AGI/MAGI Summary Guide

Reference guide explaining adjusted gross income (AGI) and modified AGI (MAGI) and their impact on tax planning.

What Is the Difference Between AGI and MAGI?

Adjusted Gross Income (AGI) and Modified Adjusted Gross Income (MAGI) are two important figures used throughout the tax code. These calculations can affect eligibility for certain deductions, credits, retirement account contributions, Medicare premiums, and other financial planning considerations.

Although the terms are often used together, AGI and MAGI are not the same. Understanding the difference can help taxpayers better understand how various tax rules apply to their situation.

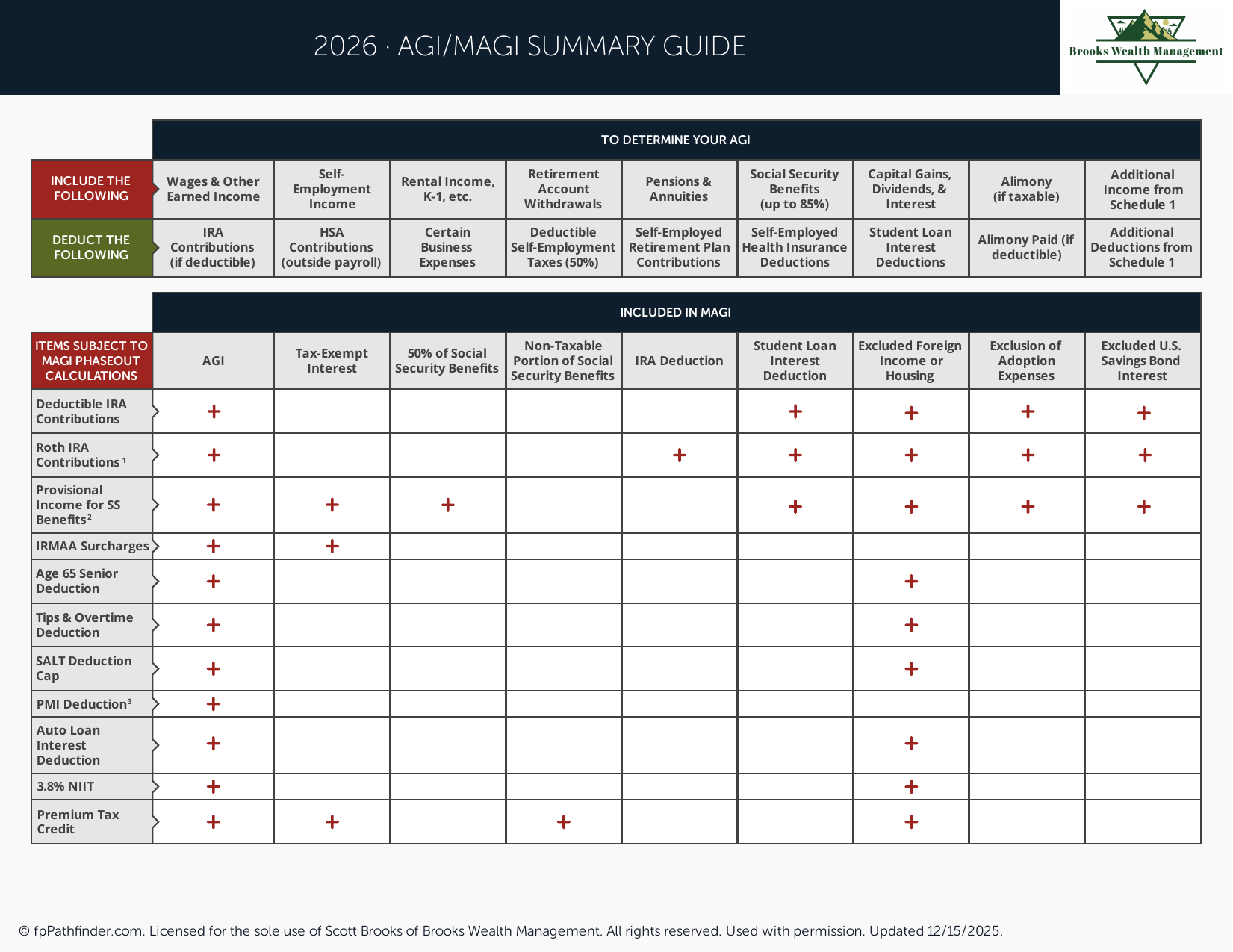

What Is Adjusted Gross Income (AGI)?

Adjusted Gross Income (AGI) is generally your total income from all taxable sources, reduced by certain eligible adjustments allowed under federal tax law.

Examples of income that may be included when calculating AGI include:

- Wages and salary

- Business income

- Interest income

- Dividend income

- Capital gains

- Rental income

- Retirement distributions

Certain adjustments may reduce gross income before arriving at AGI, depending on individual circumstances and applicable tax rules.

What Is Modified Adjusted Gross Income (MAGI)?

Modified Adjusted Gross Income (MAGI) begins with AGI and then adds back certain deductions, exclusions, or adjustments.

There is no single MAGI calculation used throughout the tax code. Different tax provisions may require different MAGI calculations depending on the specific rule being applied.

Because of this, the MAGI used for one tax benefit may differ from the MAGI used for another.

Why AGI and MAGI Matter

AGI and MAGI are commonly used to determine eligibility for a variety of tax-related benefits and planning opportunities.

These may include:

- Roth IRA contribution eligibility

- Traditional IRA deduction eligibility

- Health insurance premium tax credits

- Medicare premium adjustments (IRMAA)

- Student loan interest deductions

- Certain education-related tax benefits

- Net Investment Income Tax calculations

Understanding these calculations can help taxpayers better evaluate how changes in income may affect eligibility for various tax provisions.

Common Factors That Can Affect AGI and MAGI

Several financial decisions can influence AGI and MAGI calculations, including:

- Retirement plan contributions

- Health Savings Account (HSA) contributions

- Business income and deductions

- Investment income

- Retirement account distributions

- Capital gains and losses

Because AGI and MAGI are used throughout the tax code, changes in one area of a financial plan can sometimes affect eligibility for other tax benefits.

When AGI and MAGI Become More Important

AGI and MAGI calculations often become increasingly important for individuals with multiple income sources, investment portfolios, business ownership interests, retirement account decisions, or Medicare planning considerations.

Individuals evaluating Roth IRA contributions, Roth conversions, Medicare premiums, or tax-efficient withdrawal strategies frequently review AGI and MAGI as part of the planning process.

For additional educational resources, visit our free resources page.

When Professional Guidance May Be Helpful

Because AGI and MAGI calculations can affect many areas of the tax code, taxpayers often work with qualified tax and financial professionals to better understand how income decisions may impact their overall financial situation.

Brooks Wealth Management works with professionals, business owners, retirees, and families on financial planning, retirement planning, investment management, and wealth management considerations.

About This Resource

This resource provides general educational information regarding Adjusted Gross Income (AGI) and Modified Adjusted Gross Income (MAGI). It is not intended as tax, legal, or accounting advice. Individual circumstances vary, and tax laws are subject to change.

If you would like to discuss your financial situation, we invite you to schedule an introductory conversation.