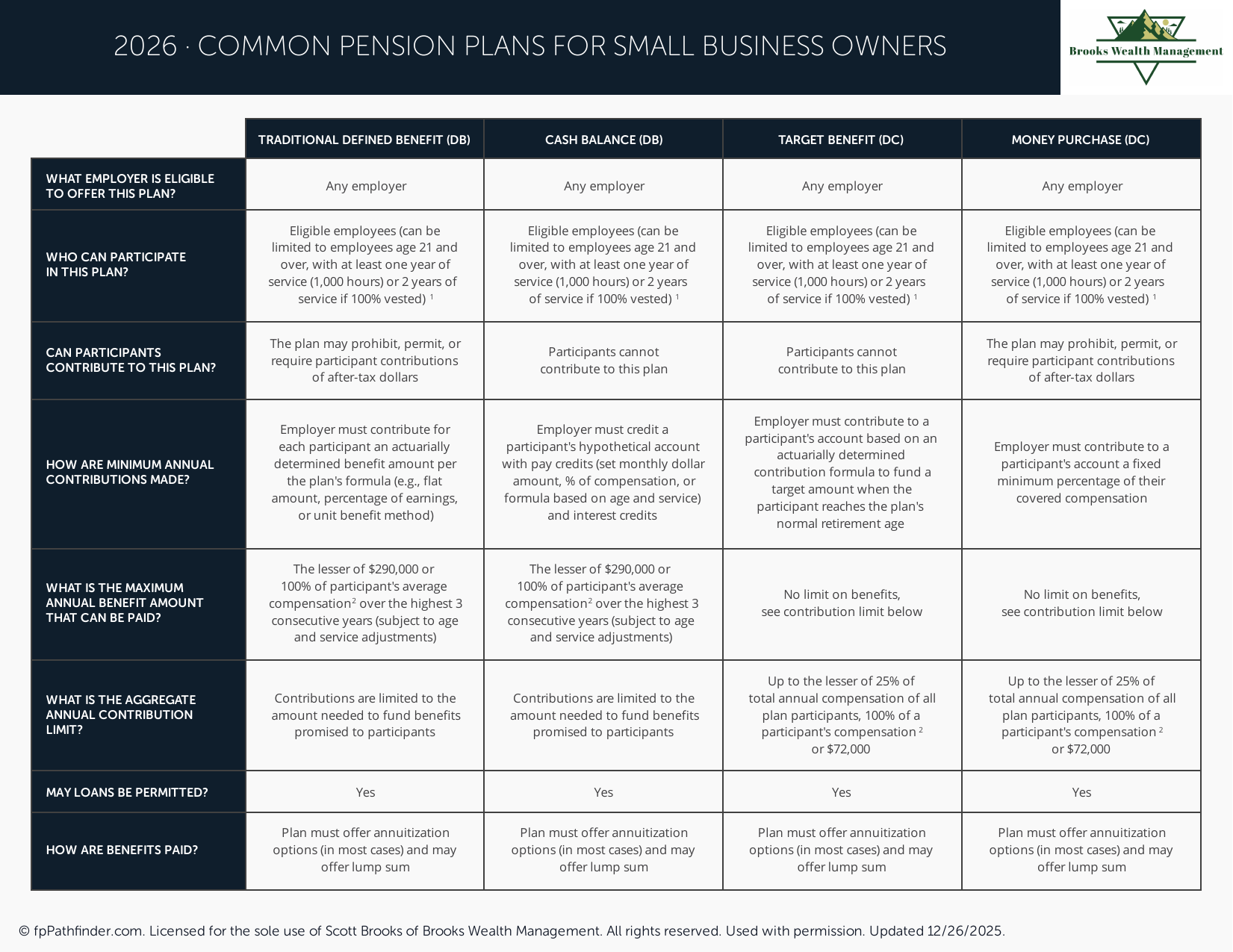

Common Pension Plans for Small Business Owners

Reference guide comparing defined benefit and pension plan options for business owners.

Navigating Pension Plans for Small Business Owners in 2026

As a small business owner, planning for your own retirement and offering competitive benefits to your employees can feel like a complex puzzle. Understanding the various pension plans small business owners can implement is crucial for long-term financial security and attracting top talent. In 2026, the landscape of retirement planning continues to evolve, offering a range of options tailored to different business sizes and objectives.

Choosing the right retirement plan is not a one-size-fits-all decision. It requires careful consideration of your business structure, cash flow, employee demographics, and personal retirement goals. At Brooks Wealth Management, we guide our clients through these critical choices, ensuring they select a plan that aligns with their unique circumstances and maximizes tax advantages.

