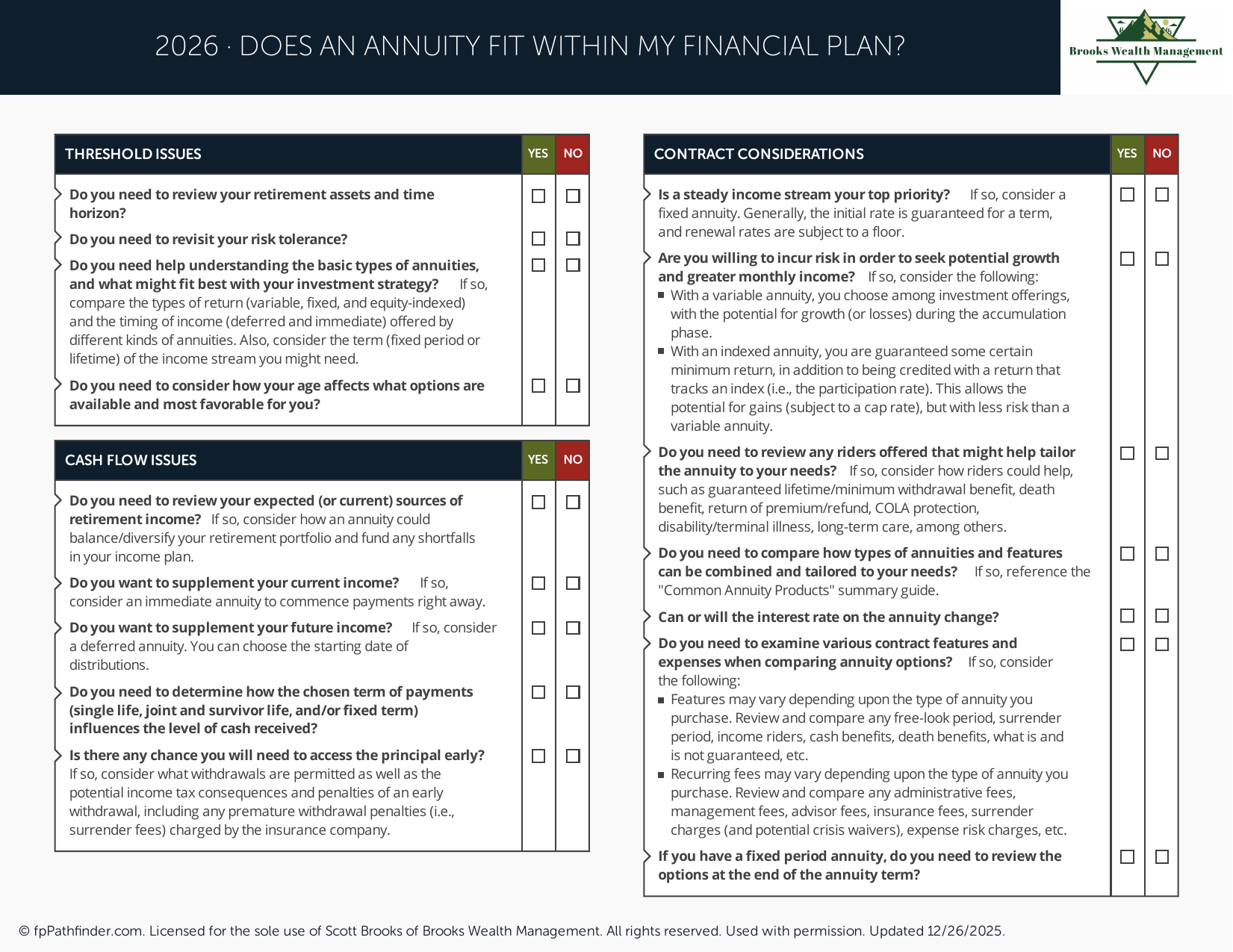

Does an Annuity Fit within My Financial Plan?

Decision flowchart to evaluate whether an annuity is appropriate for your financial situation.

Does an Annuity Belong in a Financial Plan?

Annuities are insurance contracts that may provide tax-deferred growth, guaranteed income, or other features depending on the type of annuity selected. Whether an annuity belongs in a financial plan depends on an individual's goals, income needs, risk tolerance, liquidity requirements, and existing retirement resources.

While some individuals use annuities to create predictable retirement income, others may determine that alternative investment or retirement planning strategies better align with their objectives. Reviewing both the benefits and limitations is an important part of evaluating any annuity decision.

