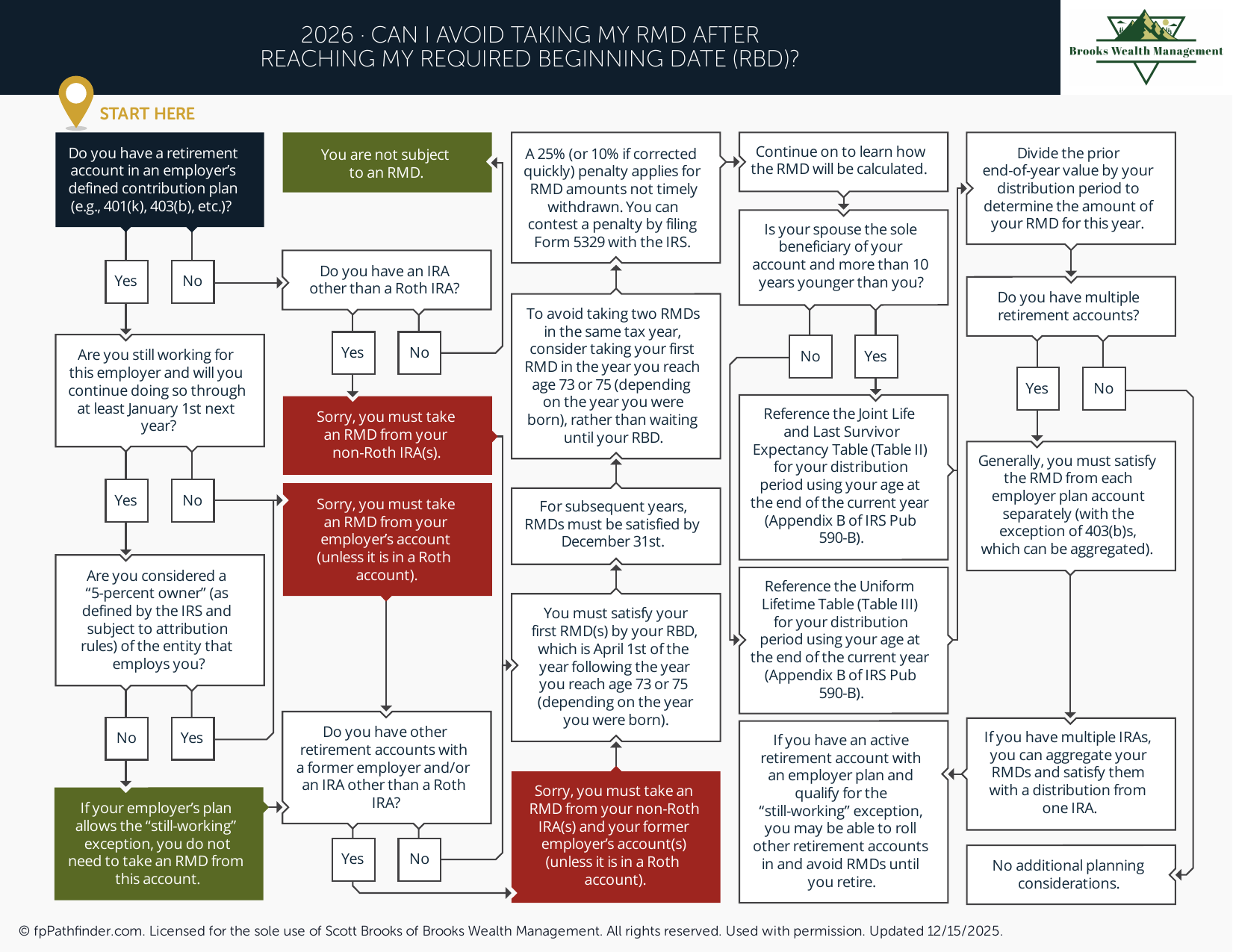

Can I Avoid Taking My RMD After Reaching My Required Beginning Date (RBD)?

Flowchart to determine whether you can delay or avoid required minimum distributions after your RBD.

Can I Avoid Taking My Required Minimum Distribution (RMD) After My Required Beginning Date (RBD)?

Required Minimum Distributions (RMDs) are mandatory withdrawals from certain retirement accounts once you reach the applicable RMD age established by federal law. After your Required Beginning Date (RBD), most retirement account owners are generally required to begin taking annual distributions.

If you are reviewing whether you can avoid taking an RMD after your RBD, several issues are commonly considered.

Review Whether You Have Reached Your Required Beginning Date

Your Required Beginning Date is generally April 1 of the year following the year you reach your applicable RMD age.

Under current law:

- Individuals born between 1951 and 1959 generally begin RMDs at age 73.

- Individuals born in 1960 or later generally begin RMDs at age 75.

Once your Required Beginning Date has passed, annual RMD requirements generally apply unless a specific exception is available.

Review Whether You Qualify for the Still-Working Exception

Some employer-sponsored retirement plans allow participants to delay RMDs while actively employed.

Individuals often review:

- Whether they are still employed by the sponsoring employer

- Whether the retirement plan permits the exception

- Whether they meet any ownership restrictions under plan rules

The still-working exception generally does not apply to traditional IRAs.

Review Whether a Qualified Charitable Distribution (QCD) May Be Appropriate

Individuals age 70½ or older may be eligible to make Qualified Charitable Distributions directly from an IRA to a qualified charity.

A QCD may satisfy part or all of an RMD obligation while excluding the distributed amount from taxable income, subject to applicable rules and limitations.

For individuals who regularly support charitable organizations, reviewing QCD eligibility may be an important part of RMD planning.

Review Future RMD Reduction Strategies

Although current RMDs generally cannot be avoided after reaching the Required Beginning Date, some individuals review strategies that may reduce future RMD obligations.

Common planning topics include:

- Roth conversions

- Qualified Charitable Distributions

- Retirement account consolidation

- Tax-efficient withdrawal planning

- Estate planning considerations

For additional information, review our resources on Roth conversions and retirement withdrawal strategies.

Review Potential Tax Consequences

RMDs are generally taxable as ordinary income and may affect:

- Federal income taxes

- State income taxes

- Social Security taxation

- Medicare IRMAA surcharges

- Overall retirement income planning

Understanding how an RMD interacts with other sources of retirement income is often an important part of annual financial planning.

About This Resource

This resource provides general educational information regarding Required Minimum Distributions and Required Beginning Dates. IRS rules are subject to change and individual circumstances may vary. This information should not be interpreted as tax, legal, or financial advice.

If you would like to discuss your retirement distribution strategy, we invite you to schedule an introductory conversation.