Understanding Your Options: Common Pension Plans for Small Business

When considering pension plans small business owners have at their disposal, it is important to differentiate between various types, each with its own set of rules, contribution limits, and administrative burdens. Here are some of the most common and effective options:

Simplified Employee Pension (SEP) IRA

A SEP IRA is an excellent choice for self-employed individuals and small business owners with few or no employees. It is relatively simple to set up and administer, making it a popular option. Contributions are made solely by the employer, are tax-deductible, and grow tax-deferred. The contribution limit for 2026 is expected to be a significant percentage of compensation, up to a maximum dollar amount, making it ideal for owners looking to save a substantial amount for retirement. Employees must be at least 21, have worked for the employer in at least three of the last five years, and have received a certain amount of compensation.

Savings Incentive Match Plan for Employees (SIMPLE) IRA

The SIMPLE IRA is designed for small businesses with 100 or fewer employees. It offers a straightforward way for both employers and employees to contribute to retirement savings. Employers can choose to either match employee contributions up to 3% of compensation or make a fixed 2% non-elective contribution for all eligible employees. This plan encourages employee participation and is generally less complex than a 401(k), though it has lower contribution limits. For more insights into saving strategies, consider exploring what accounts you should consider if you want to save more.

Solo 401(k)

For self-employed individuals or business owners with no full-time employees other than themselves or a spouse, the Solo 401(k) offers the highest contribution limits. You can contribute both as an employee (up to the standard 401(k) limit) and as an employer (profit-sharing contributions), significantly boosting your retirement savings. This plan allows for both pre-tax and Roth contributions, providing flexibility in tax planning. It is a powerful tool for maximizing personal retirement savings while running your own business.

Advanced Pension Plans Small Business Owners Might Consider

Beyond the simpler options, some small businesses may benefit from more robust retirement structures, particularly as they grow or if they have specific goals for employee retention and higher contribution levels.

Traditional 401(k)

A traditional 401(k) plan is a well-known option that allows both employers and employees to contribute. It offers higher contribution limits than SIMPLE IRAs and can include features like Roth contributions, loans, and hardship withdrawals. While more complex to administer, a 401(k) can be highly attractive to employees and provides significant tax benefits. Setting up and managing a 401(k) requires careful planning and adherence to IRS regulations, making professional guidance invaluable.

Defined Benefit Plans (Cash Balance Plans)

For business owners looking to make very large, tax-deductible contributions, a defined benefit plan, often structured as a cash balance plan, can be an excellent strategy. These plans promise a specific benefit at retirement, and contributions are actuarially determined to meet that promise. They are more complex and costly to administer but offer unparalleled savings potential, especially for older business owners nearing retirement who want to accelerate their savings. This type of plan can be a game-changer for those with significant disposable income and a desire to maximize tax-deferred growth.

Choosing the Right Pension Plans for Small Business: Key Considerations

Selecting the optimal retirement plan involves weighing several factors. First, consider your business size and growth trajectory. A SEP or SIMPLE IRA might be perfect for a startup, while a growing business might transition to a 401(k). Second, evaluate your budget for employer contributions and administrative costs. Simpler plans have lower costs. Third, think about your employees: what level of participation do you expect, and what benefits will help you attract and retain talent? Finally, align the plan with your personal financial goals, including how much you want to save and your desired tax strategy.

Understanding these nuances and navigating the regulatory requirements can be challenging. We encourage you to review our free resources for additional information or to contact us directly for personalized advice.

About This Resource

This resource provides general information on common pension plans small business owners can consider. For tailored advice specific to your business and personal financial situation, we invite you to schedule a consultation with a CFP® professional at Brooks Wealth Management. Visit our contact page to book your appointment today and start building a robust financial future for your business and yourself.

Have Questions About Your Situation?

This resource is a starting point. A free consultation with Scott Brooks, CFP® gives you a personalized perspective.

Book a Free ConsultationBased in Westlake Village, CA · Ventura County · Serving clients across all 50 states

Brooks Wealth Management is a Registered Investment Adviser (RIA) in the State of California. Registration does not imply a certain level of skill or training. This resource is provided for educational and informational purposes only and does not constitute investment, tax, or legal advice. Scott Brooks, CFP® · CRD #7227609 · Firm CRD #332237 · 2555 Townsgate Rd STE 200, Westlake Village, CA 91361