Review What an Annuity Is

An annuity is a contract issued by an insurance company. In exchange for a lump-sum payment or a series of contributions, the insurance company agrees to provide certain benefits, which may include future income payments, principal protection features, or tax-deferred accumulation.

Common considerations include:

- Whether income payments begin immediately or at a future date.

- Whether contract values fluctuate with investment markets.

- Whether guarantees are backed by the claims-paying ability of the issuing insurance company.

- How withdrawals, income payments, and death benefits are structured.

Annuities are often reviewed alongside other retirement income sources such as employer retirement plans, IRAs, taxable investment accounts, pensions, and Social Security benefits.

Review Different Types of Annuities

Not all annuities function the same way. The features, risks, costs, and potential outcomes can vary significantly depending on the contract type.

Fixed Annuities

Fixed annuities generally provide a stated interest rate or guaranteed accumulation schedule for a defined period.

Individuals often review fixed annuities when seeking:

- Predictable account growth.

- Principal protection features.

- Reduced exposure to market volatility.

- Future guaranteed income options.

Fixed annuities may be compared with other conservative savings and income-oriented vehicles when evaluating retirement strategies.

Variable Annuities

Variable annuities allow assets to be invested in underlying investment options that may increase or decrease in value based on market performance.

Common considerations include:

- Investment risk.

- Contract expenses and rider costs.

- Income benefit features.

- Tax-deferred growth opportunities.

- Liquidity restrictions and surrender periods.

Because contract features can vary significantly, individuals often review the specific costs and benefits before purchasing a variable annuity.

Indexed Annuities

Indexed annuities generally tie potential interest credits to the performance of a market index while also providing varying levels of downside protection.

Common considerations include:

- Participation rates.

- Caps on credited returns.

- Spreads or margin adjustments.

- Minimum guarantees.

- Surrender schedules.

Performance outcomes may differ substantially from the performance of the underlying market index itself.

Review Situations Where Annuities Are Commonly Considered

Annuities are often evaluated as part of a broader retirement income strategy rather than as a standalone solution.

Individuals commonly review annuities when they are seeking:

- A source of predictable retirement income.

- Protection against longevity risk.

- Additional tax-deferred accumulation after maximizing other retirement accounts.

- Reduced exposure to market volatility.

- A portion of retirement income that is not dependent on investment portfolio withdrawals.

Whether these features are beneficial depends on individual financial circumstances and overall planning objectives.

Review Potential Benefits and Limitations

Annuities may offer advantages for some individuals, but they also involve tradeoffs that should be reviewed carefully.

Potential benefits may include:

- Guaranteed income features.

- Tax-deferred growth.

- Principal protection provisions in certain contracts.

- Death benefit features.

- Reduced exposure to market fluctuations in some annuity types.

Potential limitations may include:

- Surrender charges.

- Limited liquidity.

- Contract complexity.

- Insurance-related expenses and rider fees.

- Tax treatment of withdrawals.

- Inflation risk for fixed payment streams.

Reviewing both the advantages and disadvantages can help provide context when evaluating how an annuity may affect a broader financial plan.

Review Tax Considerations

Many annuities provide tax-deferred growth, meaning earnings generally are not taxed until withdrawn.

Common considerations include:

- Tax treatment of withdrawals.

- Ordinary income taxation of earnings.

- Early withdrawal penalties when applicable.

- Required minimum distribution rules for qualified annuities.

- Coordination with other retirement accounts and income sources.

Because tax outcomes depend on individual circumstances, annuity decisions are often reviewed within the context of an overall retirement income and tax strategy.

Review Whether an Annuity Fits Within a Broader Retirement Income Plan

Annuities are one of many tools that may be considered when building a retirement income strategy. They are commonly evaluated alongside Social Security benefits, employer retirement plans, taxable investment accounts, pensions, and other income sources.

Common questions individuals review include:

- How much guaranteed income is needed to cover essential expenses?

- How much liquidity should remain available?

- What role should market-based investments play in retirement?

- How important is leaving assets to beneficiaries?

- How might inflation affect future purchasing power?

The answers to these questions often influence whether an annuity is appropriate, unnecessary, or only suitable for a portion of a retirement strategy.

About This Resource

This resource provides general educational information regarding annuities and retirement income planning. It is not intended as investment, tax, legal, insurance, healthcare, cybersecurity, or financial advice. Individual circumstances vary and contract provisions may differ among insurance companies.

If you would like to discuss how this topic fits into your broader financial plan, we invite you to schedule an introductory conversation.